Investment thesis

My initial bullish thesis about Medtronic (NYSE:MDT) aged somewhat good as the stock delivered a total 1.9% return since mid-February. As I underlined in my initial thesis, MDT is a good option for investors seeking low-volatility stock with solid dividend growth.

The company reports its fiscal Q1 earnings soon, on August 20. Today I want to update my thesis and explain why I believe there are robust reasons to remain moderately bullish about MDT. Moreover, the valuation still looks good. All in all, I reiterate my “Buy” rating for MDT.

MDT FQ1 earnings preview

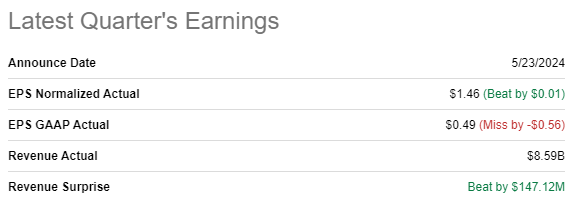

MDT released its latest quarterly earnings on May 23, surpassing revenue and adjusted EPS consensus estimates. On the other hand, there was a big miss against consensus from the perspective of GAAP EPS. Revenue was almost flat YoY with a shallow 0.5% growth.

Seeking Alpha

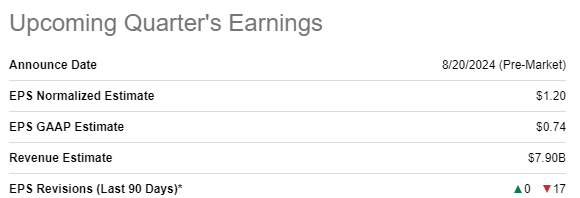

The upcoming quarter’s earnings are scheduled next week, for August 20. Wall Street analysts expect FQ1 revenue to be $7.90 billion, around 2.5% higher on a YoY basis. The adjusted EPS is expected to be flat YoY at $1.2. Sentiment of Wall Street analysts around the upcoming earnings release is quite bearish with 17 downgrade EPS revisions over the last 90 days.

Seeking Alpha

MDT has a solid earnings surprise record and several previous quarters there were only positive revenue and adjusted EPS surprises. What is also important is that the stock is rarely a big mover after earnings releases, according to historical share price movements.

Recent developments are mostly positive for MDT investors. The company declared a $0.70 quarterly dividend on August 16, in line with the previous one. Moreover, MDT got upgraded from “Sell” to “Hold” by UBS analysts, with optimism around the ability to drive growth in the company’s diabetes segment. The optimism looks sound since the industry is expected to demonstrate solid growth. According to Statista, diabetes care devices industry is expected to deliver a 12.2% CAGR between 2024 and 2029, which is a solid tailwind for MDT’s diabetes business. Moreover, Medtronic has recently won an FDA approval for its Simplera continuous glucose monitor [CGM].

Parkinson’s Foundation

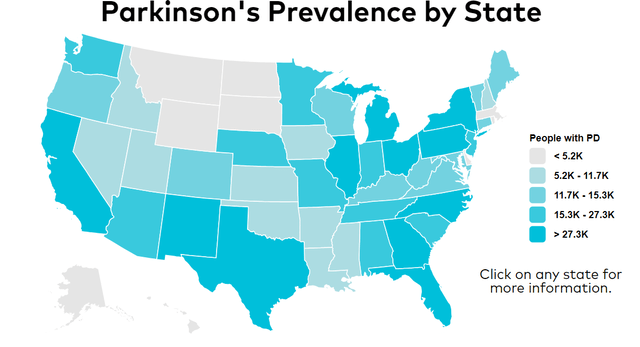

Recent information also suggests that Medtronic received another important FDA approval for its asleep deep brain stimulation [DBS] surgery. Medtronic claims that it has become the first and only company getting an FDA approval to conduct DBS surgeries. The DBS surgery solution is for people with Parkinson’s disease and with essential tremor. This is also a crucial positive development for MDT as Parkinson’s disease is also a big problem in the U.S. According to Parkinson’s Foundation, nearly 90,000 people in the U.S. are diagnosed with this disease each year and the combined direct and indirect cost of Parkinson’s is estimated to be nearly $52 billion per year in the U.S. alone.

All these developments are crucial for the company’s long-term revenue prospects. The good part is that the management is not also focused on driving revenue growth, but also expand value for shareholders. The company restructured its facilities, which allowed it to optimize the headcount in 2023. According to news as of mid-June 2024, the company continues laying off employees.

Valuation update

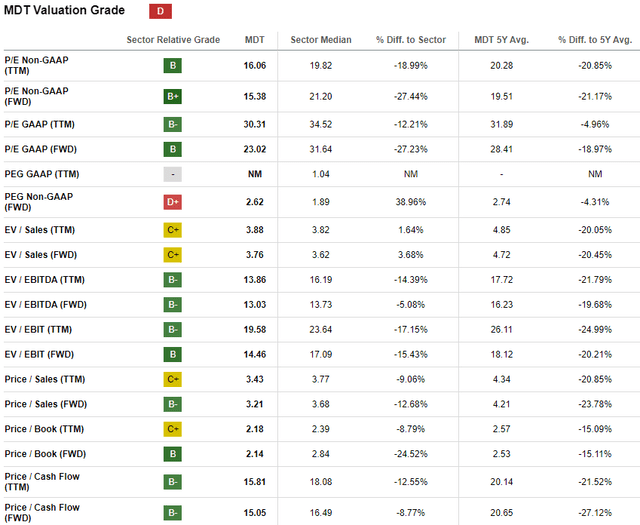

MDT demonstrated a modest 3.7% share price increase over the last twelve months, and the 52-week range varied between $69 and $89. The stock’s performance has lagged behind the broader U.S. market and the Health Care sector (XLV) over the last 12 months. Seeking Alpha Quant assigns MDT a low “D” valuation grade mainly due to the massive forward PEG ratio, but other ratios look attractive. What is crucial is that most of the valuation ratios are notably lower than MDT’s historical averages.

Seeking Alpha

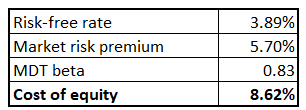

Since MDT is a mix of a growth and value stock, in my opinion, simulating both the dividend discount model [DDM] and discounted cash flow [DCF] approaches will be sound for my valuation analysis. I will use an 8.62% discount rate for both models, which was figured out using the CAPM approach below.

Author’s calculations

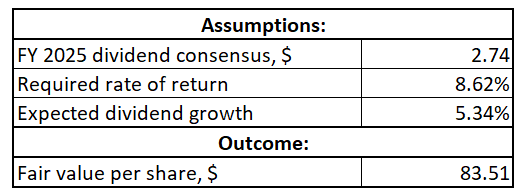

MDT has an exceptional dividend consistency, which gives me high conviction that consensus dividend estimates are reliable to incorporate into my DDM. That said, I use an FY 2025 $2.74 projection. MDT also has a solid dividend growth record, but to be on the safe side, I use the last three-years’ dividend CAGR of 5.34%. According to my DDM analysis, the stock’s fair price is $83.5. This is very close to the current share price, meaning that MDT is approximately fairly valued.

Author’s calculations

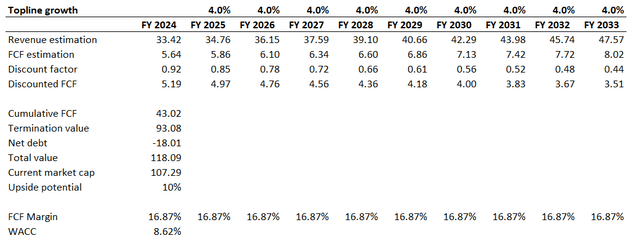

Now I will proceed with the DCF simulation. I use a 54% revenue CAGR for the next decade, which looks like a fair deceleration compared to the last decade’s 7% rate. Moreover, my projected revenue growth rate is approximately in line with the revenue consensus estimates. I use a flat 16.87% FCF margin, which is the TTM level. To be conservative, I will also deduct from my fair value calculation the current $18.01 billion net debt position.

Author’s calculations

According to my DCF simulation, the business’s fair value is around $118 billion. This is 10% higher than the current market cap, meaning that DCF meaning that MDT is attractively valued from the perspective of future cash flows.

Risks update

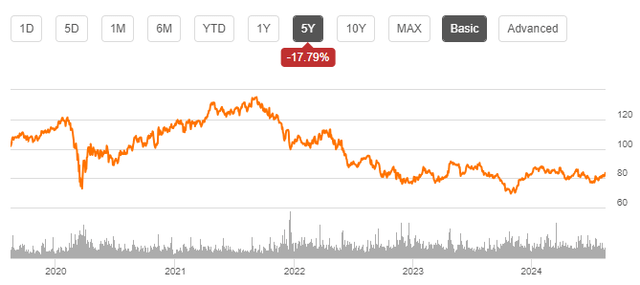

The stock price declined by 17.8% over the last five years, meaning it was not a good choice for investors who were seeking capital gains apart from the solid dividend growth. Potential investors, especially those targeting growth, should be ready for “boring” share price dynamics. On the other hand, considering the length of the timeframe below, we can see that the stock has been trading in a relatively narrow corridor and is currently much closer to the lower edge of the range, which increases the probability of a rebound to higher levels in the short term.

Seeking Alpha

The major business risk that I see is the fierce competition. There are numerous competitors in the Health Care Equipment industry, which are approximately of the same market cap as MDT, which includes Boston Scientific Corporation (BSX), Stryker Corporation (SYK), and Intuitive Surgical (ISRG). I will not dig deep into comparisons of offerings of each company because the environment and technologies are rapidly evolving, and I would better look from the perspective of financial metrics and their dynamics.

Seeking Alpha

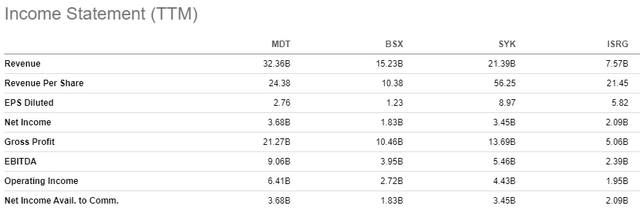

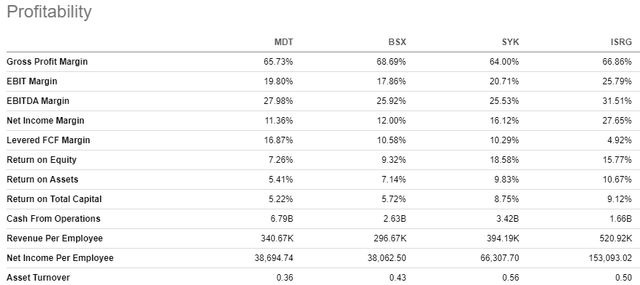

Despite the fact that the market caps of all these companies are not very far from MDT’s, we can see that Medtronic is far larger from the perspective of revenue. Such an inconsistency between the differences in market cap and revenue highly likely means that investors perceive MDT as weaker than peers. Indeed, from the perspective of profitability ratios, I cannot call MDT an undisputed leader as it lags behind competitors across some metrics.

Seeking Alpha

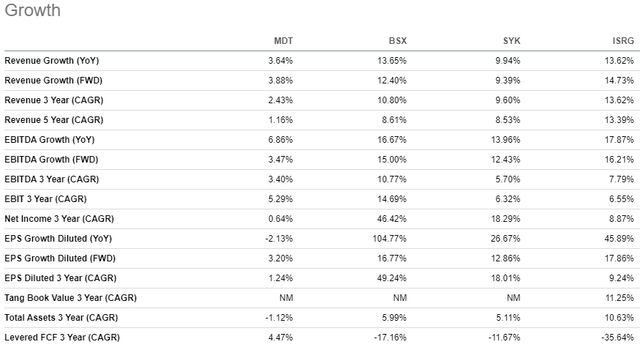

Moreover, MDT demonstrates a much more modest revenue growth than its peers. While investors apparently highly value growth dynamics and prospects, I do not think it is a big red flag for MDT. First, the company is still by far the largest from the perspective of revenues and operating cash flows generated, meaning that MDT generates more resources to reinvest into business in absolute terms. Second, the management’s efficiencies initiatives are working, which we have seen in the financial analysis, which means that MDT will close the gap in terms of profitability metrics compared to the competition.

Seeking Alpha

Bottom line

To conclude, I believe that MDT is still a “Buy”. Recent developments are quite positive and historical share price movements suggest that buying this stock before earnings is not very risky. Moreover, the valuation is still attractive.

Read the full article here