Introduction

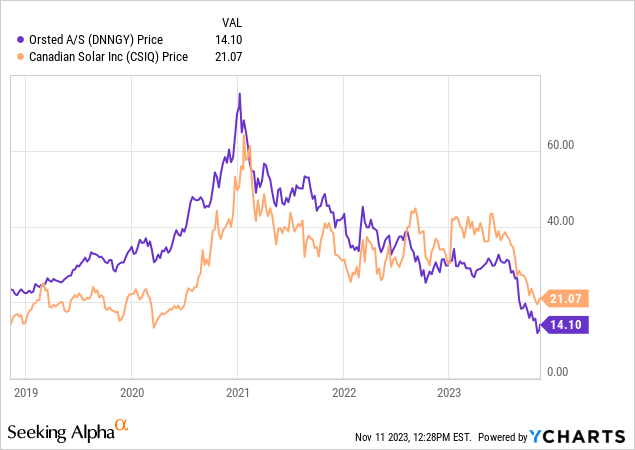

In this article I explore two companies with Grade A valuation in the renewable energy sector. These companies are Ørsted A/S (OTCPK:DNNGY) and Canadian Solar Inc. (NASDAQ:CSIQ). Both have experienced precipitous price movements in recent months. Since Q2 2023, highs both stocks are down well over 50% at current prices, and I believe they are at a buy point.

As my macroeconomic outlook includes a Biden Boom in the renewable energy sector, I rate these stocks a Strong Buy. Both companies supply to a highly lucrative industry with some serious government stimulus, a powerful tailwind to take effect. In my opinion, they should not be trading at their current valuation given long term trends towards sustainability. They deserve better multiples than what the market yields them for the likelihood of strong future cash flow driven by government subsidies in at least the near term. Although there are risks, I believe these two stocks will outperform the greater ESG indices and deserve a position in your portfolio.

Ørsted A/S

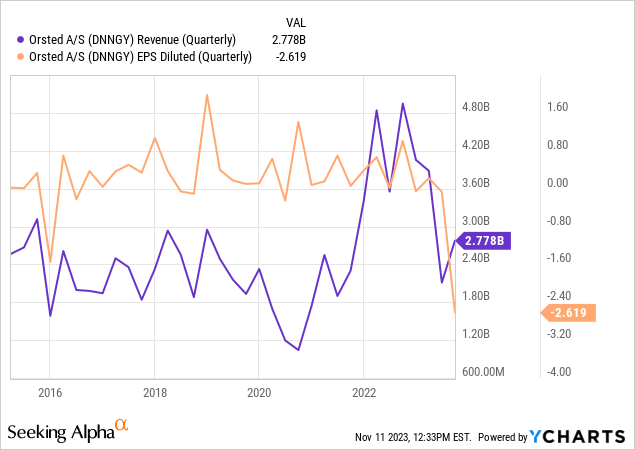

The decline in the price of Ørsted is due to the perceived jeopardy of future offshore wind farm projects in North America based on project cancellations. For background, Ørsted is the undisputed leader in offshore wind on this planet. They have implemented countless wind farms across the globe over three centuries. “Our growing portfolio of offshore wind farms will produce enough clean energy to power over 2 million American homes.” This is about 1.37% of American Housing Inventory, as estimated by the Federal Reserve Bank. Total American consumption of energy amounts to $1.3 trillion according to Michigan University. A liberal estimate of Ørsted’s annual revenue prospects is around $17.8 billion in the United States alone. The chart below shows the surprise hits that earnings and revenue have taken from H2 2022 and H1 2023 from operational performance and project cessation.

In 2022, total revenue was around $19 billion. According to figures on the company website, Ørsted will be looking to grow 2022 U.S. revenue by 150% over an unknown period of time through offshore wind projects alone. Offshore wind project completion in the United States will increase U.S. revenue from approximately $7 billion to $18 billion by my estimate. Total revenue should grow to $30 billion when just the current pipeline focused on North American offshore wind completes. However, time to completion for the project pipeline greatly effects the net present value of this company’s cash flows its valuation. Project cancellation for various reasons is a serious risk to Ørsted’s growth potential in North America. Seeking Alpha Quant gives Ørsted grade A and A- valuation and growth, with a low PEG ratio of around 0.72. Forecasted upticks in EPS is the main positive growth indicator. Momentum grade F indicates that there is no technical sign suggesting a bull market yet. I still believe Ørsted is near a buy point, and that fundamentals should improve as government tailwinds set in for the longer term and projects facing political impasses resume.

Canadian Solar Inc.

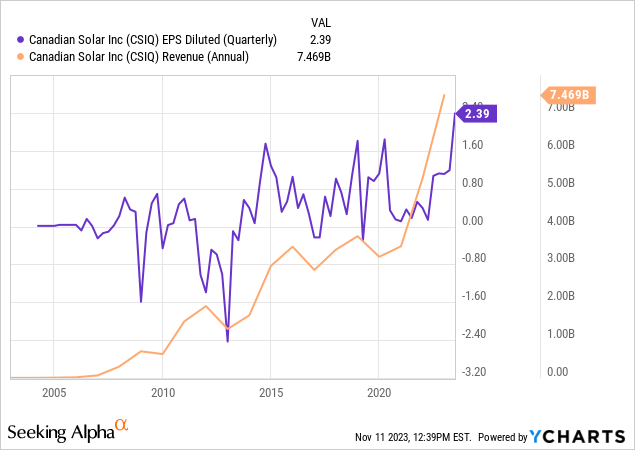

It is unclear what has caused the drop in Canadian Solar share prices. Apparently, the company experienced some severe sensitivity to the bond markets, with the green bonds it issues having depreciated, making it harder to refinance and raise capital for new projects. There is also concern with the majority Chinese ownership in an elevated geopolitical atmosphere. Canadian Solar has not only a strong leadership position with more than two decades of experience in the solar industry, but also made enormous contributions to the battery or energy storage markets. While many battery players are focused on concentrating power in small fuel cells for the electric vehicle market, larger next generation energy storage facilities not unlike nuclear power plants are a burgeoning technology to help smooth out energy consumption and production discord across communities. As shown below, Canadian solar is trading at a discount in spite of revenue and EPS Diluted at all-time highs.

Both solar and battery projects and wind projects too stand to raise capital in the form of tax credits. This technique of economic stimulus is likely underlooked in the numbers of mainstream banks in my opinion. This sort of policy device is relatively new and works similarly to the government’s investment in the Human Genome Project, from which tremendous advancements occurred for financiers, entrepreneurs, and society as a whole. Often times tax credits save a company upwards of 20% on total expenses and can even be liquidated in dark pools to help other companies offset their taxes. The value that Canadian solar is generating in its project operations is therefore tremendous, as is its pricing power and ability to capture upfront lots of capital, which are reflected in strong financials. Seeking Alpha Quant gives Canadian Solar a grade A+ for value and A for growth. The PEG ratio is just 0.02, compared to a sector median of 2.48. Although momentum is nearly a failure at a D, I argue that share prices are undervalued and present a good opportunity to a portfolio that doesn’t hold them.

Risks

Technically speaking, I believe there is a high degree of risk in holding these stocks at this time. There is no clear sign of a bottom, but all the while growth and valuation are around very attractive levels. Both companies are foreign to the U.S. but do business in the United States. Canadian Solar describes its project pipeline as “geographically diversified” and Ørsted as well has operations spanning across continents. For U.S. based investors, assets that do business in the U.S. or have strong U.S. consumer demand are less risky, and these assets are not pure plays by any means on the U.S. economy. They are global operations and therefore exposed to risks including but not limited to currency depreciation, war, and corruption.

Conclusion

For investors like me that prefer some technical momentum in a holding, it can be a little daunting to consider buying or adding to a position in these stocks while downtrending. Overall, Quant rates Ørsted a Strong Sell and Canadian Solar a Hold. By picking out some of the best metrics in these companies in the context of their marketplace weakness, I argue that investors who prefer to speculate based on fundamentals rather than technicals, and those who are interested in ESG diversification without paying ETF fees, may be interested in adding these two stocks to their portfolio at 50%+ discount prices. The green premium only increases with fossil fuel prices, and global conflict suggests these prices will remain high. This piece reflects my honest market outlook on 11/11/2023 as I write and is subject to change, revision, or follow up to be published exclusively on Seeking Alpha.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here