Co-produced by Austin Rogers

Many investors like the idea of contrarianism, or going against the crowd. And we all know that in order to be a successful investor, we must at least sometimes, in some ways, embrace contrarian ways of thinking.

But often, when the market is gripped with fear or greed, investors find actual contrarianism unappealing. We go along with the broad thrust of the market, only realizing later on that we failed at our chance to embrace contrarianism.

It is only human. When stock prices are dropping, rather than see it as great buying opportunity (accumulating shares on the cheap when others are despondently selling), many of us become paralyzed by fear, thinking that the market must know something we don’t.

Even when we have done our due diligence and can’t see why our stocks are bleeding red, it is hard not to go along with the crowd and sell, just to free ourselves from the discomfort of paper losses.

Contrarianism is hard, almost by definition.

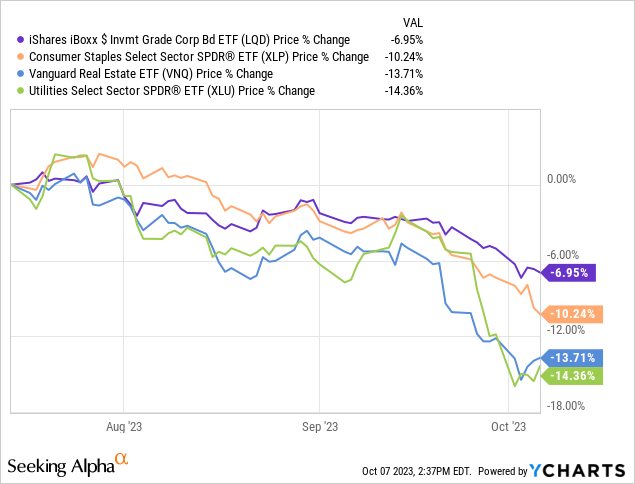

Right now, perhaps the most consensus view in the market is “higher for longer” interest rates.

That is why bonds and debt-utilizing, dividend-paying stock sectors have sold off so heavily over the last few months. See, for example:

- iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD)

- Consumer Staples Select Sector SPDR ETF (XLP)

- Vanguard Real Estate ETF (VNQ)

- Utilities Select Sector SPDR ETF (XLU)

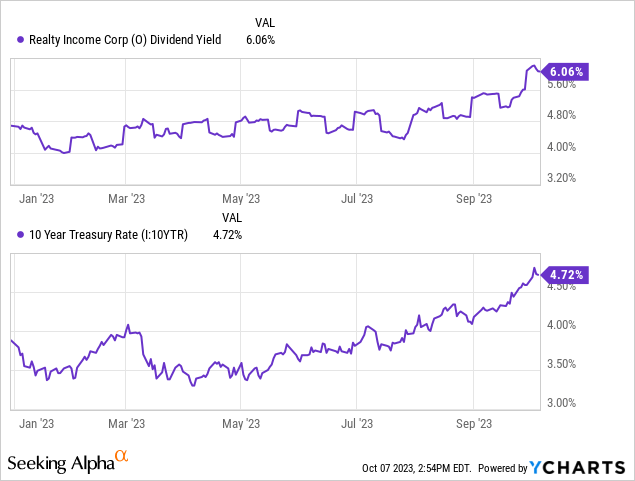

Bond yields have surged, causing companies’ cost of debt to rise and creating competition for income investors’ money. As bond yields rise, income-seeking investors increasingly turn to lower-risk bonds, forcing dividend stocks like REITs to reprice at higher dividend yields in order to remain competitive.

Take, for example, monthly dividend-paying real estate stalwart, Realty Income (O). As the 10-year Treasury yield has surged higher this year, so too has O’s dividend yield.

Virtually the same could be said about corporate bonds, REITs, utilities, and consumer staples.

So, if one of the most consensus views in the market right now is “higher for longer,” perhaps the most contrarian view would be to buy the very stocks that have taken the biggest hit from the “higher for longer” narrative.

As you can see from the chart above, one of the most badly beaten up sectors has been real estate, or REITs. Therefore, we think dyed-in-the-wool contrarians should be looking for buying opportunities in the REIT space right now.

This isn’t “blind contrarianism.” We genuinely think the market has it wrong.

Contrary to what the market seems to be pricing in, we think the odds of a coming recession remain high, as we explained in “The 2023 Recession Is Still Likely.” And recessions have an excellent track record of quickly bringing down both inflation and interest rates.

With that said, here are two of our favorite REITs to benefit from a potential drop in interest rates.

Alexandria Real Estate Equities (ARE)

ARE owns state-of-the-art, Class A life science R&D properties located in the most productive and highly sought after innovation clusters in the United States.

Alexandria Real Estate

Unlike traditional office buildings, ARE’s facilities are not nearly as susceptible to remote work. The mission-criticality of the research and magnitude of intellectual property contained within these buildings makes them indispensable to the tenants.

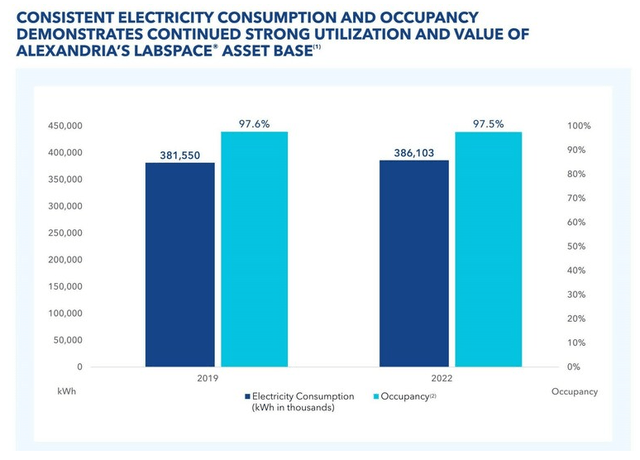

As a demonstration of this, ARE recently highlighted that its portfolio occupancy rate of 97.5% is basically the same as it was in 2019, while electricity consumption at its buildings has even increased.

ARE Q2 2023 Slides

This shows that its buildings’ usefulness as lab spaces and storage of experiments and tests has only increased.

Maybe researchers need to spend just as much time in the lab today as they did in 2019, or maybe they don’t. In either case, the bulky, expensive, specialized, highly power-intensive equipment housed in these lab spaces ensures that they will remain indispensable to their users (ARE’s tenants).

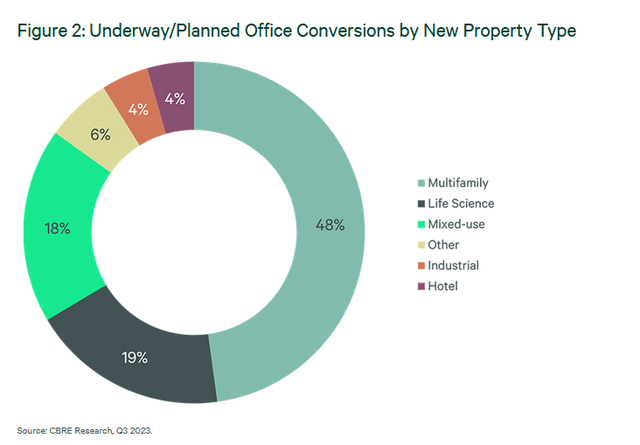

Another worry the market seems to have is the oncoming wave of new supply. Almost 1/3rd of office space under development is life science, and about 1/5th of traditional office conversions underway are expected to end up as life science properties.

CBRE

We think the market’s concerns here are misplaced. The market seems to treat life science real estate the same as traditional office, which is basically a commodity product wherein each office building has little to no competitive advantage.

On the contrary, we think ARE’s high-quality, energy-efficient building designs and unbeatable locations within the nation’s top innovation clusters together act as a “moat” against the increasing competition. Most of this oncoming supply will not enjoy nearly the same quality of construction or location as ARE’s properties.

There may be some downward pressure on leasing volume and rent growth from the increased supply, but not to the degree that the market seems to fear.

Finally, what makes ARE such a great REIT for falling interest rates? Three things:

- Depth of valuation discount: ARE currently trades at a price to AFFO of a little under 11x, compared to a 5-year average (not peak!) AFFO multiple of 25.5x. During the period of ultra-low interest rates, it traded at a multiple over 30x. Even if ARE only ever regains a valuation multiple of 20x, that still implies over 80% upside.

- Fortress balance sheet: ARE enjoys BBB+/Baa1 credit ratings that were just affirmed by Moody’s, low debt, >99% of debt featuring fixed interest rates, a weighted average debt maturity over 13 years, and no loans maturing until 2025. That means that if interest rates fall before 2025, ARE will have suffered very little impact from the period of rising rates.

- While most of ARE’s tenants are large biotech corporations, a meaningful minority of tenants are newer, smaller biotech startups with venture capital funding. High interest rates have depressed VC funding. Thus, falling interest rates will likely cause VC funding in the biotech space to make a resurgence.

While you wait for the upside from repricing, ARE pays a 5% dividend yield and it is expected to grow its cash flow by about 6% in 2023, resulting in double-digit economic returns.

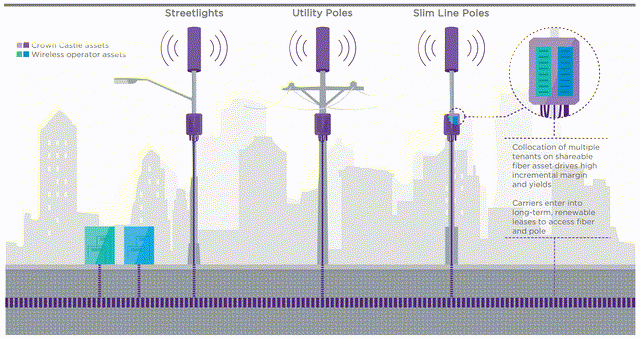

Crown Castle (CCI)

With its extensive network of telecommunications infrastructure across the United States, including 40,000+ cell towers, 120,000 small cell nodes, and 80,000 route miles of fiber, CCI boasts perhaps the largest portfolio of telecom infrastructure in the US.

Crown Castle

We love CCI’s business model because of its ability to colocate multiple tenants onto the same piece of infrastructure.

Take CCI’s largest growing segment of small cells. These assets typically start as build-to-suit projects for a single carrier-tenant at a cash yield of 6-7%, but as more tenants are added (colocated) over time, the cash yield on CCI’s invested capital rises into the double digits. And given contractual rent escalations of 2-3% per year, CCI’s revenue grows whether carriers are expanding their network footprints or not.

There are three primary reasons why CCI has lost over 50% of its market cap since the beginning of 2022:

- Sprint is canceling many of its tower leases with CCI as a result of its merger with T-Mobile (TMUS). The hit from these cancellations will be felt through 2025. However, CCI still expects to grow its revenue and cash flow at a low single-digit pace over the next two years, and management remains confident in its ability to return to mid- to high-single-digit growth thereafter.

- CCI began the current rising interest rate environment with around 20% of total debt with floating rates. Thus, despite its BBB+ credit rating, the market perceived CCI as being particularly vulnerable to rising rates. After issuing some fixed-rate debt at about a 5% interest rate earlier this year, though, CCI’s floating rate debt as a percentage of total debt sits at only 9%.

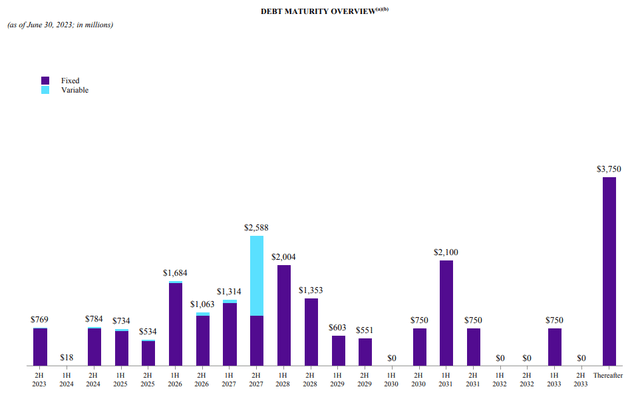

- CCI still has $750 million of debt maturing in the second half of 2023, as of the end of the second quarter. This debt bears an interest rate of 3.2% and will likely have to be refinanced at a new interest rate about 250-300 basis points higher. Moreover, CCI has a $500 million note bearing interest at 1.35% maturing in 2025 and a $1 billion note bearing interest at 1.05% maturing in 2026. Unless interest rates reverse course and go back to ultra-low levels, CCI will have to refinance these notes at meaningfully higher interest rates. Fortunately, these amounts are not very big for a company with a ~$40 billion dollar market:

CCI Q2 2023 Supplemental

The good news is that CCI has virtually no debt maturities in the first half of 2024, and maturities through the end of 2025 are manageable.

Don’t get us wrong, we believe CCI will be able to survive if interest rates stay at their current level, albeit with a slower growth rate.

But if interest rates fall sooner than the market is expecting, CCI should massively outperform.

Consider this: CCI currently trades at about a 12x AFFO multiple, compared to its 5-year average of 23x. At the lowest level of interest rates, CCI reached a peak valuation of 30x AFFO.

If CCI only ever regained a conservative 18x multiple, it would imply 50% stock price upside from here. If it regained its 5-year average multiple of 23x, it would achieve around 80% upside.

While you wait, you earn a 7% dividend yield, and the management has guided for a return to 7-8% annual FFO per share post-2025, which should result in ~15% average annual economic returns.

Bottom Line

These two REITs are high-quality companies with strong balance sheets, investment-grade credit ratings, and attractive real estate assets that enjoy durable demand. Investors today can buy ARE at a slightly over 5% yield and CCI at a 7% yield. That provides shareholders a significant stream of dividend income so that they can get “paid to wait” for the potential upside described above.

If interest rates plateau and remain at this level for many years, we still think these two REITs will survive and are confident in the margin of safety at which we can buy them today.

But if interest rates drop over the next year or so, as we expect, then these two blue chip REITs should soar. Ultimately, we believe we will be happy to have stuck with our “landlord” mindset in buying and holding these real estate assets for the long run.

We are embracing contrarianism by buying REITs like these two today.

Read the full article here