Research Note Summary

Today’s research note will focus on Royal Bank of Canada (NYSE:RY), also commonly known on Wall Street as “RBC”, and a major player in the diversified banks sector. My note today will be a 3-month review after my last note on this bank.

Since my last rating of this stock in June, which I rated a buy, the stock price had jumped up going into mid-summer, as the chart below shows, presenting a potential opportunity for capital gains. However, after that opportunity passed the price took a steep dip again. Does this present a buy opportunity now?

RBC – price performance since last rating (Seeking Alpha)

As it turns out, after today’s analysis I reaffirmed my buy rating for this stock again.

Its tailwinds are driven by dividend growth, top-line and bottom-line growth, and a relatively cheap share price compared to the long-term moving average.

Some headwinds discovered are underperformance vs the S&P 500 index and overvaluation.

A risk discussed further was exposure to office loans in their commercial real estate portfolio, which was determined to be a low risk.

Methodology Used

I will utilize my WholeScore Rating methodology which looks at this stock holistically across 7 categories including potential downside risks, and assigns a rating score.

Some of the financial data comes from the most recent quarterly earnings release on Aug. 24th (for fiscal 2023, Q3 ended July 31st). Forward sentiment relates to fiscal Q4 earnings results due out on Nov. 30th.

Industry Outlook

This company lies in the sector of diversified banks, according to Seeking Alpha. I would add that it is essentially a bank on a global scale, as one of the largest based in Canada, and with that said in order to find comparable banks I picked 8 very large global well-known banks trading on major exchanges.

These banks tend to be very diversified in terms of products and services, and some or more have wealth management shops in addition to the personal / business banking and institutional, and perhaps a brokerage shop too.

This sector makes a considerable amount of revenue from interest on assets it holds, and other revenue from things like fees, and some from trading. In elevated interest-rate environments, it is important to mention that while these banks can earn more interest they also can incur higher interest expenses both on deposits and on borrowing they do to raise additional money for the bank.

This could be from issuing new corporate bonds or borrowing from the Fed’s lending facility, or interbank lending. It is important to grasp this before someone decides to invest in the banking sector, in my opinion.

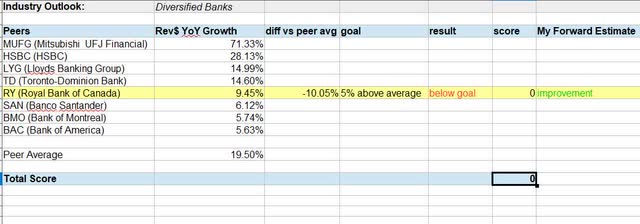

In the table below I created, comparing the YoY revenue growth among this peer group I created, this bank lies somewhere in the middle of the pack on revenue growth.

RBC – industry outlook (author analysis)

Unfortunately, I gave it a score of 0 in this category since it did not meet my target of achieving a 5% above-average revenue growth. Instead, it achieved revenue growth -10% below average.

However, my future sentiment is positive and I expect improvement in revenue growth.

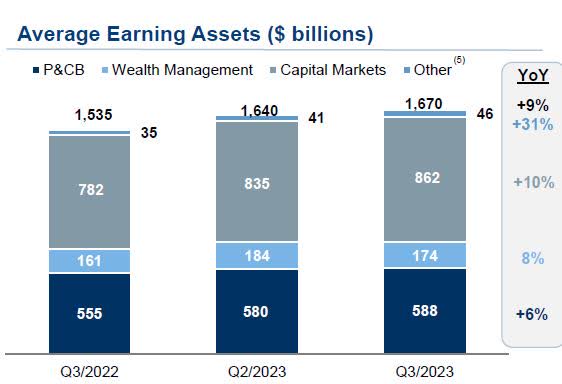

One indicator of this is the increase in this bank’s interest-earning assets, and interest is a major source of revenue for a bank:

RBC – growth in avg earning assets (RBC quarterly presentation)

As you can see in the above graphic, the firm achieved a 9% YoY growth in “earning” assets, which I find to be a positive indicator of future revenue growth since these assets earn revenue.

Financial Statements

To understand this firm’s fundamentals, the three financial statements I care about are the income statement, balance sheet, and cash flow statement.

If you look at the table below, you can see that this bank has met or outperformed all of my goals / targets.

RBC – financial statements (author analysis)

For example, it achieved 14.2% YoY revenue growth and 5% YoY net income growth, outperforming my target of 5%.

It also achieved YoY growth in free cash flow per share of 119%, quite an impressive growth, not to mention YoY growth in positive equity of 5%.

In a nutshell: it grew revenue, profitability, cashflow per share, and equity.

I already mentioned a key revenue driver looking forward, and that is growth in interest-earning assets, so my sentiment on revenue and earnings is positive, as well as on cash flow.

In terms of positive sentiment on equity, consider that increasing debt can have an effect on equity and possibly lower it since it can increase liabilities. In this case, we see a trend of YoY decreasing long-term debt.

As you can read from my recent research notes, companies with increasing debt loads are a concern of mine, whereas this one seems to be going in the opposite direction.

RBC – long term debt (Seeking Alpha)

I deservedly gave this stock a total score of 4 in this category.

Dividends

When it comes to dividends, my targets for any stock are that it pays at least $0.10 per share on a quarterly basis (earning $100 a year in dividends on 100 shares), has a dividend yield at least 5% above its sector average, and 3-year dividend growth of 5% or better.

If you look at the table I created, this stock meets or beats my goal on all of those:

RBC – dividends (author analysis)

If you compare the dividend amount in fiscal 2023Q3 with 2020Q3, it shows a 3-year growth of almost 22%. I expect this to remain as long as the dividend is not raised, but I also expect to happen again due to profitability.

The yield of 4.75% could drop slightly since I expect the share price to rise, which can affect yield. Again, revenue growth is what I think will push the share price up and bring out the bulls.

In this category, I confidently gave the stock a score of 3.

Share Price

In this section, I am looking for a share price opportunity that tells a “value” story, and I think I found it!

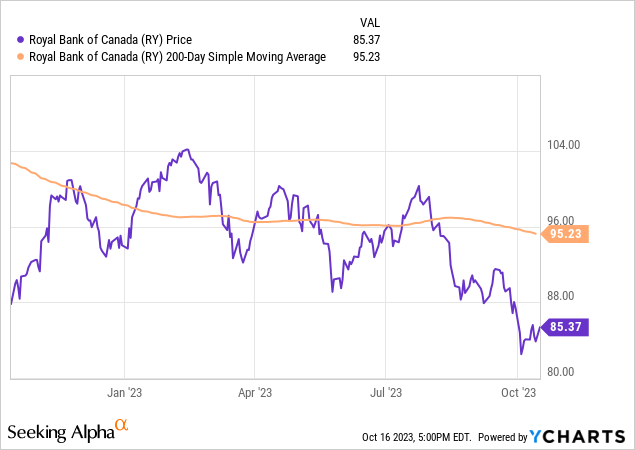

If you look at the YCharts below, you can see the stock did a crossover below the 200-day moving average sometime this summer and is now trading considerably below average at $85.37, as of the writing of this article. Incidentally, it was the closing price on Monday, Oct. 16th.

My target is a share price no higher than 5% above the 200-day moving average, and as you can see in my table below this stock is now trading at 10.35% below this long-term average, so I consider this a buying signal.

RBC – share price (author analysis)

In this category, I gave it a score of 1.

I also want to reiterate that I don’t think it’s possible to predict with 100% certainty a future share price, so my portfolio strategy is to track the 200-day average and wait for the share price to not go too far above it, as I think that would limit the upside potential and increase the downside price risk.

Again, we are not talking about a perfect buy or sell price but about decreasing downside and increasing upside potential, as a very simple strategy.

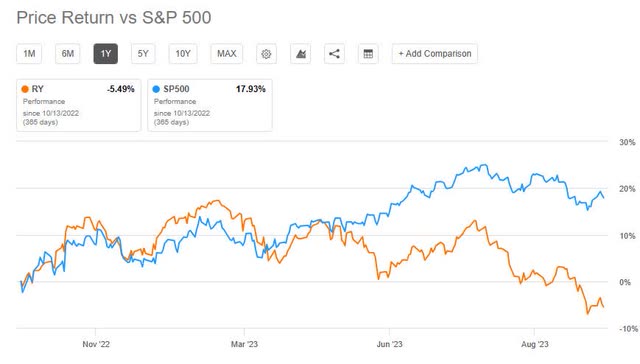

Performance vs S&P 500

Let’s take a quick look at the 1-year price performance of this stock in relation to the performance of a major index like the S&P 500. This comparison is my gauge of general market momentum for this stock.

Now, I may be ambitious but my target is a 5% outperformance of the index. I did not get it with this stock, however, which saw a 131% underperformance vs the index.

RBC – price vs S&P 500 index (author analysis)

I gave it a score of 0 in this category this time, however, I anticipate future improvement vs the index since the financial sector itself which saw a drop in market momentum this year since the spring banking sector turbulence, evident in the chart below which shows this stock dipping below the index around March.

RBC – price 1 year return vs index (Seeking Alpha)

It also did not help that we read media stories this summer about ratings agencies downgrading some banks in the US.

However, I think the key tailwinds for this sector, and this firm as part of it, is the continued high interest rate environment which is driving record interest revenues, along with revenue YoY growth in this sector and earnings surprises. For example, this bank beat the fiscal Q3 earnings estimate by $0.09, after having a miss in Q2.

Valuation

The metrics on valuation I am looking at are the forward price-to-earnings and price-to-book ratios.

In the table below I made, you can see both are overvalued. My target is no more than 5% above the sector average, and this stock is well above average on both ratios, which I think will remain the same in the near term.

RBC – valuation (author analysis)

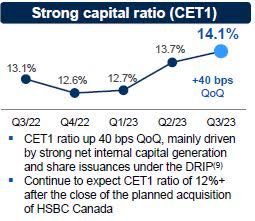

As far as what is driving this overvaluation, I would say that it is the positive earnings growth YoY which I mentioned earlier, and the market is expecting even better earnings going forward, but also balance sheet expansion.

Consider also that the capital ratio continues to increase, and according to the company it is driven by “strong net internal capital generation and share issuances.” but also expecting capital strength “after the close of planned acquisition of HSBC Canada.”

This is significant because it will take on all the assets of that bank it takes over.

RBC – CET1 ratio (company quarterly presentation)

I gave this stock a score of 0 in this category, as I see it being too overvalued, though the reasons why it is overvalued are clear and I have mentioned them.

Forward-Looking Risks

The risk I identified is a downside risk and could impact my bullish sentiment. Let’s take a look at the table below I created.

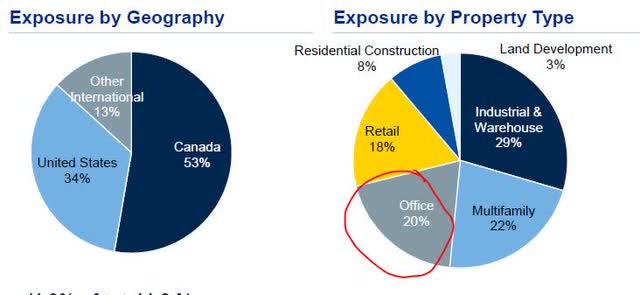

As a large bank, it is exposed to certain asset risks in its portfolio. With concerns lately in the media about exposures to commercial real estate and defaulting office loans, I wanted to see where this firm stands on that.

For instance, a Business Insider article in August spoke about the issue.

According to the story:

Office loans just hit a 5% delinquency rate – a 20 month high – as work from home and rate rises pile more pressure on commercial real estate.

It turns out that about 20% of its CRE portfolio is tied to office properties, but a large portion of them is in suburban areas and also require guarantees / collateral.

In this case, I gave it a risk impact score of 2( low) and probability of 5 ( high), for a total risk score of 7 which is within my tolerance.

RBC – risks (author analysis)

So, the total score I gave this stock in this category is +1, which is positive.

The supporting evidence is below.

Consider the following graphic from the company, showing the proportion of office vs total CRE exposure:

RBC – CRE Office exposure (company quarterly presentation)

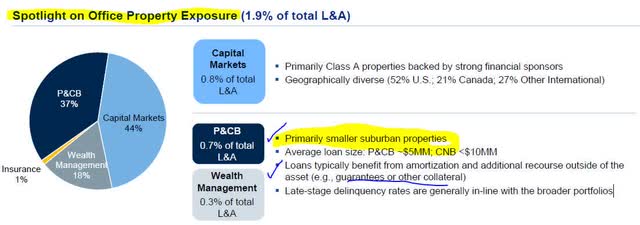

In addition, consider this data below which speaks to more detail on risk mitigation factors this company undertook when it comes to office loans:

RBC – CRE office exposure – detail (company quarterly presentation)

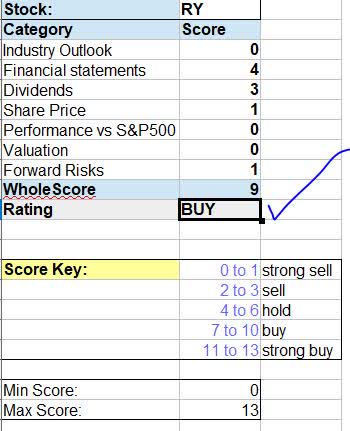

WholeScore Rating

I gave this stock a WholeScore of 9, which is a buy rating.

So, my rating remained the same as in the prior coverage and my prior rating is reaffirmed.

RBC – WholeScore (author analysis)

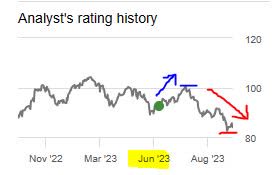

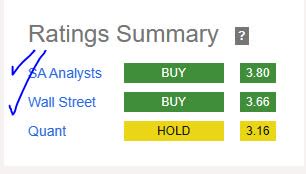

This time around, my buy rating is in line with the consensus from both SA analysts and Wall Street, which is good news as it shows that many other analysts may be seeing the value of Canadian bank stocks, a hidden gem I discovered earlier this summer after reviewing a few of them including this one.

RBC – rating consensus (Seeking Alpha)

Read the full article here