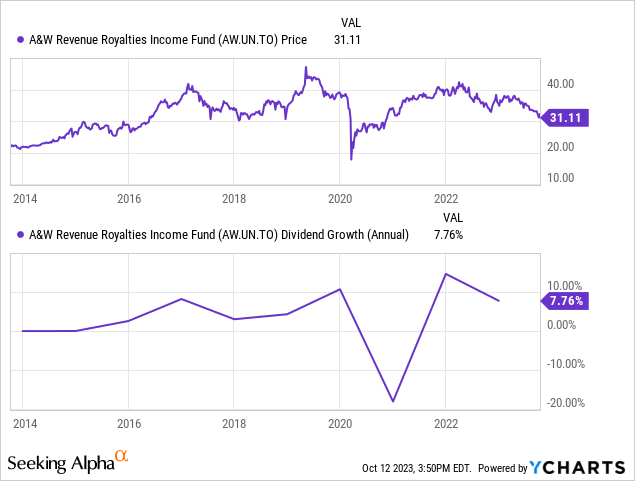

A&W Revenue Royalties Income Fund (OTC:AWRRF) has been a strong dividend grower over the past number of years. A&W Trade Marks Limited Partnership owns the ability to create the restaurants in Canada. They have a strong position in the Canadian fast food market, and recent focus on breakfast could benefit them long term. I have covered A&W before written here on the impressive sales trajectory in February 2023. It was a solid buy for the income part of a portfolio then, but has only gotten more intriguing for long term investors. However, the recent bond yield explosion on the long end of the curve has put heavy pressure on dividend stocks. Royalty plays have taken a big hit, as bond yields are now more intriguing versus previous compared to the strong 6.2% yield AW.UN has. The company has also put out Q2 results showing slowing same store sales growth. However, the decrease in price from above $40 to now near $31 is a huge buying opportunity, as they continue to innovate the menu and increase the restaurant pool consistently each year. They are a monthly dividend payer, helping give retirees that consistent income that they desire.

Q2 results – mixed bag

A key piece in whether a royalty company can grow its share price long term, is a function of the growth rate of the underlying dividend. If the underlying business is performing well, the market will reflect it in the price. For all royalty consumer plays, revenue and same-store sales growth are the main focal points contributing to dividend growth. When growth in same store sales for A&W was above 10%, the stock traded at a premium to many other royalty companies at around 5% dividend due to fast growth rate. Now at 6.2% per year it is a bargain. While shorter term dividend growth has stopped, the macroeconomic environment has been the reason for it. A&W has added 22 restaurants over last year which is a reasonable 2% growth rate. The market isn’t fully saturated but it does require a better environment to facilitate better growth in units.

Sales growth has slowed as inflation has bit into consumer spending habits, with the bottom end of the market being squeezed significantly. This has led to the growth in same store sales in Q2 2023 of only 2.5%, after a strong 12.2% increase the year prior. However, with this not being a company specific issue and the dividend stable or potentially growing slightly in the coming year, the selloff seems overdone. The stock has declined 9.5% the past year in the meantime, and significantly more from its all-time high even as sales continue to grow. While weakness could appear in 2024 with flat or even negative same store sales, the dividend should be safe with worries about 2024 baked into the price at $31.20 today. Additional restaurants added to the pool in early 2024 should negate the slowing sales growth at each restaurant, but dividend increases may be hold if we don’t see one late this year. This is reflected in the chart below, as the stock dipped in 2017 as growth waned, as well as with the 2020 pandemic and the recent dip.

Menu upgrades – Jury is out

A&W isn’t just sitting on its hands either as it tries to add additional menu items to compete against the giants like McDonald’s. It has added a stylized brew bar with higher end coffee items like lattes and cappuccinos plus the iced A&W root beer offerings. This is now available at over 560 locations and with management leading into it, they see it bringing in some new customers that may not have otherwise visited. Starbucks has used this model effectively to compete in the breakfast area and A&W is hoping it helps them win share there as well. They also have added 3 new chubby chicken sandwiches to the menu recently, looking to utilize that brand and offer good value to customers. How much in same store sales these may be able to add is unclear for now, we should hear more commentary on both on the upcoming earnings call.

New chubby chicken lineup (A&W IR)

Conclusion – A great buy under $30

At the $31 CAD level it is currently at, A&W is a very interesting long term hold. It has averaged solid dividend growth over the past 10 years, while also providing some nice capital gains you may not see in other dividend payers. This Canadian issue is a great choice for those with a long term outlook as it continues to execute well and keep pace with new interesting menu items. I have held the stock for some time, through different phases of growth. However, I continue to hold due to the solid and growing dividend as well as good long term capital appreciation of shares. While short term it will be fairly volatile due to the ‘higher for longer’ yield mantra from the federal reserve, long term the stock is a winner.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here