Aerospace and defense companies are performing strongly, some perform strongly due to the positive trends in commercial airplane productions and utilization and others are performing very well due to the increased demand for defense equipment and services. In my view, European aerospace companies have significant upside, as they have been underappreciated in comparison to their US peers. One of those names that I believed has significant space to run up is BAE Systems (OTCPK:BAESF, OTCPK:BAESY), and the buy rating on BAE Systems has performed extremely well with a 74% return on its share prices compared to the 28% return for the S&P 500. In this report, I will be revisiting BAE Systems and discuss whether I see additional upside for the stock and discuss the latest earnings and outlook.

BAE Systems Sales Grow, Expected Margin Expansion Remains Absent

BAE Systems

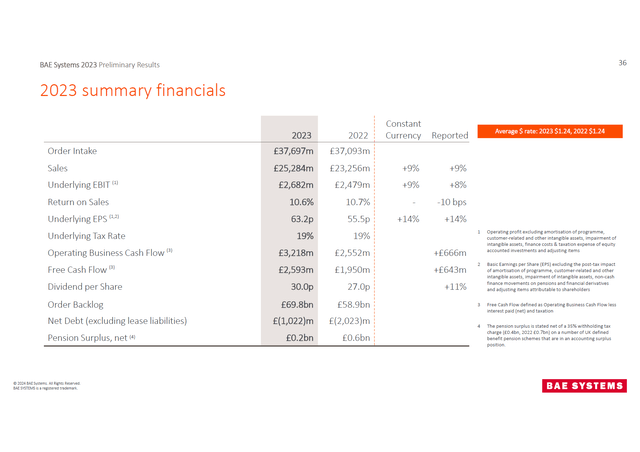

BAE Systems provides detailed earnings every six months, so in this report I will be discussing the 2023 earnings. Starting with order intake, we see it grew 1.6% to £37.7 billion. While that is not a huge backlog growth, we see that the book-to-bill ratio for 2023 was almost 1.5x, pointing at a strong opportunity for sales growth supported by the backlog growth and backlog of nearly £70 billion. Year-over-year sales grew 9% to £25.3 billion, with margins more or less stable. In December 2022, I pointed at the combination of sales growth with higher margins as a driver of the company’s valuation and appeal. We see that the sales growth is indeed there, but the margin expansion is not there yet.

However, we do see solid free cash flow growth of £643 million to £2.6 billion and that increase was in line with the operating cash flow. So, while margins have been stable, we see that cash flow growth is outpacing both the earnings and sales growth.

Electronic Systems sales grew in line with the revenue growth driven by commercial aerospace strength and growth in electronic combat systems, but its margins declined to 16.1% from 16.6% resulting in nearly £1.1 billion in EBIT. Platform and Services sales grew 7%, falling short of the company sales growth, but the segment margins increased from 8.8% to 9%. Sales were driven by combat vehicles volumes and ship repair volumes, while margins increased, driven by Combat Mission Systems and higher margins in a Swedish subsidiary.

Air sales grew by 4.7% to £8.1 billion, driven by higher volumes on the BAE Systems Tempest, which is the in-development sixth generation fighter to replace the Eurofighter Typhoon. Furthermore, Typhoon support activity increased and higher missiles demand. Margins grew from 11% to 11.8% reflecting lower program risks. Maritime sales grew 20% to £5.5 billion, driven by funding acceleration for the Dreadnought program and higher combat ship activity. Margins remained stable at 7.7% resulting in EBIT of £425 million. Cyber & Intelligence sales grew 5% to £2.9 billion, but margins fell from 10.5% to 8.6% resulting in EBIT decline from £287 million to £248 million. The decrease in margins primarily reflects investments in space and networking capabilities.

So, when viewing all segments in the context of combining revenue growth with margin expansion, we can conclude that Air, Electronic Systems and Platforms & Services were able to achieve this. It is not a bad thing, I would say, but it shows that margin expansion remains challenging as expansion in some segments and domains is offset by stable or lower performance in others. However, what does stand out is the strong cash conversion in all segments.

Is Ball Aerospace now BAE Systems?

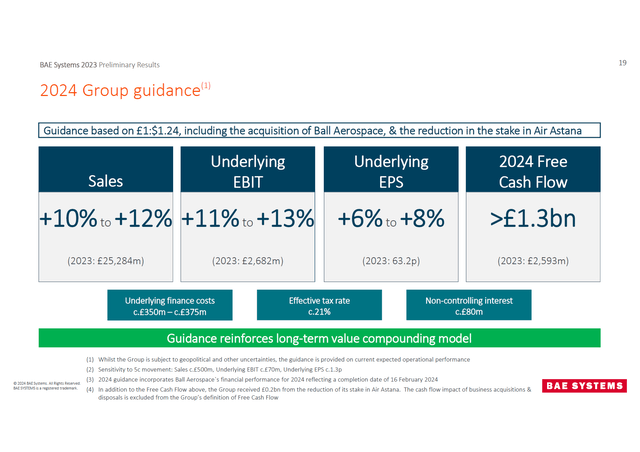

In August 2023, BAE Systems agreed to buy the Aerospace segment from Ball for $5.6 billion. The transaction has been completed in mid-February 2024 and Ball Aerospace is now part of the newly established Mission & Space system business which is part of the Electronics Systems segment and will add $100 million in free cash flow.

BAE Systems

For 2024, BAE Systems expects 10 to 12 percent growth in revenues and 11 to 13 percent growth in EBIT. About half of the sales and EBIT growth comes from Ball Aerospace. Electronic System Sales are expected to be up about a third driven by the acquisition and integration of Ball Aerospace with margins of 15% down from 16.1% last year and that margin decline is also by Ball Aerospace which has lower margins compared to the segment. Platforms and Services sales will be up 5 to 7 percent with margins of 10 to 11 percent, up from 9 percent a year ago. Air sales are expected to be up 3 to 5 percent on stable margins and Maritime Sales are expected to be up 6 to 8 percent with margins of around 8%. Cyber & Intelligence sales growth is expected to be 3 to 5 percent with margins in the 8 to 9 percent range compared to 8.6 percent a year ago. So, overall, the story is mostly about sales growth coupled with inorganic growth and not so much about segment margin expansion as I had expected. There is also a 100 bps sales and EBIT headwind from the disposal of the stake in Air Astana. The free cash flow guide for 2024 is >£1.3 billion and in my view that is a conservative guide and I would be expecting around £3.2 billion in free cash flow given the conservative 3-year guidance that BAE Systems provides against actual cash flow performance as well and the growth rate observed.

The Aerospace Forum

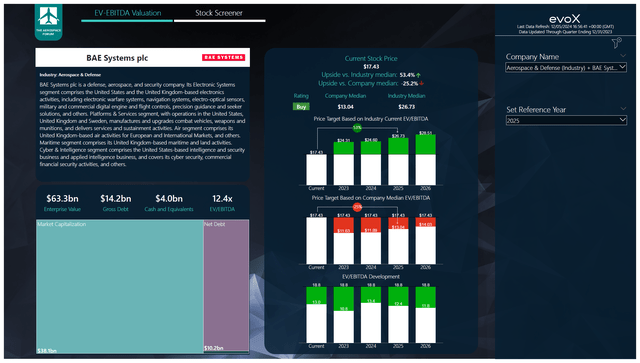

Valuing BAE Systems stock is tricky. The median EV/EBITDA of 9x does not provide upside to the stock. However, the industry median provides significant upside, namely 53%. I believe that given the current tailwinds in commercial aerospace as well as defense, it is justified for BAE Systems to trade at expanded multiples. Taking an EV/EBITDA of roughly 14x which is right in between the median for the peer group and BAE Systems, we get to a price target of $19.88 providing 14% upside based on 2025 earnings.

Conclusion: BAE Systems Stock Remains A Buy

BAE Systems had quite a big run-up in its stock price, but I believe there is more upside. It is unlikely to be in the return range we have seen previously unless the market considers that BAE Systems is worth an aerospace peer group valuation. However, I believe that the upside is compelling, with sales growth currently and the associated shift in company margin mix providing margin upside. It will be interesting to see whether we can see some thorough margin expansion on segment level as well, which would drive even more upside. We certainly see positive trends in end markets, and BAE Systems is increasing exposure via investment and acquisitions to capitalize on the market trends.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here