The best blood will at some time get into a fool or a mosquito. – Austin O’Malley.

Shares of blood disorder concern Disc Medicine, Inc. (NASDAQ:IRON) rallied strongly in 2023, buoyed by positive open-label data from its lead heme biosynthesis program bitopertin. Results from a placebo-controlled trial (due early 2024) should validate bitopertin’s open-label study, setting the stage for a registrational trial in either late 2024 or early 2025. With two other in-licensed assets in the clinic, a cash runway well into 2026, but a somewhat demarcated domestic peak-sales potential, Disc merited further investigation. An analysis follows below.

Seeking Alpha

Company Overview:

Disc Medicine, Inc. is a Watertown, Massachusetts-based clinical-stage biopharmaceutical concern focused on the development of therapies for serious hematological diseases. The company is advancing three clinical programs pursuing six indications. Disc was formed in 2017 and went public when it reverse-merged into failed ocular therapy concern Gemini Therapeutics, Inc. in December 2022, with its first trade executed at $20.89 a share. Its stock currently trades around $65.00 a share, translating to an approximate market cap of $1.55 billion.

Pipeline

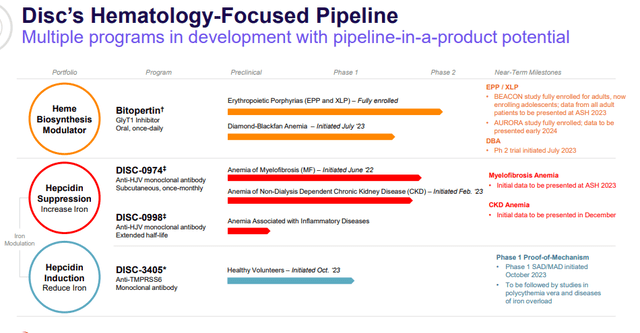

The company in-licenses its clinical candidates, which are designed to modify two biological pathways associated with the formation of red blood cells: heme biosynthesis and iron homeostasis.

December Company Presentation

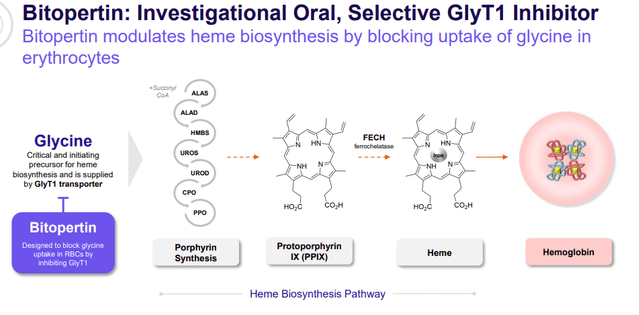

Bitopertin. The company’s lead program for heme biosynthesis is bitopertin, an oral inhibitor of GlyT1, which is a vital membrane transporter necessary for the supply of the amino acid glycine to developing red blood cells in support of their formation (erythropoiesis). Dysregulation of heme biosynthesis can lead to a buildup of toxic metabolites known as porphyrins, which can cause damage to the skin, gallbladder, and liver – diseases collectively known as erythropoietic porphyrias (EPs). Disc believes that the inhibition of glycine in newly forming red blood cells will limit the accumulation of porphyrins in instances of heme biosynthesis dysfunction. Enter bitopertin, which was in-licensed from Roche (OTCQX:RHHBY) in 2021 after failing to treat neurological disorders in clinical trials encompassing more than 4,000 patients. However, in those studies it was shown to reduce levels of GlyT1.

December Company Presentation

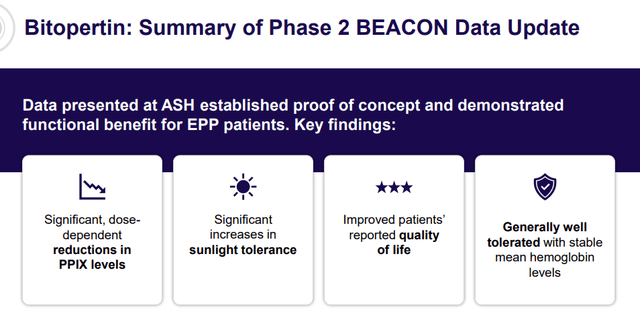

Bitopertin is undergoing evaluation in a two Phase 2 trials. BEACON is an open-label study initiated in Australia during July 2022 to assess bitopertin in the treatment of erythropoietic and X-linked protoporphyria (EPP and XLP, respectively) at 24 weeks. Both diseases are characterized by severe photosensitivity (and debilitating pain), as well as damage to the hepatobiliary system caused by the accumulation of toxic metabolite protoporphyrin IX (PPIX). Data (updated in October 2023) covering two dose cohorts have demonstrated significant dose-dependent reduction of whole-blood, metal-free PPIX levels (>40% overall; p<0.001; n=22). More importantly, light tolerance increases were observed in every patient, along with significant quality-of-life improvements (in nearly all cases). For what would likely be the primary endpoint of a pivotal trial, average cumulative pain-free hours in light over six months was three times higher in bitopertin patients versus historical control (222.6 hours versus 60.6 hours). Furthermore, bitopertin was well tolerated.

December Company Presentation

When initial data were released in June 2023, it triggered a two-day, 24% rally to $48.85 a share, which Disc used as an opportunity to raise capital – more on that below. Despite the dilution, shares of IRON have continued to rally and are up some 180% since the onset of 2023.

The other Phase 2 trial (AURORA) is a double-blind placebo-controlled study that initiated in October 2022 and encompasses 75 patients in the U.S. with a focus solely on EPP. Top-line data from this 17-week trial is anticipated in 1Q24. Given that there are no hiccups in the data, Disc will huddle with the FDA to determine protocol for a registrational Phase 3 trial, which would probably commence in late 2024 or early 2025.

If ultimately approved for EPP, bitopertin would enter a domestic treatment market of ~3,200 to ~6,100. Currently, Clinuvel’s (OTCPK:CLVLY) subcutaneously implanted melanocortin-1 receptor agonist Scenesse (afamelanotide) is the only approved therapy for EPP. The Australian-based competition produced revenue of ~$57 million (US) in the twelve months ending June 30, 2023, although it is unclear what portion of that was derived from U.S. sales of Scenesse. Other EPP therapies include steroids, Vitamin D, and narcotics. Also of note is Mitsubishi Tanabe’s Phase 3 oral melanocortin-1 program (dersimelagon).

Bitopertin is also undergoing Phase 2 evaluation in a study sponsored by the National Institutes of Health for the treatment of Diamond-Blackfan Anemia with its first patient enrolled in July 2023.

DISC-0974. Disc’s lead iron homeostasis program is DISC-0974, a once-monthly subcutaneously injected monoclonal antibody that inhibits the protein hemojuvelin, which in turn modulates iron regulator hepcidin. It is undergoing assessment in two Phase 1b/2 trials for the treatment of myelofibrosis anemia and non-dialysis dependent chronic kidney disease anemia. Designed to increase serum iron levels and enable red blood cell production, DISC-0974 was in-licensed from AbbVie (ABBV) in 2019. Early returns suggest DISC-0974 can induce a meaningful drop in hepcidin and an increase in iron. Additional proof-of-concept data are anticipated in 2024.

DISC-3405. The company’s other clinical program is DISC-3405, a monoclonal antibody targeting transmembrane serine protease 6, which elicits the exact opposite result of DISC-0974: an increase in hepcidin to reduce serum iron levels. Imported from San Diego based Mabwell Therapeutics in January 2023, it has entered proof-of-mechanism Phase 1 study with an eventual eye on treating polycythemia vera, a chronic leukemia in which the bone marrow produces too many red blood cells (as well as white blood cells and platelets), causing the blood to become too viscous, impairing blood flow, and manifesting in pulmonary issues such as blood clots. Initial healthy subject data is expected in 2024. DISC-3405 received a Fast Track designation from the FDA in September 2023.

Collaborations

Each of these in-licensing deals came with different price tags.

For bitopertin, Disc paid Roche $4.5 million upfront and is potentially obligated on aggregate milestones of $205 million for the EPP and XLP indications, as well as high-single digit to high teens royalties. Additionally, concurrent to Disc going public, it issued 482,313 shares of IRON to Roche.

For DISC-0974 (and preclinical asset DISC-0998) AbbVie received $0.6 million upfront and is eligible to receive milestones up to $150.5 million in the aggregate, as well as low-single digit royalties.

For DISC-3405, Mabwell was paid $10 million upfront and is eligible to receive aggregate milestones of $402.5 million covering three indications, as well as single digit royalties.

Balance Sheet & Analyst Commentary:

To cover these in-licensing costs and the advancement of its programs through the clinic, Disc opportunistically executed a secondary subsequent to announcing initial promising data regarding bitopertin in June 2023, raising net proceeds of $147.9 million at $49 per share in a sale of common stock and pre-funded warrants. As of September 30, 2023, the company held cash and equivalents of $370.5 million, providing it an operating runway well into 2026.

With initial strong data from bitopertin, the Street was unanimously behind Disc until Morgan Stanley’ Jeffrey Hung downgraded shares of IRON from an outperform to a hold after a strong run, leaving him the only one of nine analysts without a buy or outperform rating. Their price targets range from $70 to $85 a share on IRON.

It should also be noted that OrbiMed Advisors, represented on the board by Mona Ashiya, has reduced its position in Disc, selling 553,300 shares on December 12-14, 2023, reducing its position to 1.7 million shares, or 7% ownership interest. They also have sold just over $12 million worth of shares in January of this year.

Verdict:

To date, Disc has done a solid job of in-licensing other drug concerns’ castoffs and converting them into viable clinical candidates for hematological disorders. In fact, Morgan Stanley estimates the company’s aggregate peak domestic sales from bitopertin and DISC-0974 at more than ~$700 million.

However, given the relative lack of placebo-controlled data to date and earliest commercialization for bitopertin not likely occurring until late-2026 or early-2027 under a best-case scenario, Disc Medicine, Inc.’s $1.2 billion market cap net of cash is fair. Upcoming data from AURORA will set the early tone for the company in 2024, but even if it validates BEACON, the amount of upside in IRON shares is somewhat capped (for now). Without any change in news, Disc merits at least a “watch item” position below $50 and this is a story will keep an eye on in 2024.

A man who is good enough to shed his blood for the country is good enough to be given a square deal afterwards.” – Theodore Roosevelt.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here