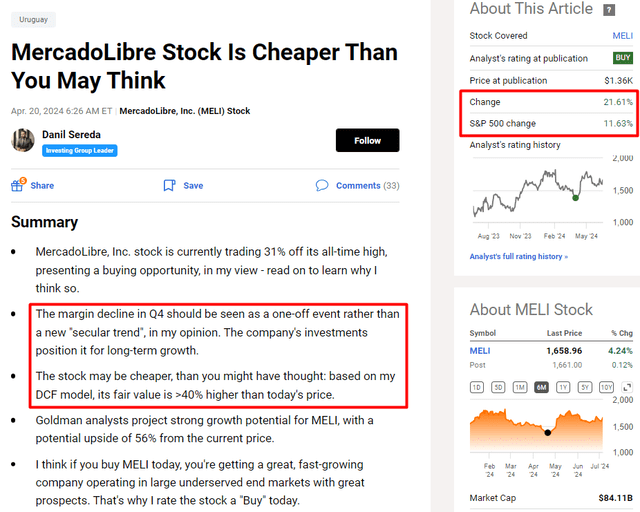

About three months ago, I published my first article on MercadoLibre (NASDAQ:MELI), whose shares were trading around $1,360 apiece at the time. I was of the opinion that the contraction in margins in the fourth quarter was probably a one-off event and that the company was very well positioned for the long term with its investments. My discounted free cash flow valuation model [DCF] indicated an undervaluation of at least 40%. Over the last three months, the stock is up 21.6%, almost twice as much as the broad market index S&P 500 (SP500) (SPY). I was lucky enough to basically “catch the local low” in MELI 3 months ago:

My previous article on MELI

Today, after updating my DCF model and reviewing the company’s latest financials, my opinion remains unchanged: I believe that MELI’s growth investments in recent quarters and the momentum of its business acceleration point to continued growth for MercadoLibre stock. Therefore, I’m updating my rating and remaining bullish on the company.

Why Do I Think So?

In case you hear about MELI for the first time, let me give you a little description. MercadoLibre is an $84-billion market-cap e-commerce ecosystem online and leading fintech platform – the biggest of its kind in Latin America – operating in 18 nations such as Argentina, Brazil, and Mexico. It has its safety shopping cart software that securely takes care of all kinds of merchandise transactions for consumers and sellers, thus making it a popular choice where over 650 people reside. In addition to granting individuals digital accounts, debit cards, online payments, insurance policies, savings vehicles, investments, and personal credit lines; MercadoPago also offers payment processing solutions to merchants.

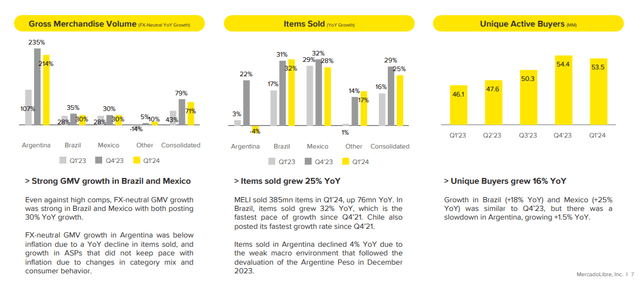

Looking at the latest quarter results (Q1 FY2024), we see that MELI reported a total revenue of ~$4.3 billion, a 36% increase from the previous year. What seemed interesting to me was the fact that in Brazil and Mexico, MELI’s gross merchandise volume (GMV) surged by ~30% YoY, fueled by “enhanced user experience, strategic infrastructure investments, and successful marketing efforts”, as the management commented during the earnings call. Why it was interesting to me? Because I think it’s important to understand here that MercadoLibre is already a major player in Latin America, and such a substantial GMV growth over just one year looks stunning.

MELI’s IR materials

The company’s advertising sector and its fintech division, MercadoPago, also saw significant gains: Notably, the acquiring business, credit portfolio, and TPV experienced remarkable growth, with TPV hitting $1.9 billion, marking a 133% increase from the previous year. Although the total operating profit margin declined by 395 basis points YoY to ~12.2%, net income rose to $344 million, marking a 71.14% YoY increase, beating the consensus estimates by a really wide margin.

Seeking Alpha, author’s notes

After the company presented its Q1 results, however, analysts had a somewhat mixed impression – the estimates for the next quarter, which the company is set to publish on August 2, have changed upwards and downwards in roughly equal measure. In other words, estimates have not increased significantly overall, suggesting that analysts aren’t particularly optimistic bullish on MELI’s upcoming Q2 report.

In my opinion, Mercado Libre has significant positive attributes that analysts should appreciate.

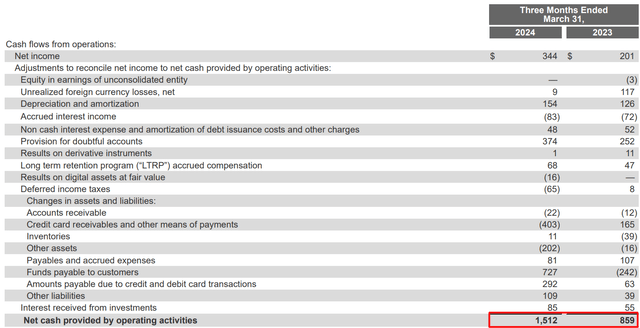

First, I’m impressed by the growth trajectory of its operating cash flow. Being essentially a smooth transition from net income, MELI’s OCF is almost double that of last year, indicating that Mercado Libre’s operations are quite effective if it can generate such substantial cash flow growth. This is a very critical characteristic for any prospective investor, in my view.

MELI’s cash flow statement, the author’s notes added

Second, despite some skepticism about the recent decline in margins, it appears that the company’s investment projects are actually bearing fruit and leading to higher top-line growth.

I like the management’s focus on improving the user experience and making strategic investments in infrastructure, especially in fast-growing areas. Going forward, I believe MELI’s well-executed marketing campaign will leverage the publicity generated during the peak season to generate more interactions, as the management expects (based on the earnings call commentary). In addition, the advertising business should continue its growth trajectory by achieving regular GMV penetration in all markets.

Third, I believe MercadoPago – MercadoLibre’s fintech arm – should drive further high-quality (i.e. profitable) growth in the future quarters. According to the latest IR materials, MercadoLibre’s fintech division’s MAU increased by 38% YoY, with Brazil leading the growth; Argentina also showed good momentum due to the strong value proposition of Mercado Pago amidst high inflation. The total assets under management amount grew by 90% YoY, with Brazil and Mexico more than doubling, and Argentina showing strong growth both annually and quarterly. The credit portfolio expanded by 46% YoY, driven by a 132% increase in the credit card portfolio (particularly in Brazil and Mexico). Despite a 43% YoY decline in Argentina’s credit portfolio due to the devaluation of the peso, it began to grow again on a quarterly basis, which is also a good sign. So from what I see, MercadoPago is focused on maintaining its strength in Mexico and Brazil through a growing acquiring business and credit portfolio. So the growth of the company’s fintech segment is therefore likely to accelerate further. I like that even significant macroeconomic challenges in certain regions of Latin America haven’t hindered MercadoLibre’s growth in these areas (so we may assume that a stabilization of the macroeconomic environment could further accelerate growth).

Fourth, MELI also seeks to enhance its logistics network via the Meli Más program, thereby improving efficiency and involvement: The largest e-commerce platform in Latin America aims to strengthen its delivery capabilities. In my point of view, MELI’s margins should also get better over a number of quarters through the optimization of logistical processes. With these margins leveling out we can start to expect the acceleration of operating profit growth, which is likely still not priced in.

To be fair, however, it should be noted that not all Wall Street analysts hold the seemingly neutral sentiment. Analysts at Jefferies gave MercadoLibre a “Buy” rating backing May 2024, forecasting that the company’s revenue will triple by the end of 2024 compared to its peak in 2021. Jefferies has set an upwardly revised target price of $2,000 while increasing its 2024 revenue projection by 10% and its 2026 estimate by 15%.

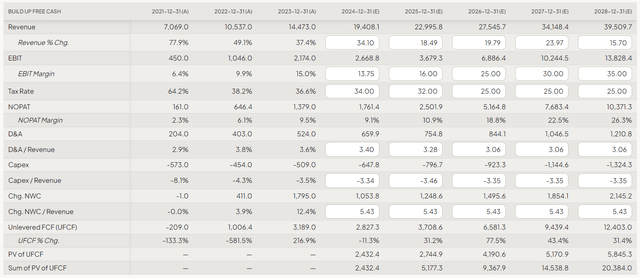

Let’s focus on the consensus first and adjust it to reflect the most realistic developments for the next few years. I will only use the sales forecasts and take them as the ultimate truth. Why? As I noted in my previous article, this approach is in line with the principle of conservatism, as the company has only missed its sales estimates once since 2012.

For the EBIT margin, I expect a smooth transition to a margin of 35% by the end of the forecast period (FY 2028). Other key figures, such as the ratio of D&A to sales or CAPEX to sales, will be in line with historical norms. In addition, the effective tax rate in my model will gradually return to the level of many years ago (25%). Here’s the result of my calculations at this stage:

FinChat, MELI, the author’s notes

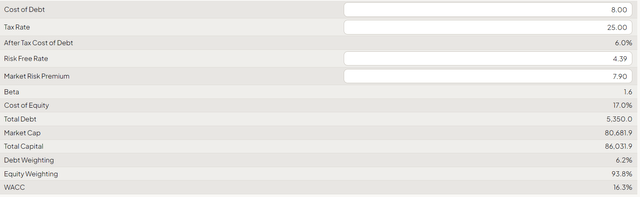

Getting to the discount rate calculation part, I’ll simply assume that MELI’s current borrowing rate is ~8% and that the large variation between the risk-free rate of 4.39% is caused by geographical risk. In addition, the MRP will also be above its typical figure of 5% (at 7.9%) as there are higher expectations among investors theoretically since they have to choose non-American equities in order to earn high returns. As a result, it gives a WACC of 15.4%, which might seem too much; nevertheless, bear in mind that this company is still growing quickly, and it has huge risks involved.

FinChat, MELI, the author’s notes

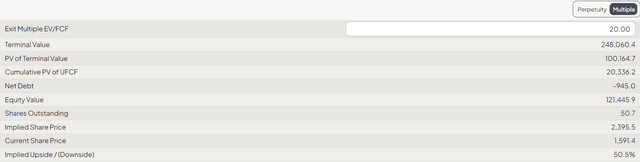

Next comes a tricky assumption: the terminal value calculation. FinChat’s template model that I use only allows us to use the EV/FCF ratio, and by that measure, MELI looks very cheap today: The COVID period distorts the long-term view, but the current multiple of 15x (vs. Amazon’s (AMZN) 44x as of today) shows that the multiple has dropped significantly in the last year. Just as before, I believe this multiple will rise as the company’s margins improve – with better margins, we’ll have more visibility into FCF, which the market should appreciate. Therefore, I’ve set an EV/FCF multiple target of 20x by FY2028. All of the above forecasts lead me to conclude that the company’s shares have become even more undervalued since my last model update. Despite the stock’s growth of more than 20%, the current undervaluation stands at 50.5%, which is quite significant. This suggests a price target of almost $2,400, well above Jefferies’ May estimate of $2,000:

FinChat, MELI, the author’s notes

As you see, MercadoLibre somehow became even more undervalued over the past 3 months despite its recovery rally. Therefore, I reiterate my bullish rating, believing that the recovery we saw recently is just the beginning of a greater long-term rally in the stock price.

Where Can I Be Wrong?

I admit that we shouldn’t ignore some very important risks to my today’s thesis. First off, currency fluctuations, particularly if the Argentine Peso devalues, could impact MELI’s financial results and challenge my expectations for margin expansion. Similarly, the firm’s lending operations face risks if borrowers struggle to repay loans, leading to higher costs and deteriorating credit quality. Also, among other things, intense competition in the payments sector might require increased spending on customer acquisition and could result in slower growth. This means the consensus revenue and EBIT figures I’ve assumed in my DCF update might not fully support my conclusions.

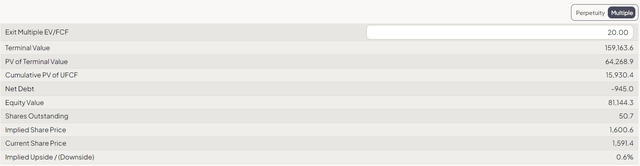

To be honest, the biggest risks in my valuation model come from the assumptions about the company’s future operating profit margin. If we assume that the margin stabilizes at 20% by 2028 instead of 35%, the undervaluation of the company would disappear if all other factors remain the same. This is what the fair value calculation would look like if we assume that the margin peaks at 20% by the end of 2028.

FinChat, MELI, the author’s notes

So if you agree with my conclusions, you should also agree with my assumptions about the company’s EBIT margins. If you have a different perspective on that, then MercadoLibre may be too risky for you as a long-term investment, so think twice, and please do your own due diligence (as you always should).

The Verdict

Despite the risks described above, I’m quite optimistic about MercadoLibre’s strategic trajectory and business momentum in recent quarters. The company is investing heavily to capture as much of the Latin American market as possible. The environment is highly competitive, but judging by recent growth rates, MercadoLibre appears to be achieving its goals in most areas. This is crucial for the long-term growth prospects.

I appreciate that the company remains cash flow positive (the OCF is expanding rapidly) and has high growth rates despite its scale. Furthermore, Latin America is expected to grow significantly in the coming years, providing a solid base for MercadoLibre to maximize its projects. According to my DCF valuation model, the company is currently undervalued by 50.5% – this significant undervaluation is hard to ignore, although it is based on some risky assumptions that I firmly believe in. I think the company can reach an operating profit margin of 35% by the end of 2028 – if this rapid margin expansion materializes along with relatively conservative assumptions for other factors, the stock could indeed rise to $2,300-$2,500 in the next few quarters.

My technical analysis suggests a bullish outlook for MercadoLibre. The seasonality of MELI stock is favorable, as July has been the most profitable month in the last 10 years, giving hope that this July will also be positive. This short-term perspective is complemented by a long-term view: significant resistance levels need to be overcome on the weekly chart, but the overall trend remains bullish as the price stays firmly above the 52-week moving average.

TrendSpider Software, MELI, the author’s notes added

I believe that this long-term uptrend will continue. Hence, my “Buy” rating upgrade today.

Thank you for reading!

Read the full article here