Speaking at the Federal Reserve’s annual retreat to Jackson Hole, Wyoming on Friday, 23 August 2024, Fed Chair Jerome Powell finally committed to cutting U.S. interest rates after months of playing “will they or won’t they, even though everybody knows we’re going to.”

The S&P 500 (SPX) responded to the Fed’s commitment by rising 1.15%, ending the week at 5,634.61, up 1.45% from where the index closed out the preceding week.

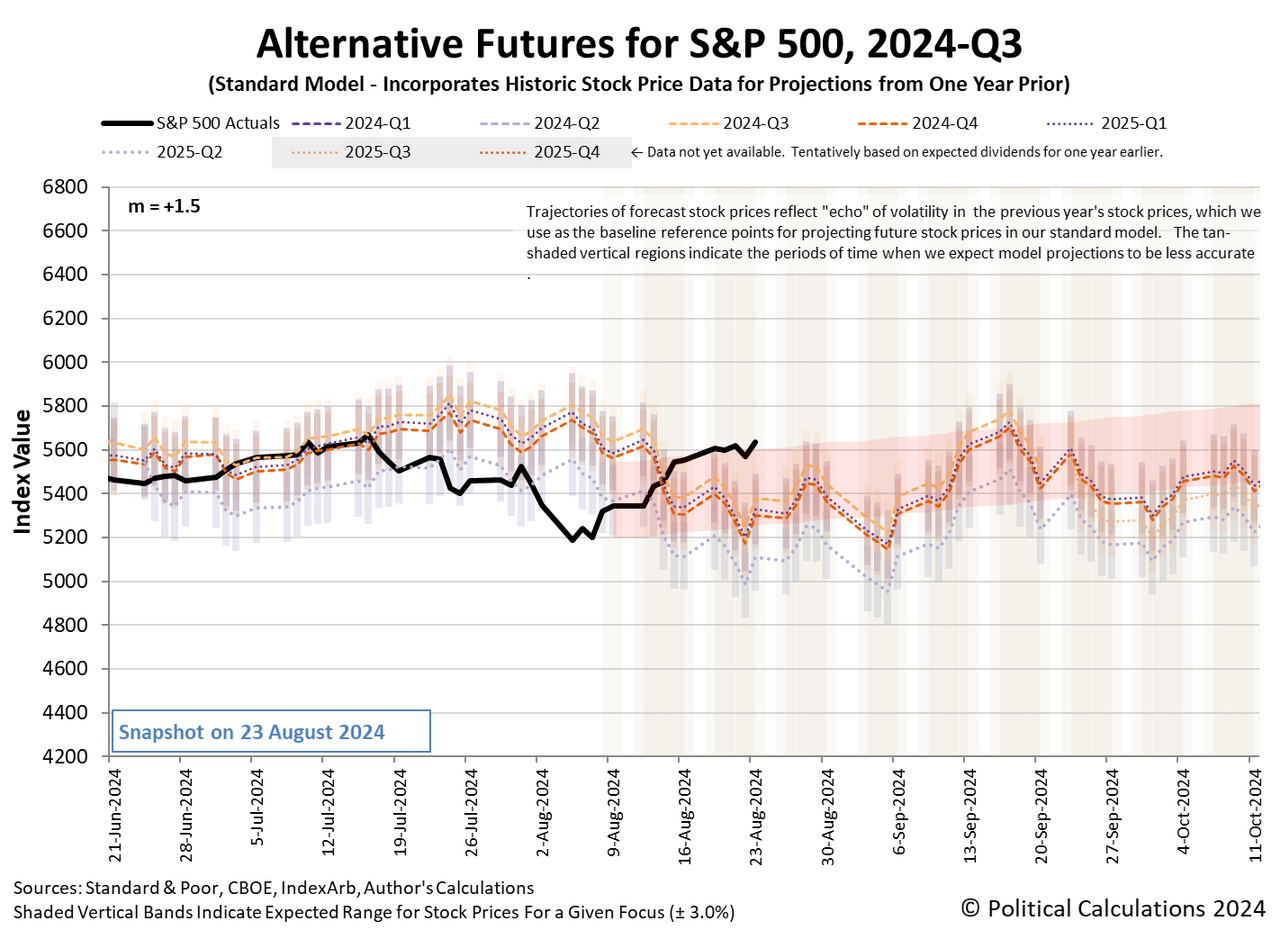

That’s less impressive than might have been predicted, but the level of the S&P 500 is consistent with investors focusing their attention on the current quarter of 2024-Q3. Investors have reason to do so because now the question at the center of billions of investment decisions is no longer “will they cut?” or “when will they cut?” but instead is now “how much will they cut?”

The CME Group’s FedWatch Tool continues to anticipate the Fed will hold the Federal Funds Rate steady in its current target range of 5.25-5.50% until 18 September (2024-Q3). On that date, the Fed is expected to start a series of 0.25%-0.50% rate cuts that will occur at six-week intervals well into 2025.

In the latest update for the alternative futures chart, we find the trajectory of the S&P 500 running just above the top end of the redzone forecast range.

As regular readers will recall, that redzone forecast range is based on the assumption that investors would be shifting their forward looking attention from the distant future quarter of 2025-Q2 toward the nearer term quarter of 2024-Q4 during the period it covers. Instead, the Fed’s long-awaited commitment to cutting rates has prompted investors to draw their attention back to the current quarter, which is why the S&P’s trajectory has settled where it has without any more impressive change in its level on the biggest news of the week. If we were to re-draw the redzone forecast range to show that adjustment, the actual trajectory of the S&P 500 would fall well within the projected range.

As it is, without dramatic new information to compel it to perform otherwise, we think the S&P 500’s trajectory will increasingly converge with the redzone forecast range shown on the chart because investors will have no reason to maintain their focus on the current quarter for much more than the next four weeks and will once again reset their forward time horizon. We think the next change will involve them shifting their attention toward 2024-Q4, which the redzone forecast range already assumes will happen.

Meanwhile, other things happened during the week that was, here are the week’s market-moving headlines:

Monday, 19 August 2024

- Signs and portents for the U.S. economy:

- Fed officials now expected to deliver three rate cuts in rest of 2024, to signal upcoming policies at Jackson Hole event:

- Nasdaq, S&P, Dow end higher as investors wait for Powell Jackson Hole’s speech

Tuesday, 20 August 2024

- Signs and portents for the U.S. economy:

- Fed officials paying more attention to soon-to-be revised jobs data:

- Bigger trouble developing in China:

- BOJ officials now expecting wage inflation, but won’t do much about it:

- ECB officials thinking about next Eurozone rate cuts, may have caught a break with German wage inflation:

- Nasdaq, S&P, Dow end lower, break win streaks as investors cast eye toward Fed rate views

Wednesday, 21 August 2024

- Signs and portents for the U.S. economy:

- Fed officials thinking about when, how much to cut U.S. interest rates:

- Bigger bailouts developing in China:

- BOJ officials seeing Japan’s export economy slow, majority of economists think they’ll be forced to hike rates in Japan again this year:

- S&P, Nasdaq, Dow end higher after Fed minutes point to rate cuts beginning in September

Thursday, 22 August 2024

- Signs and portents for the U.S. economy:

- Fed officials getting excited to start cutting U.S. interest rates, claim there won’t be any recession:

- Slowing decline in Japan’s factory output:

- BOJ officials influencing global central bank policies as synchronized Japanification spreads:

- ECB officials get summer boost from Olympics, looking forward to next rate cut:

- Nasdaq slumps, S&P, Dow end down ahead of Powell’s potential signal on rate-cut sizing

Friday, 23 August 2024

- Signs and portents for the U.S. economy:

- Fed officials commit to cutting U.S. interest rates in September 2024:

- Studies find Fed actions more impactful than words, use mortgage bonds to influence economy’s momentum:

- BOJ officials looking at stagflation, claim’s they’ll get a benefit from Fed rate cuts:

- ECB officials getting excited to cut Eurozone interest rates again:

- S&P, Nasdaq, Dow end higher after Powell says rate cuts are in the pipeline

The Atlanta Fed’s GDPNow tool’s projection of the real GDP growth rate for the current quarter of 2024-Q3 remained at +2.0% with no updates taking place during the past week. It will next be updated during the upcoming week.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here