Thesis

Nasdaq, Inc. (NASDAQ:NDAQ), one of the holdings in which I am indirectly invested through Investor AB (OTCPK:IVSXF), posted strong Q3 earnings. In my last article on Nasdaq, I talked about the Adenza acquisition and its implications, especially regarding the two major shareholders, Thoma Bravo and Investor AB, and how this might play out. It is too early to judge the relationship between these two major shareholders, but the Q3 results have some interesting facts that I would like to talk about, especially the debt and its impact. My main point is that Nasdaq needs to reduce its debt in order to be more attractive and have more flexibility for investments.

Nasdaq Q3 Earnings Review

Nasdaq Q3 Investor Presentation

Nasdaq posted strong results from a growth perspective. The Solutions business, which now represents 74% of total revenues, grew 8% organically or 9% on a constant currency basis. Overall, net sales growth was 5% organic or 6% on a constant currency basis. Definitely a strong performance in a challenging environment.

In particular, the Index segment benefited from the strong YTD performance of the Nasdaq index, with inflows of $24 billion YTD and $5 billion in Q3. On a year-over-year basis, assets under management (“AUM”) is up 22% and index fees are up 15%.

Nasdaq Q3 Investor Presentation

The IPO market also seems to be recovering somewhat, as there were 35 new IPOs on the Nasdaq in Q3 and 83 YTD. However, the win rate is still 7% lower year-over-year at 84% compared to 91%. Still, management is optimistic about 2024 and the prospects for new IPOs. With Arm Holdings (ARM) and Instacart (CART), Nasdaq had two of the most hyped IPOs in 2023.

The Anti-Financial Crime segment performed even better with a 21% year-over-year growth rate, driven by strong surveillance growth and Verafin’s strong client growth.

Nasdaq Q3 Investor Presentation

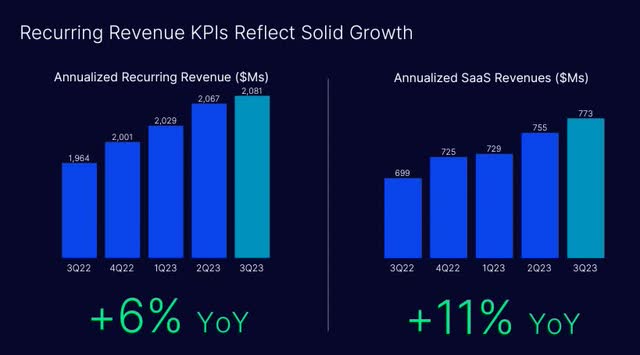

Total ARR also developed favorably, growing 6% to $2.1 billion, and annualized revenue grew 11% to $773 million, representing 37% of total ARR. These are both things that Nasdaq’s management team predicted they would focus on, and they delivered. In the long term, the goal is to reach a figure of 50% of ARR coming from SaaS.

Nasdaq Q3 Investor Presentation

Among the trends Nasdaq sees are an increase in passive and thematic investing, more digitalization, and a strong need for financial crime intelligence solutions. In addition, risk management, regulatory compliance and ESG are things where they are also investing to grow and see a big total addressable market (“TAM”). As you can see in the graph above, they believe that they have only a small part of the TAM at the moment and, therefore, have many growth opportunities that they will take advantage of.

One thing I would point out is that there is a big difference between the GAAP and non-GAAP numbers for Nasdaq. The non-GAAP operating margin for the first nine months is 52%, while the GAAP operating margin is only 44%. I am not a big fan of some of the adjusted numbers, so I would advise investors to look at the GAAP numbers as a better guide, as Nasdaq mostly uses the adjusted numbers in their press releases.

NDAQ Q3 Earnings Call Summary

Nasdaq Q3 Investor Presentation

Many questions were asked about the Adenza acquisition, which is expected to close in Q4 2023. Nasdaq’s management team sees good synergies and is working with Adenza’s team to make the transition as smooth as possible. They also discussed Adenza’s strong YTD performance, which included the addition of 17 new customers and a strong net retention rate of 113%.

The SEC also approved the first AI-powered order type called dynamic M-ELO, which stands for dynamic midpoint extended life order. This is for clients looking for larger trade sizes in the midpoint and will improve fill rates and reduce market friction. In addition, a beta version of an AML workflow co-pilot will be launched in October, using generative AI to help clients automate the AML process. In the ESG space, there will be 2 new offerings to help companies meet their sustainability goals.

Also, the CFO will step down after 8 years and the new CFO, who will be recruited from UBS, will start on December 1, 2023. It will be interesting to see if this changes some aspects of Nasdaq’s financial situation.

The difference between Google’s (GOOG) AML offering and Verafin’s was discussed. One of the main advantages is that Verafin uses data from around 2500 banks which they can leverage and they have a low upfront investment for customers as it is a cloud solution. Google, on the other hand, has 1 specific bank they are currently working with.

A very small preview for Q4 was given as they mentioned that 40% of the bookings for the Anti Financial Crime unit occur in Q4 and that Adenza has a somewhat similar cycle as they also have 40% – 45% of their bookings in Q4.

Nasdaq’s Balance Sheet

Nasdaq Q3 Earnings Presentation

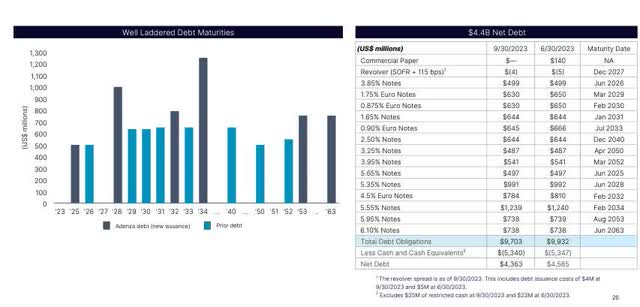

With $9 billion in total debt and only $1.1 billion in TTM net income, Nasdaq is highly leveraged. Even if we include the cash position, net debt is $4.9 billion, or ~4.5 times net income. A threshold for many investors is that debt/net income should be < 4. In an era of cheap credit, leverage was not a major concern for most investors, but as times have changed and interest rates have risen, the environment has evolved and some companies are in a dangerous position. Highly leveraged companies could be in big trouble if they need to refinance at higher rates. And with the Adenza acquisition, Nasdaq has new debt of $500 million due in 2025 at 5.65% and $900 million due in 2028 at 5.35%. Plus 4 more with later maturities.

They did reduce debt by $200 million vs. Q2, but it will take some time to get to <4x. But unlike other companies, Nasdaq still has strong free cash flow (“FCF”). TTM FCF is $1.6 billion and YTD is $1.3 billion. So, if they focus their capital allocation on reducing debt, it will greatly reduce the risks to the company and its shareholders.

Capital Allocation of NDAQ

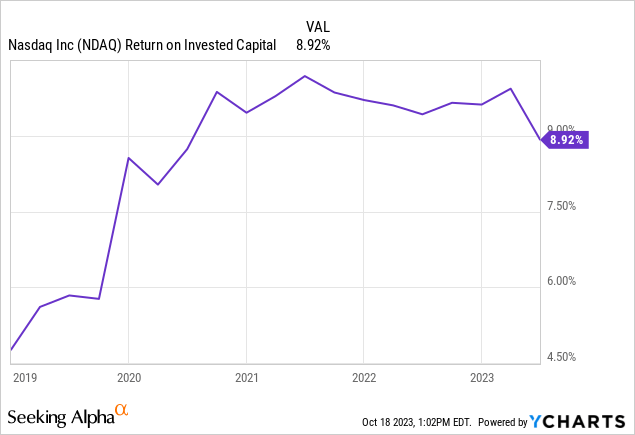

Nasdaq’s ROIC is only 8.92%, while their WACC is between 9% and 10% because of their high leverage. So, right now they are not creating value and have a negative ROIC-WACC spread. Another sign that they clearly need to reduce debt. The WACC needs to be lowered.

However, management understands this and has laid out the following capital deployment plan. Investing in organic growth is the No. 1 priority, while deleveraging is No. 2. Dividends and share repurchases to offset dilution are the targets if plan 1 and 2 are achieved.

Reverse DCF

Author

In my opinion, one of the best tools to see if a stock price is justified is a reverse discounted cash flow (“DCF”) analysis. Nasdaq’s stock price implies EPS growth of 12% over the next 5 years and 9% over the next 5 to 10 years at a 10% discount rate. The basis for the reverse DCF was TTM diluted EPS of $2.23.

Historically, the EPS CAGR over the last 10 years was 14.09%, which would make the stock look cheap, but over the last 5 years the EPS CAGR was only 8.39%. So, depending on the time frame we look at, the story changes. However, since future execution is key and Nasdaq has many growth opportunities, I believe the stock is fairly valued. Nasdaq could generate the required EPS growth rate if their strategy succeeds.

Conclusion

Nasdaq’s management team has historically demonstrated a long-term focus, and they continue to execute on the strategy they have set. The trends they are trying to capitalize on are clearly defined and have great growth opportunities. Furthermore, the stock is fairly priced, and every bit of debt reduction minimizes risk. The strong ability to generate FCF and the increasing share of recurring revenues are also very positive signs for the future.

In summary, I think Nasdaq is a high quality company that could return a lot of capital to shareholders after reducing debt to a debt/net income <4, hopefully closer to <3. Rising dividends and buybacks would then have a strong positive impact on total shareholder return.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here