Ford Motor Company (NYSE:F), the world’s sixth-largest multinational automaker that markets vehicles under the Ford brand, encompassing both automobiles and commercial vehicles, as well as luxury automobiles under the Lincoln brand, released its third-quarter earnings results, which has disappointed investors with its misses on both lines, suspension of its 2023 financial guidance, as well as the pause on $12 billion EV investment.

The company has witnessed a decline of over 10% in market value since the beginning of October 2023, reaching its lowest point since January 2021, following the earnings announcement where Ford withdrew its adjusted EBIT guidance for FY 2023.

TradingView

Ford stock reached last week its lowest point since January 2021

Investment Thesis

Ford’s business continuously grapples with challenges, particularly in the current landscape marked by the evolution of the electric vehicle market, the emergence of new global competitors from China, and the disruptions caused by both technological advancement, supply chain, as well as the labor strike in its factories, which is rather short-term.

The company’s leadership stated that they suspended the 2023 guidance because they were awaiting the final ratification of their tentative agreement with the United Auto Workers, which had been reached on October 25. Chuck Browning, the UAW Vice President who served as the primary negotiator with Ford, announced that workers will receive a 25% general wage raise, along with cost-of-living adjustments that will push the total pay increase beyond 30%. This will result in top-scale assembly plant workers earning over $40 per hour by the end of the contract.

While the tentative labor agreement with the United Auto Workers is introducing uncertainty regarding its future earnings potential, this factor should not serve as a strong justification for long-term investors to question the viability of a positive investment thesis – compared to the change in the EV market that Ford has been betting on.

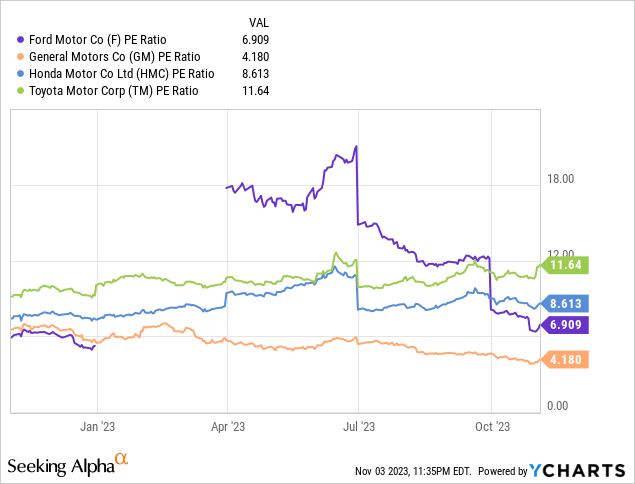

Despite ongoing losses in the EV division and the withdrawal of FY 2023 guidance, I still find Ford to offer an appealing value proposition at its current stock price. My investment thesis remains Bullish on Ford’s stock over the long term, the stock has an attractively low P/E ratio that currently stands below 6, and I firmly believe that Ford will continue to be one of the top six global automobile manufacturers in the foreseeable future.

Ford’s reported Q3 results

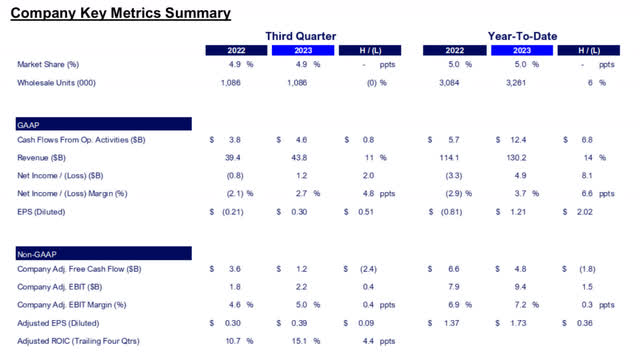

On October 26, Ford released its third-quarter earnings, which were a mixed bag and did not meet expectations. The company fell $1.34 billion short of revenue estimates and missed consensus EPS projections by $0.07 per share, primarily attributed to increasing losses in the EV segment. Ford’s Q3 adjusted earnings per share totaled $0.39 and even though total revenue of $43.80 billion was 11% up YoY, it missed analyst estimates by about $1.3 billion. Ford generated about $1.2 billion of profits during the third quarter, and it is noteworthy that the company’s profitability in that period was primarily driven by its traditional businesses, namely, Ford Blue and Ford Pro, which contributed profits of $1.72 billion and $1.65 billion, respectively.

Ford Earnings Release

On the other hand, in the third quarter, Ford’s electric vehicle division sustained significant losses, with a reported total adjusted EBIT loss of $1.3 billion, as opposed to a Q2’23 EBIT loss of $1.1 billion. Year-to-date, the electric vehicle division has accumulated total losses of $3.7 billion, resulting in a negative EBIT margin of 72.8% which indicates that Ford is incurring substantial losses on each electric vehicle sold. The EV segment will be discussed in detail in the coming section.

The UAW strike introduced substantial uncertainty surrounding Ford’s annual performance. To offer some perspective, during the third quarter, the strike had an EBIT impact of approximately $100 million. Additionally, the strike has resulted in a reduction of about 80,000 units in production so far, which could potentially decrease 2023 EBIT by around $1.3 billion.

At the close of the quarter, Ford possessed more than $29 billion in cash and had access to $50 billion in liquidity. This figure encompasses the newly established $4 billion contingent liquidity facility that Ford implemented in August to navigate the uncertainties prevailing in the current business environment.

EV sales surged 9.1% Y/Y in October, but is still losing money

Ford Motor witnessed a 5.3% year-over-year decline in its U.S. sales for October while experiencing a notable 9.1% increase in electric vehicle (EV) sales. The most recent data indicates that Ford sold 149,938 units in the U.S. during October but the encouraging news is that year-to-date (YTD) figures demonstrated a 7.7% rise, resulting in a total of 1,658,010 vehicles sold. Furthermore, the automaker achieved even more positive results in the EV sector as it experienced a 9.1% year-over-year increase in electric vehicle (EV) sales, reaching 6,831 units in October. This growth contributed to a year-to-date (YTD) increase of 12.6%. During a Q3 earnings conference call, Jim Farley, President and Chief Executive Officer, said that he is extremely bullish on the EV future but he also warned that a great product is not enough in the EV business anymore. Jim Farley, President and Chief Executive Officer of Ford, added:

We have to be totally competitive on cost. Tesla actually gave us a huge gift with a laser-focus on cost and scaling the Model Y. They set the standard, and we are now making real progress on our second- and third-cycle EVs that are in the midst of being developed today as we get closer to the introduction. While our Gen 2 EVs were targeting to deliver an EBIT margin comparable to ICE by 2026, the dynamic changes in the market, pricing, adoption rates, regulations are forcing us to further reduce the cost of our EVs.

President and Chief Executive Officer Jim Farley has identified that the essential components for achieving this competitive cost structure are scalability, vertical integration, and battery technology. In the third quarter, Ford’s electric vehicle division sustained significant losses but the company’s expanding scale and rising delivery volumes are expected to gradually reduce these losses in the future. Ford’s potential in the electric vehicle (EV) revolution is highly auspicious, primarily due to the company’s robust financial position. This financial strength equips Ford with the necessary resources to propel its ascent as a significant player in the global EV market.

Valuation

Despite certain apprehensions, Ford offers an enticing opportunity for investors with a long-term perspective. The company possesses a strong financial foundation and has the ability to effectively manage cost pressures, particularly when compared to smaller competitors, even amidst the persistent supply chain issues affecting the automotive sector. Ford distinguishes itself by achieving significantly higher profitability than many other automakers, and its shares are characterized by an appealing P/E ratio, which presently stands below 6, in contrast to the industry’s average P/E ratio, which is in the range of 8 to 10. Anticipating earnings of $1.80 per share for the upcoming year, Ford may potentially have a fair value that is more in the vicinity of $15, given its solid results and financial position.

Considering that the current share price is below $11, I believe Ford represents an exceptional bargain at this time. It is also important to mention that analysts from Barclays upgraded Ford Motor Company shares on Wednesday to an Overweight rating. Analysts have acknowledged that structural concerns are expected to persist for some time, but they are of the opinion that even a slight reversal of the strongly negative sentiment could lead to appealing upside potential. Barclays analysts have a $14 price target for shares of Ford which implies significant upside for potential investors.

Risk Factors

- Although Ford offers an appealing investment prospect, it is important to take into account various risk factors. Firstly, there is the potential for increased competition in the electric vehicle industry, as other automotive companies compete for a larger share of the market.

- Additionally, ongoing supply chain disruptions and semiconductor shortages may persist, leading to production disruptions and potentially limiting Ford’s ability to meet growing demand.

- Onwards, the recent agreement with the UAW will significantly affect Ford’s operations, potentially resulting in higher expenses and the potential for reductions in dividends. As part of the new agreement, Ford is set to implement an immediate 88% wage increase for its lowest-paid workers and an 11% increase for its top earners. The company has also pledged to raise wages by 25% over the next four years, enhance contributions to retirement savings plans to 10%, and transition temporary workers into permanent positions once the deal is officially approved.

- At the same time, the Federal Reserve will probably keep interest rates higher for longer and the majority of adverse outcomes resulting from elevated interest rates are yet to manifest. Additionally, the escalation of geopolitical tensions introduces another challenge and heightens the potential risks for financial markets and economic conditions.

Conclusion

Ford’s business consistently confronts obstacles, especially in the present environment characterized by the transformation of the electric vehicle (EV) sector, the emergence of fresh global competitors hailing from China, and the disruptions stemming from technological advancements.

Since the start of October 2023, Ford’s stock has seen a decrease of more than 10% in its market value, and in the previous trading week, it reached its lowest point since January 2021, following Ford’s withdrawal of its adjusted EBIT guidance for the fiscal year 2023. The tentative labor agreement with the United Auto Workers is introducing uncertainty regarding its future earnings potential, but this factor should not serve as a strong justification for long-term investors to question the viability of a positive investment thesis.

Despite certain apprehensions, Ford shares offer an enticing opportunity for investors with a long-term perspective and I firmly believe that Ford will continue to be one of the top six global automobile manufacturers in the foreseeable future.

Read the full article here