U.S. oil production has been holding at or near record highs since October, topping the previous peak from 2020, even though the number of active domestic oil drilling rigs is down by nearly 30% from four years ago.

Strength in oil prices and gains in investment and output efficiency have contributed to that climb, though analysts see a potential slowdown in output growth ahead.

U.S. oil production has “nearly tripled in the last 15 years, fueled by advances in drilling and fracking technology and investments in the early 2010s due to sustained higher oil prices and favorable government policies,” said David Carter, industrials senior analyst with assurance, tax and consulting firm RSM US.

U.S. strategy to “reduce dependence on foreign oil led to various federal and state-level tax breaks and eased regulations for oil exploration and production (E&P) companies.”

The surge in production has also led the U.S. to become a “major oil exporter, opening up new markets for companies to sell the increased production despite limited increases in U.S. demand,” he told MarketWatch.

Read: What record crude production says about the long road to U.S. oil independence

U.S. crude-oil production stood at 13.2 million barrels per day as of the week ended Jan. 5, after reaching a record at 13.3 million bpd for the weeks ended Dec. 15 and Dec. 22, according to data from the Energy Information Administration.

That topped the previous record of 13.1 million bpd for the week ended March 13, 2020.

At that time, the number of active U.S. rigs drilling for oil stood at 683, according to data from Baker Hughes

BKR,

That number was at 499 as of the week ended Jan. 12, marking a roughly 27% drop.

Drilling efficiencies and rig counts

Since 2010, one of the biggest developments in oil production efficiency was the “increase in horizontal drilling, called laterals, and fracking, said Carter.

Horizontal drilling is a drilling technique in which a well is drilled along a horizontal path, while fracking involves injecting liquid at high pressure to help extract oil or gas.

In the Permian Basin, average lateral lengths, defined as the horizontal sections of a well, grew by over 250% to over 10,000 feet from 2010 to 2022, while average oil production per rig grew from 126 bpd in 2010 to 1,211 bpd in 2022, Carter said.

In a report published in September 2022, the EIA cited data from Enverus showing first quarter Permian Basin new well oil production of more than 200 bpd in 2010 and more than 1,000 bpd in 2022.

The Permian region spans parts of western Texas and southeastern New Mexico, with the EIA estimating that the region produces more crude oil than any other U.S. region, accounting for more than 40% of total domestic crude-oil production.

Oil E&P companies are also using “artificial intelligence and machine learning for optimization of exploration,” Carter said. Adoption of these technologies is likely to continue to “expand and mature as more use cases are discovered and optimized themselves.”

In a way, oil E&Ps are “becoming technology companies,” said Carter.

Imre Kugler, director of upstream research at S&P Global Commodity Insights, meanwhile, said that in roughly the last year and a half, the U.S. has had a 10% increase in the rate of penetration — the amount of feet drilled per day.

That means a rig today drills 10% more than it did just 2 years ago, he said. That’s where a lot of “efficiency gains” have been made.

Baker Hughes reported a U.S. oil drilling rig count of 499, as of the week ended Jan. 12 — a far cry from the four-digit rig counts last seen in 2015. The weekly U.S. oil drilling rig count last topped 1,000 on Feb. 20, 2015, at 1,019.

For that week, the EIA pegged production at just 9.285 million bpd.

A slowdown

Since the end 2022, the U.S. drilling rig count has dropped sharply but domestic oil production has climbed by around 1 million barrels per day.

The rig count has slowly fallen as commodity prices have fallen, but there is a “time lag, measured in months, between when the rig count increases and oil production increases,” said Chris Duncan, director of investments at Brandes Investment Partners.

Most of the drilling efficiency gains were made in the first half of the past decade, with drilling productivity gains slowing in the last three years, he said.

As production fields mature, there is the potential that efficiency gains are offset by less prolific wells, Duncan said. “Spare capacity in the oil-field service industry has been largely absorbed, leading to the risk of cost inflation if productivity gains are insufficient.”

So the “risk of productivity gains being offset by worsening geology and oil-field service cost inflation may be one of the many reasons for increased industry consolidation over the past couple of years,” he said.

Oil prices

Strength in oil prices have been a key reason to the rise in production.

At $70 a barrel, U.S. benchmark West Texas Intermediate crude is an important price point, said S&P Global’s Kugler. As long as prices are roughly over $70 a barrel on an annual basis, oil producers can still grow and provide return to shareholders, he said.

His company expects to see an average WTI oil price of $78 this year.

Unconventional oil production, which includes oil extracted from shale, likely breaks even at $60 to $65 a barrel, so prices around $80 would leave “a lot of breathing room,” said Kugler. That’s a “testament” to the overall resources available in the U.S., he said. “There’s still a lot of high quality, high break-even oil” that remains in U.S. unconventional oil drilling.

For now, oil prices trade closer to $70. On Tuesday, WTI crude for February delivery

CLG24

CL.1,

settled at $72.40 a barrel on the New York Mercantile Exchange, down 28 cents, or 0.4%.

Output growth

Looking ahead, production growth is likely to continue, “all else equal,” said Duncan, but “at a slower pace” than what has been seen over the past two years.

“How demand evolves over the next year will largely dictate the commodity price, which will dictate production growth” or decline, he said, with E&P cash flows at $70 a barrel likely to support current activity levels.

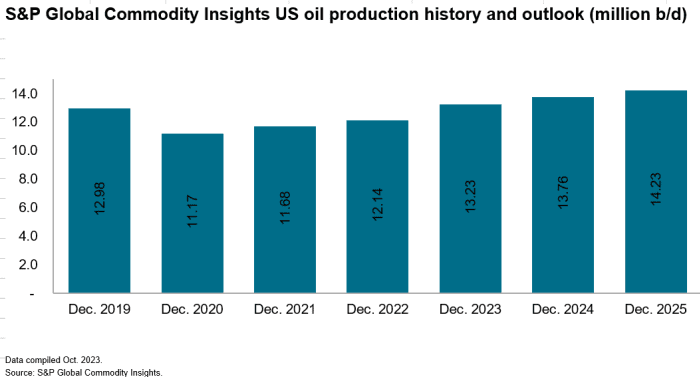

S&P Global Commodity Insights estimated U.S. oil production at 13.23 million bpd in December 2023, and sees growth in output to 13.76 million bpd in December 2024 and 14.23 million bpd in December 2025.

Overall, U.S. production growth will be a “function of the cost to develop new resources and whether the commodity price supports the cost of that development,” Duncan said. For now, “both seem to support slow production growth, but that could change with a major shift in any of the demand or supply macro factors.”

Read the full article here