By Gene Tannuzzo, CFA, Global Head of Fixed Income

You don’t have to be bearish on the economy to be optimistic on the bond market. Here’s why.

As we head into 2024, we think that the next phase for the Federal Reserve is likely a pause while the central bank assesses the impact of the tighter lending and financial conditions it’s established. Investors should expect a lot of talk about whether the Fed will achieve a soft landing, but bond investors have the potential to generate attractive returns either way. Here’s our rationale:

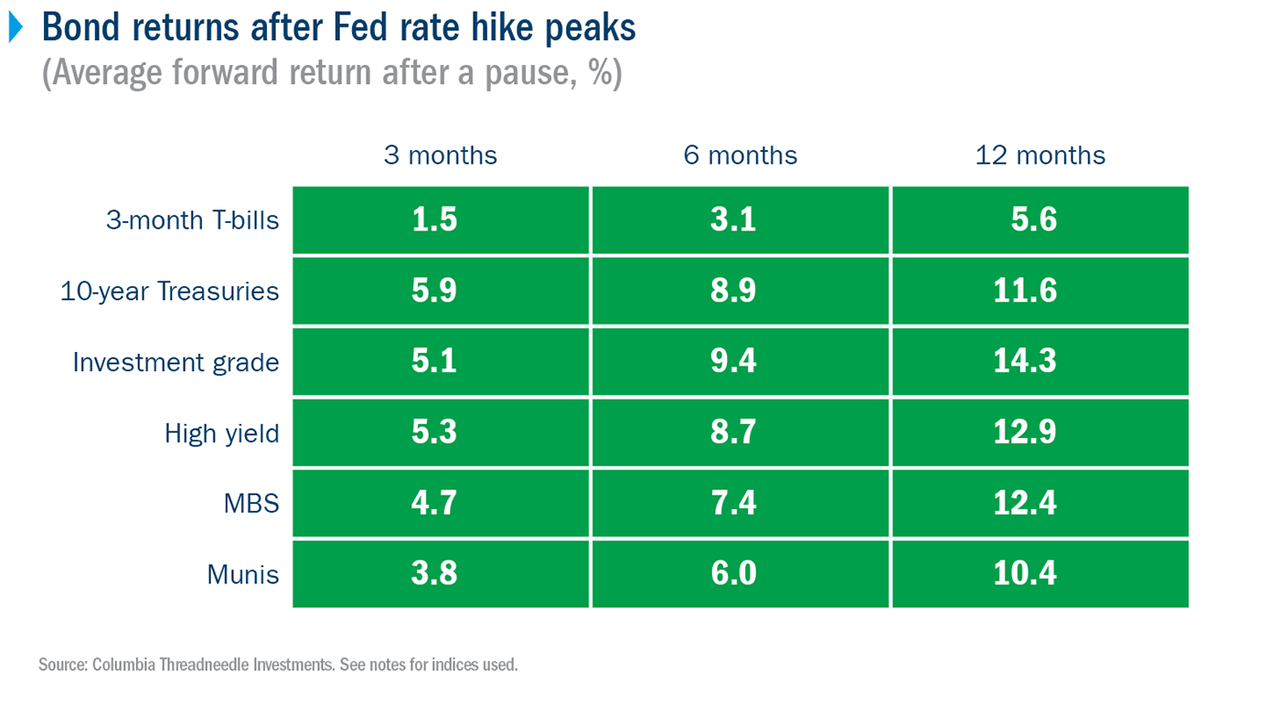

Bonds have performed well around Fed pauses

Typically, Fed pauses like this last less than a year, and it doesn’t take a cut in rates for bonds to rally. History suggests that when the Fed reaches the peak of its rate hike cycle, overall bond performance in the period afterward is exceptional.

We’re not in the hard landing camp, but given the unknown magnitude of an economic slowdown and the level of inflation, we think where investors are on the quality spectrum will make a difference. While lower rated bonds have been strong performers in 2023, we think the market is going to be more discerning as we head into 2024. We expect higher quality bonds will be the best bond performers over the next year.

We also think performance will be more dispersed than it has been. As we enter a higher-for-longer rate environment, we should see more separation between the winners and the losers – especially in lower quality segments of the market. This will make credit selection more important, which is one of our core strengths.

Investors can lock in higher rates for the long term

Bond yields have risen to levels we haven’t seen in decades. We think investors shouldn’t miss the opportunity to lock in higher yields for the long term (not to mention the total return potential as prices on those bonds rise). It’s also a great incentive to move out of cash. There’s been a money market renaissance as investors realized they can own cash and get a competitive yield. The attractiveness of cash will start to fade when short-term interest rates move lower and the diversification benefits of owning high-quality, long-term bonds at higher yields start to make more sense.

Opportunities in municipal bonds are even more attractive when you consider the effect of taxes, especially in high tax states, where tax equivalent yields on high-quality munis create a further incentive. Underlying municipality fundamentals are generally healthy, but we’re cautious on high-yield munis, which are not offering yields that much higher than better quality bonds for the added risk.

Looking outside U.S. markets, opportunities may be even more striking in Europe, despite lower absolute yields. Unlike the U.S., they’re coming off not just near-zero interest rates, but negative rates. Now, we’re not only seeing positive real interest rates, but also wider credit spreads. That means you’re going to get more risk premium for a similarly rated bond in Europe than you would in the U.S.

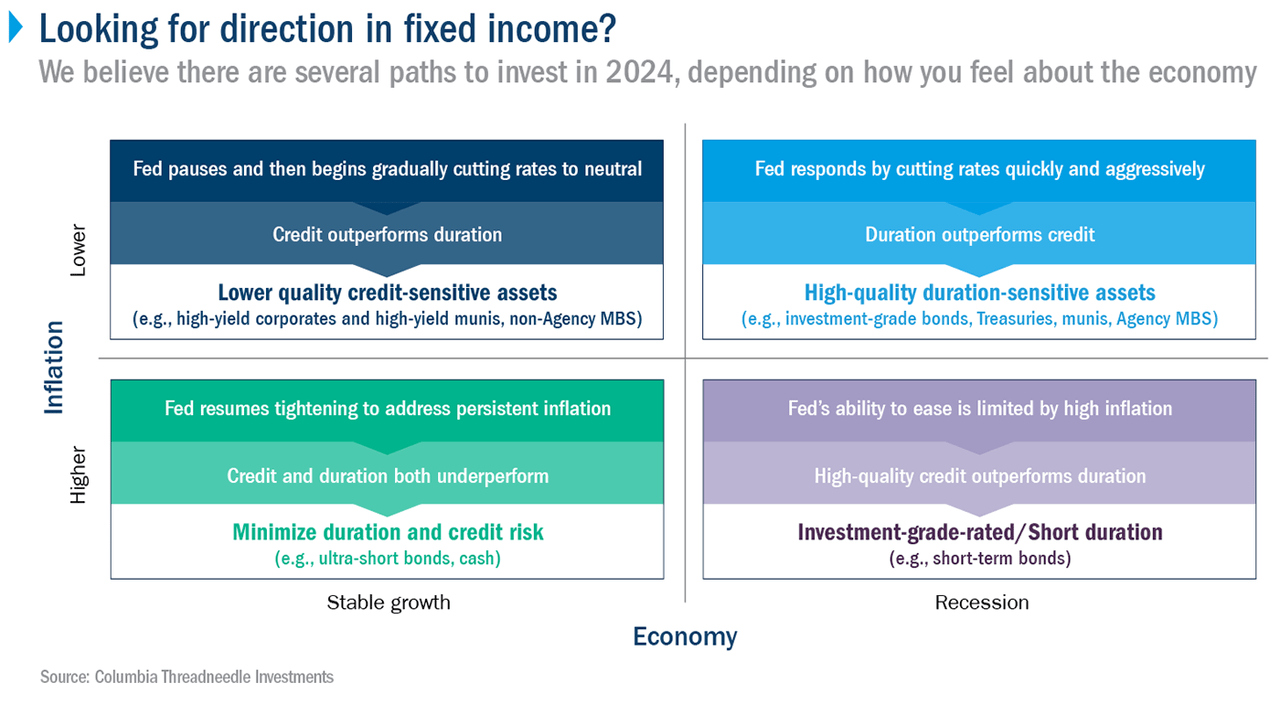

There’s more than one way to take advantage

There are several paths to invest in the bond market in 2024, depending on how you feel about the economy:

-

Get paid with higher yielding credit. If you feel growth will remain resilient, you could benefit from the income of high yield (if you are comfortable with the risk) and ultra-short bonds.

- Seek income and mitigate risk with high-quality bonds. If you’re not confident about the economy, high-quality assets like municipals and short-term bonds could help mitigate risk in case of a harder landing.

The bottom line

Our optimism for bonds is balanced by a realistic view of a still uncertain economy, and the understanding that geopolitical risk has the potential to introduce volatility. Having said that, we still think a hard landing is unlikely. More importantly, we believe the peak in rates is near and a Fed pause will be a significant market event. It’s an inflection point that has historically delivered outsized returns for bondholders. Combined with the opportunity to lock in attractive yields, we think now is an opportune time for investors to participate in the bond market.

© 2016-2023 Columbia Management Investment Advisers, LLC. All rights reserved.

Use of products, materials and services available through Columbia Threadneedle Investments may be subject to approval by your home office.

With respect to mutual funds, ETFs and Tri-Continental Corporation, investors should consider the investment objectives, risks, charges and expenses of a fund carefully before investing. To learn more about this and other important information about each fund, download a free prospectus. The prospectus should be read carefully before investing. Investors should consider the investment objectives, risks, charges, and expenses of Columbia Seligman Premium Technology Growth Fund carefully before investing. To obtain the Fund’s most recent periodic reports and other regulatory filings, contact your financial advisor or download reports here. These reports and other filings can also be found on the Securities and Exchange Commission’s EDGAR Database. You should read these reports and other filings carefully before investing.

The views expressed are as of the date given, may change as market or other conditions change and may differ from views expressed by other Columbia Management Investment Advisers, LLC (OTC:CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, may not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not take into consideration individual investor circumstances. Investment decisions should always be made based on an investor’s specific financial needs, objectives, goals, time horizon and risk tolerance. Asset classes described may not be appropriate for all investors. Past performance does not guarantee future results, and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that any forecasts are accurate.

Columbia Funds and Columbia Acorn Funds are distributed by Columbia Management Investment Distributors, Inc., member FINRA. Columbia Funds are managed by Columbia Management Investment Advisers, LLC and Columbia Acorn Funds are managed by Columbia Wanger Asset Management, LLC, a subsidiary of Columbia Management Investment Advisers, LLC. ETFs are distributed by ALPS Distributors, Inc., member FINRA, an unaffiliated entity.

Columbia Threadneedle Investments (Columbia Threadneedle) is the global brand name of the Columbia and Threadneedle group of companies.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here