Investment Thesis: I rate Motorcar Parts of America as a Hold at this time.

Motorcar Parts of America (NASDAQ:MPAA) is a manufacturer and distributor of aftermarket parts (or parts not made by the original vehicle manufacturer) for a range of vehicle types, including passenger vehicles, light and heavy-duty trucks.

Over the last five years, we see that the stock has been on a downward trajectory, trading significantly below levels seen previously.

TradingView.com

The purpose of this article is to assess whether the stock has capacity for a rebound in upside going forward – taking recent results into consideration.

Performance

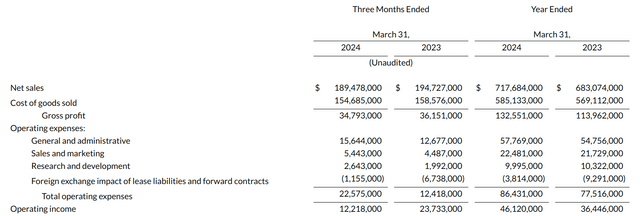

When looking at most recent earnings results for Motorcar Parts of America as released on June 11, 2024, we can see that net sales were down by -2.70% on that of the prior year quarter.

Motorcar Parts of America Reports Year-End Results: June 11, 2024

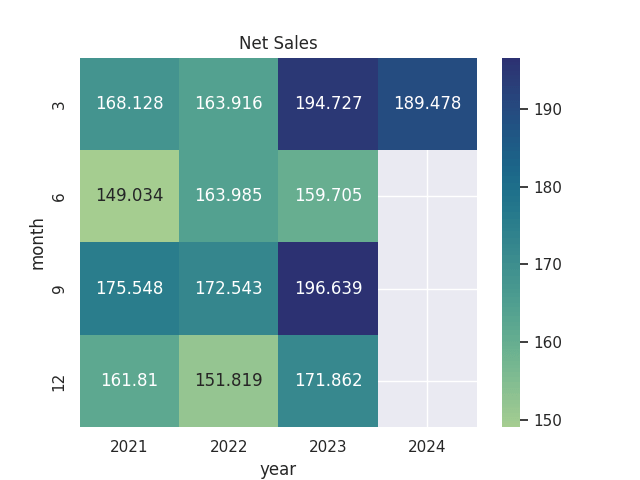

In terms of the trajectory of net sales for Motorcar Parts of America on a longer-term basis, we see that net sales were still higher than that of the quarter ended December 2023 and the third-highest quarter in net sales since the quarter ended March 2021.

Net sales figures (in US$ millions) sourced from historical quarterly reports for Motorcar Parts of America. Heatmap generated by author.

However, diluted net income per share remained in negative territory – with a net loss of -$0.03 per share on a three-month ended basis and a net loss of -$2.51 per share on a year-ended basis.

Motorcar Parts of America Reports Year-End Results: June 11, 2024

From a balance sheet standpoint, we can see that the quick ratio for Motorcar Parts of America (calculated as total current assets less inventories less prepaid expenses and other current assets all over total current liabilities) has been significantly below 1 in the most recent quarter and the prior year quarter, indicating that the company does not possess sufficient liquid assets to meet its current liabilities.

| Mar 23 | Mar 24 | |

| Total current assets | 537478000 | 560459000 |

| Inventory – net | 339675000 | 377040000 |

| Prepaid expenses and other current assets | 20150000 | 18202000 |

| Total current liabilities | 382592000 | 404425000 |

| Quick ratio | 0.46 | 0.41 |

Source: Figures sourced from Motorcar Parts of America Reports Year-End Results: June 11, 2024. Quick ratio calculated by author.

When analysing the company’s balance sheet, it is also notable that accounts payable is up by almost 30% since the prior year quarter.

Motorcar Parts of America Reports Year-End Results: June 11, 2024

This could reflect an increase in raw material costs – which the company cites as having the potential to affect the cost of products and negatively impact profitability. The company also states that fiscal 2024 was marked by increased costs of raw materials and finished goods, as well as higher labor costs in Mexico, and higher administrative costs.

Overall, we have seen that net sales have seen a slight decrease from that of the prior year quarter, but diluted earnings per share has yet to rebound into positive territory.

Looking Forward and Risks

In terms of growth prospects for Motorcar Parts of America going forward, the company has cited that ordering activity has shown increased momentum, while industry fundamentals are also in a good position to drive product demand.

On the margin side, this has been enhanced by multiple rounds of price increases, while the company has also seen further momentum in its brake-related business. In this regard, net sales could have the capacity to exceed that of the prior year in subsequent quarters.

As concerns auto sales in the US more generally, continually high interest rates as well as high prices have meant that sales growth has been modest – with May light vehicle auto sales projected to be up by 3% from the year-ago total, according to S&P Global Mobility.

In this regard, this could mark a potential opportunity for Motorcar Parts of America to sustain sales growth – as one would expect demand for aftermarket parts to increase as consumers try to keep their older vehicles running for longer.

However, rising auto insurance in the United States continues to pose a risk to demand – with the average cost of motor insurance having risen by over 20% from February 2023 to February 2024. Moreover, US auto insurance rates are currently at their highest level in over 50 years.

In this regard, we could see a situation where drivers either stop using or greatly reduce the usage of their vehicles – which would also be expected to decrease demand for aftermarket parts.

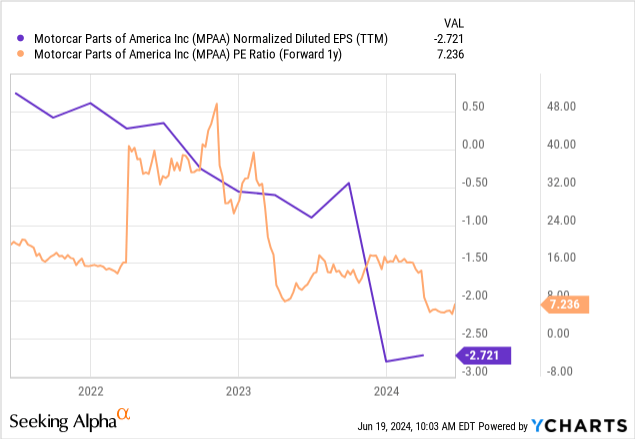

When looking at the company’s P/E ratio, we see that while the same is at a three-year low, earnings per share is also in negative territory.

ycharts.com

In this regard, I take the view that attempting to value the stock at this time is not appropriate until we see earnings rebound into positive territory.

Ultimately, I take the view that the outlook for the market remains uncertain, and will be looking to see whether net revenue has the capacity to rebound from here, and whether earnings can follow suit.

Conclusion

To conclude, Motorcar Parts of America has seen some downward pressure on sales in the most recent quarter. In my view, the outlook for net sales and the overall market remains uncertain, and I thus rate Motorcar Parts of Americas as a Hold at this time.

Read the full article here