For all its longstanding live service games and impressive cash generation over the years, gaming giant Electronic Arts (NASDAQ:EA) has been trading in the same range for years now with a stagnant dividend. Currently, the main matter weighing on the stock’s outlook is where the next big hit is coming from, or indeed whether it’s coming at all. For this reason it’s hard to see the appeal over higher growth or stronger dividend options.

State Of Key Franchises

The core line up of franchises EA depends upon continue to serve as impressively profitable cash cows. The transition to EA Sports FC from FIFA was more or less shrugged off as inconsequential following the license debacle despite it being widely reported as risky at the time, with management reporting ‘high teens’ growth YoY in their football franchise. Meanwhile Apex Legends, recently having entered its 21st season, has reached an impressive $3.4 billion in lifetime net bookings, although is a bit weaker growth wise and had an embarrassing security issue during a competitive event not long ago.

The Sims 4 players are up double digits for FY 24 and Sims Online and Sims Mobile have over 500 million downloads. There is also a Sims movie in the works produced by Margot Robbie’s production company which EA would be remiss not to capitalise on, given the success of the Barbie movie, as well as the recent resurgence of interest in Fallout following its series. Adding to this pattern, there’s the success of The Last Of Us’ HBO show and the impact of the Edgerunners anime on the reputation of the once maligned Cyberpunk.

This success of gaming IPs in other media is obviously one theme in the games industry at the minute, but the rest of EA’s IP library seems poorly positioned to take advantage of this. How would EA SPORTS FC, Madden, Battlefield ever be adapted? These are not exactly IPs which provide rich script or worldbuilding material.

Having confirmed that the latest season of Battlefield 2042 will be the last, the matter of how EA will salvage the franchise is an uncertain one. There is no specific information on the next mainline title, but EA appears to be working on something.

Andrew Wilson, Q4 earnings:

Motive, armed with cutting edge frostbite technology and compelling storytelling is joining dice, criterion and ripple effect to build a Battlefield universe across connected multiplayer and single-player experiences. This is the largest Battlefield team in franchise history. A few weeks ago, I was visiting with the teams and I couldn’t be more excited about what they showed and what we were able to play.

Motive, developer of the Dead Space remake, joining the effort along with the others means EA is putting a lot of resources behind revitalising the franchise. The language here and a later reference to what’s coming as a ‘tremendous live-service’ is not promising though and has already been received poorly. After all, the original failure of Battlefield 2042 could be attributed to pushing the live service model too far and away from the roots of the earlier games. Returning the Battlefield franchise to its glory days would be one avenue towards growth, but entirely new IPs would provide a clearer catalyst.

Fresh IPs In The Pipeline?

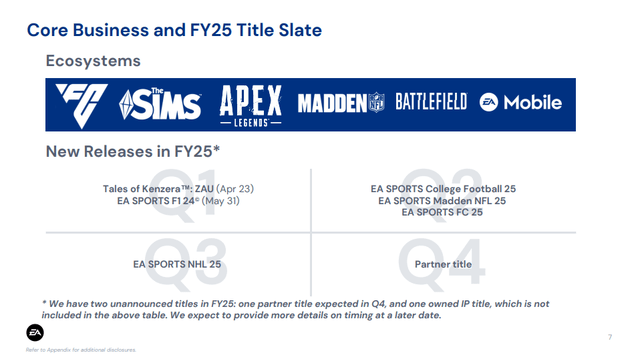

If EA’s key franchises are indeed a mixed bag with relatively flat growth, then it is natural to look to further down the line for big, new IPs on the horizon. In that respect, FY25 can offer one answer: College Football 25. The official reveal trailer already has over 2 million views on YouTube after only days, so there is some hype for the game, which is due for July. Referring to the slide below though, there is a dearth of fresh titles not already part of existing franchises, College Football itself is part of the broader EA SPORTS umbrella and has previous entries. This relatively weak slate of games was alluded to in earnings so it undoubtedly has to be compensated for by growth in the established live service games.

EA Q4 earnings presentation

To me, this is an uninspiring outlook, so I would need to see an upcoming big title that is clearly a strong entry to become more optimistic, even with EA’s long term (successful) reliance on long running franchises.

The recent history of new IPs doesn’t inspire confidence either, Immortals of Aveum being one example of EA trying and failing to produce fresh successful hits. Saying that the game sold poorly would be an understatement, it capped out at 750 concurrent steam players — while somehow eating through a budget of $85 million.

AI

For the games industry as a whole, AI is unavoidable. An array of uses have already cropped up from voice and animation generation to changing NPC behaviour and even crude AI generated games. Accordingly, AI is already being used in EA’s development process, specifically it has increased the number of run cycles (animations) in FC 24 to 1,200 from 36 in FIFA 23. What’s more, this acceleration of development isn’t expected to be limited to niche areas, CEO Andrew Wilson thinks generative AI might positively affect more than 50% of development processes. Andrew Wilson has made quite a few comments regarding AI recently, addressing longer term views on the matter, some with intriguing implications.

Andrew Wilson, Morgan Stanley Conference:

So if you fast forward this over a five year plus time horizon, you think about where we’ve got to in terms of efficiency, what I would like to believe is 30% more efficient as a company, where we can attract 50% more people into our network. And hopefully by virtue of the nature of content that we can create through generative AI, which will be created faster and more personal to every player, that there’s 10% to 20% more monetization opportunity to us on an ARPU level.

Andrew then goes on to speculate on the possibilities even further in the future:

How do we build these things to allow us to build bigger, broader, more deep, more personal experiences? And then how do we give that to the world? And once you give that to the world and you have 3 billion players around the world creating personal content and expanding and enhancing the universes that we create and building and creating their own universes on our technology platform, all of a sudden we are the beneficiaries of platform economics. And for me, that’s a multi-billion dollar opportunity for us in addition to what we would otherwise get out of our regular growth.

It’s worth underscoring that this is not a minor statement for the CEO of an industry-leading gaming company to be making regarding AI and the future of gaming. This would be quite the departure from EA’s current business model, the platform dynamic being one very lucrative potential outcome, although presumably this kind of scenario also implies some risk in less favourable ones. For instance, in a world where games are AI generated and user guided, what exactly is the role of traditional gaming companies like EA? Where is the moat? One potential advantage is data. Data is one of the main constraints on AI training runs right now and the immediate supply is drying up for AI companies. EA has 40 years of data, which the CEO speculated could be used to feed models and speed up the progress of its efficiency in gaming.

Q4 And FY

Total net bookings for the quarter were down 14% YoY at $1.67 billion, missing Street expectations by $100 million. The breakdown was $259 million for full games and $1.41 billion for live services. Total net bookings for the year of $7.43 billion increased 1% YoY, while outlook of $7.3 billion to $7.7 billion was also under expectations. Generally, FC Ultimate Team is mentioned as driving strength in live service while being balanced by muted performance from Apex Legends, though Apex also saw high engagement in the latest quarter according to management. EA’s performance this quarter underlines the general sentiment that new IPs and franchises are needed to reinforce currently flatlining growth. On the plus side, buybacks of $5 billion over the coming 3 years were announced, possibly providing some stability for the stock.

Valuation

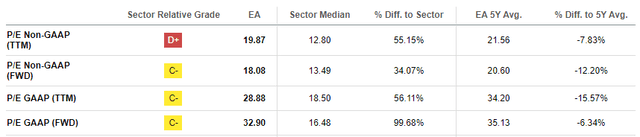

EA usually trades at a premium relative to other gaming companies, one slight positive for the stock here is that price and enterprise multiples are both currently somewhat below the five year average. A forward Non-GAAP P/E of over 18X is still 34% above the sector median though, the GAAP P/E offers an even less favourable comparison, while a forward EV/EBITDA of 13.08 puts it at 71% above the sector, all considered quite expensive. Assuming a reduced Non-GAAP P/E of 16X which still allows some premium, and EPS of 7.47 taken from earnings estimates would imply a tad below $120 might start to look fairer.

Seeking Alpha Seeking Alpha

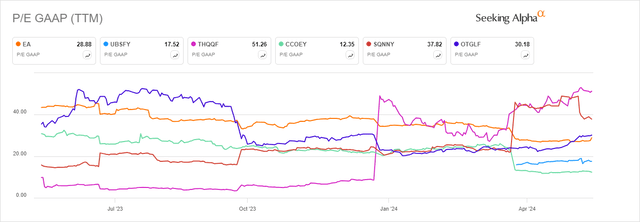

Charted below a selection of gaming only stocks compared on a trailing P/E basis tells a similar story, of a relatively expensive stock converging slightly with the broader market. This isn’t pronounced enough to be a strong factor in favour of EA for me, given the outlook it might even seem appropriate.

Seeking Alpha

Conclusion

EA is in need of more big hits on the horizon to help languid growth following a disappointing quarter and so far these are mostly not materialising. College Football 25 carries a lot of the expectations in this regard, so the game’s reception will be an important bellwether for the stock. While the company has a strong track record when it comes to anything related to EA SPORTS, management of other titles has been less impressive. These factors, coupled with a valuation that still does not seem very cheap is why I am neutral here.

Read the full article here