Is there a stock universe where Tech and Life Sciences, which are traditionally low dividend payers, intersect with high dividend stocks?

As it happens, yes there is, in the form of a Business Development Company, a BDC, known as Horizon Technology Finance (NASDAQ:HRZN), which focuses on these 2 sectors.

We previously wrote about HRZN in a late September ’23 article, where we rated HRZN a speculative Buy, “based on its floating rate exposure, its very well-covered yield, its low P/NII, and its long-dated debt maturities.”

Since that article, HRZN moved from $11.88 to $12.00, and paid an $.11 regular monthly distribution, for a 1.9% return in ~6 weeks. Its P/NAV valuation is now twice as high, while its P/NII valuation is a bit lower. (See Valuations section for more detail.)

What’s New:

HRZN reported Q3 ’23 earnings on 10/31/23.

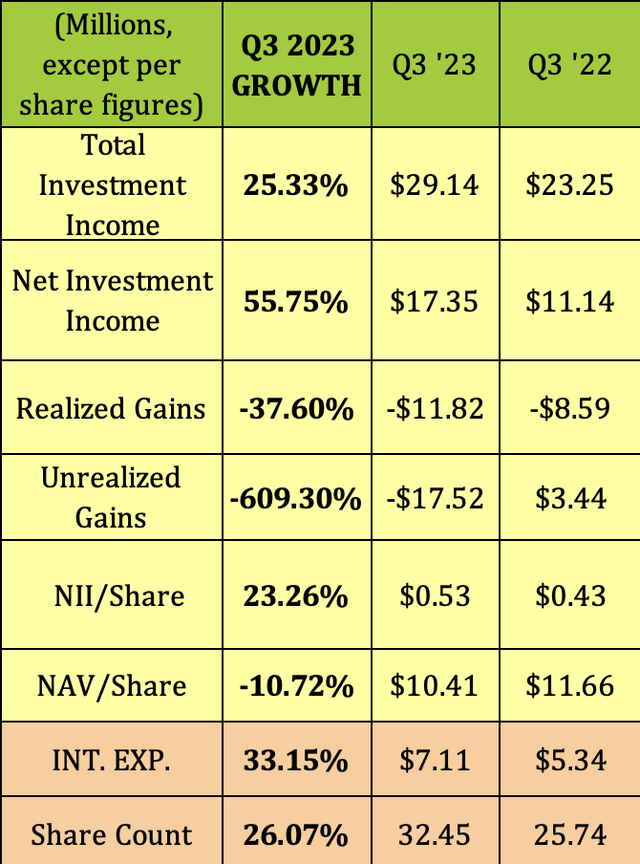

Q3 ’23 was a big growth quarter for HRZN, with total Investment Income up 25%, NII up ~56%, and NII/Share up 23%, with the share count rising 26%. Interest expense rose 33%, to $7.1M.

However, Realized Gains were in the red, at -$11.8M, up 37% from $8.6M in Q3 ’22, while Unrealized Gains also worsened, to -$17.5M, vs. a positive $3.4M in Q3 ’22.

One portfolio company, Evelo Biosciences, had 2 unfavorable trial outcomes during 2023, including a failed Phase 2a trial for a psoriasis drug 2923 in October. This resulted in a significant unrealized loss on our Evelo debt investment in Q3. However, in early Q4, HRZN received an additional cash paydown of $11M from Evelo. It also got a $5 million paydown from Evelo early in Q3, bringing the total of Evelo’s principal repayments to $16M in 2023.

Hidden Dividend Stocks Plus

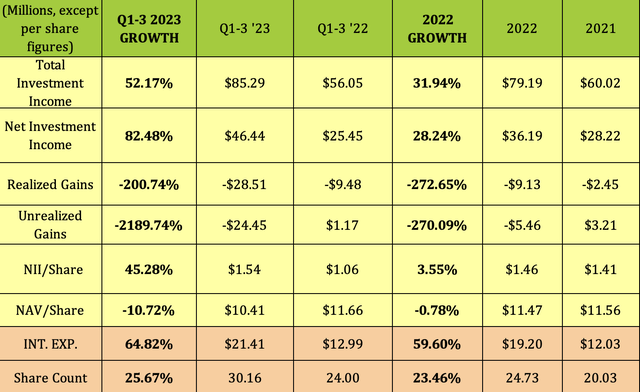

Looking at Q1-3 ’23 figures shows HRZN’s Realized and Unrealized Gains have gone deeper into the red in 2023, (like some other BDCs’), as some of the underlying companies struggle with higher rates, and other challenges.

Q1-3 ’23 Realized Gains were -$28.51M, over 3X the -$9.13M full year 2022 figure; while Unrealized Gains went from -$9.13M in 2022, to -$28.51M.

On the positive side, a bigger portfolio and higher interest rates created strong revenue growth, up 52%, and even stronger income growth, with NII up 82.5%, and NII/Share up 45.3%, as NII outstripped a 65% rise in interest expense.

Hidden Dividend Stocks Plus

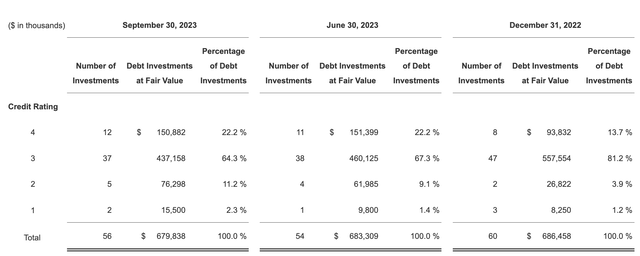

Like other BDC’s, HRZN’s management rates its debt portfolio companies quarterly. 4 is the highest tier – 1 is the lowest. As of 9/30/23, its debt portfolio consisted of 56 companies, up 2 in the quarter, with 86.5% rated in the top 2 tiers, vs. 89.5% at the end of Q2 ’23.

Its bottom rating, Tier 1, rose to $15.5M, 2.3%, vs. $9.8M in Q2 ’23; and Tier 2 rose from ~$62M, 9.1%, to $76.3M, 11.2%.

Historically, HRZN has a low annual net loss rate of 10.0bps or 0.10% of the value of its portfolio.

HRZN site

Valuations:

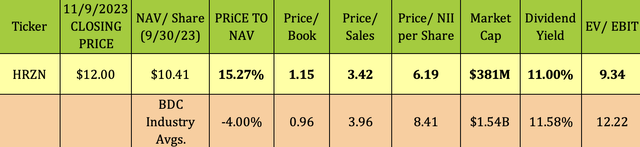

As of the 11/9/23 close, HRZN was selling at 15.3% premium to its $10.41 NAV/Share, vs. an overall BDC 4% discount to NAV. That’s up considerably vs. its 9/29/23 P/NAV premium of 7.32%, when we last covered HRZN.

Over the past year, HRZN has ranged from as low as a ~4% discount to NAV during the March banking mini-crisis, up to a ~20% premium.

HRZN does look undervalued on an earnings multiple basis – its P/NII of 6.19X is much lower than the 8.41X BDC industry average, and is a bit lower than its previous 6.46X valuation, (based upon ttm earnings through Q2 ’23.).

Its EV/EBIT of 9.34X is also much lower than the industry average. Its 11% dividend yield is roughly in line with the industry average.

Hidden Dividend Stocks Plus

Performance:

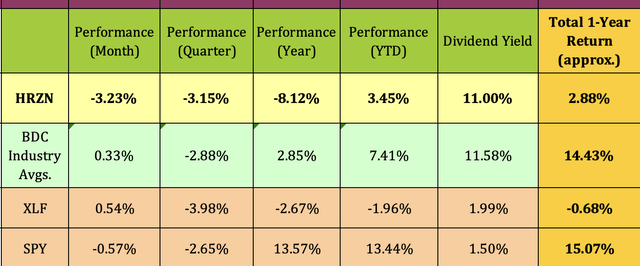

Tech took a beating in 2022, with the advent of rising interest rates, taking many tech-focused investments down with it. HRZN’s price performance has trailed the BDC industry’s average, the broad Financial sector, and the S&P 500 over the past year.

HRZN has done a bit better than the Financial sector so far in 2023, but still trails the BDC industry and the S&P. Meanwhile, Tech is up ~39% in 2023, while Healthcare is down ~7%.

Hidden Dividend Stocks Plus

Company Profile:

Horizon Technology Finance Corporation (HRZN) is managed by its advisor Horizon Technology Finance Management LLC, an affiliate of Monroe Capital (MRCC). Since 2004, Horizon has directly originated and invested more than $3 billion in venture loans to more than 315 growing companies. (HRZN site)

HRZN’s $680M debt portfolio holds 56 companies, with exposures of 40% each In Tech and Life Sciences, 12% in Sustainability-related companies, and 8% in Healthcare Information Services.

Its transaction size is generally up to $50M, in Term, bridge, or special purpose loans, with a 3-5 year term. It takes a priority interest over equity and unsecured debt; and also invests in Warrants/success fees – it has a portfolio of warrant, equity and other investments in 102 companies with an aggregate fair value of $49M.

The majority, 63%, of its investments are in expansion stage companies, with 29% in early stage, and 8% in later stages of development.

Software, at 22%, is its largest sub-sector exposure, followed by Biotech, which decreased from 26% to 20% in Q3 ’23. The remaining sub-sectors were roughly static, excepting Health Software, which increased from 4% to 7%.

HRZN site

Dividends:

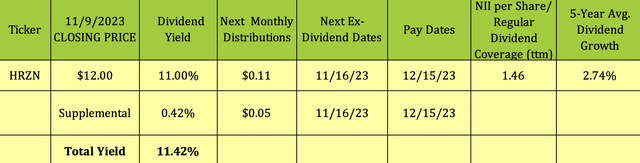

HRZN declared a regular $.11 monthly distribution, and a $0.05 supplemental payout, both of which go ex-dividend this week, on 11/16/23, with a 12/15/23 pay date.

HRZN’s base dividend yield is 11%, while the 1-time $.05 payout adds 0.42%, for a total yield of 11.42%.

HRZN has paid out $17.77/share in distributions since its 2010 IPO. Its 5-year dividend growth annual average is 2.74%.

Hidden Dividend Stocks Plus

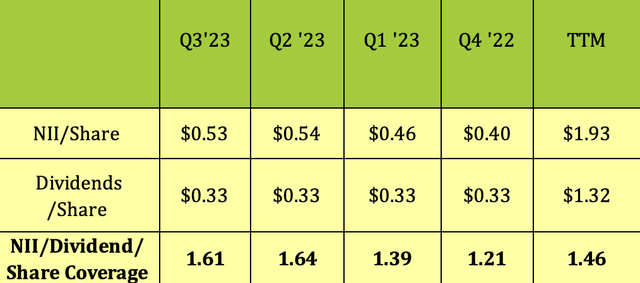

HRZN has one of the strongest dividend coverage factors in the BDC industry. Coverage topped 1.6X again in Q3 ’23, giving it a trailing average of 1.46X:

Hidden Dividend Stocks Plus

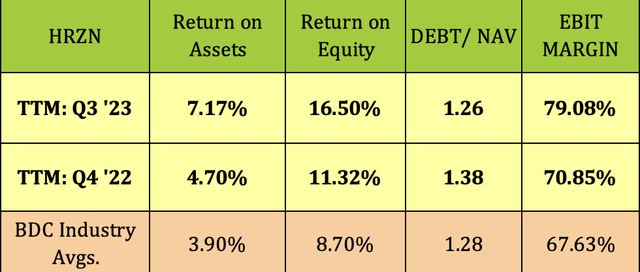

Profitability & Leverage:

HRZN’s profitability has improved in 2023, with ROA, ROE, and EBIT Margin all up significantly, and remaining above BDC industry averages. Debt leverage in in line with the BDC industry average.

Hidden Dividend Stocks Plus

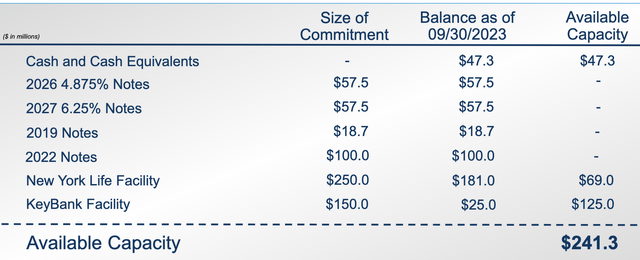

Debt & Liquidity:

As of 9/30/23, HRZN had $241.3M in available liquidity consisting of $47M in cash, and $33M in funds available under its existing credit facilities.

On June 29, 2023, management amended the KeyBank Facility, to increase the commitment amount to $150M, and to increase the amount of the accordion feature, which now allows for the potential increase in the total commitment amount to $300M.On May 24, 2023, the Company amended the NY Life facility, to increase the commitment by $50M.

HRZN site

Analysts’ Price Targets:

On 10/17/23, Compass Point downgraded HRZN from Neutral to Sell, with a $10.00 price target. That was ~3 weeks after Compass upgraded HRZN in late September from Sell to Neutral with a $10.50 target. Confusing, eh?

The low price target is now $9.25, vs. $10.50 in late September.

At its 11/9/23 closing price of $12.00, HRZN is 3.5% above Wall St. analysts’ average price target of $11.59, and 20% below the highest target of $15.00.

Hidden Dividend Stocks Plus

Parting Thoughts:

At its 12/9/23 closing price of $12.00, HRZN was ~10% below its 52-week $13.45 high, and ~18% above its 52-week $10.14 low. It’s approaching an overbought indication on its slow stochastic chart.

While earnings have been very strong in 2023, realized and unrealized losses are a concern. We rate it a Hold at this point, due to a much higher P/NAV, and these other issues. There may be lower entry points in the future.

If you’re interested in other high yield vehicles, we cover them every Friday and Sunday in our articles.

All tables furnished by Hidden Dividend Stocks Plus, unless otherwise noted

Read the full article here