The stock market, as measured by the S&P 500 Index

SPX,

bounced off the lower trend line of the bear market last week. The ensuing rally has been strong, fueled technically by oversold conditions and a favorable seasonal pattern.

But is this just another oversold rally, doomed to fail at or just above the declining 20-day Moving Average (as the one did in early October)? Or is it the “real thing,” something with more staying power? The answer will come from the price action of SPX.

Currently the S&P 500 is locked in a downtrend (lower highs and lower lows), marked by the declining red lines on the accompanying SPX chart. Until that changes, this is still a bearish market. The area around 4400 is important in that regard for a couple of reasons. First, a close above 4401.60 would close the gap on the chart from mid-September. Second, the downtrend line is in that same area, so a close above there would be a breakout above the downtrend line. Third, 4400 is the October high, so it is a resistance area.

On the other hand, if this is merely an oversold rally, expect it to top out just above the declining 20-day Moving Average of SPX, which is currently at about 4270.

This past week, several internal indicators generated buy signals, and we will review them here. First, a new McMillan Volatility Band (MVB) buy signal was generated (green “B” on the SPX chart). Its target is the upper +4σ Band, which is currently at about 4420 and moving sideways. The buy signal would be stopped out if SPX were to close below the -4σ Band – as happened with the two most recent MVB buy signals. That lower Band is currently at about 4120. This is a long-standing useful indicator, and it is rare to see two consecutive losing signals. But that’s what happened.

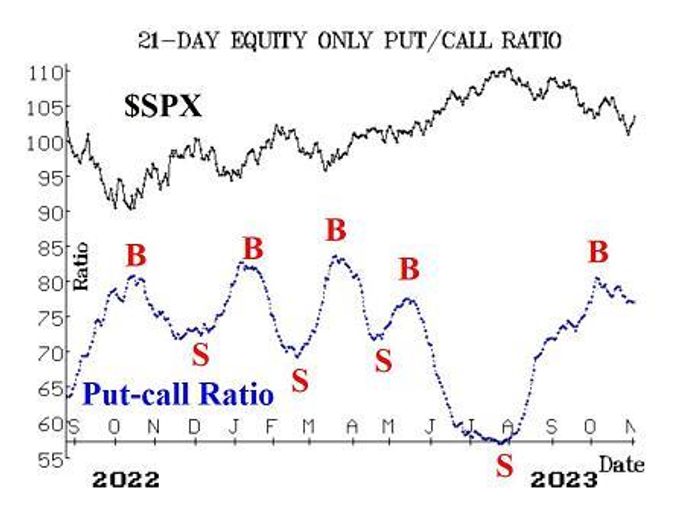

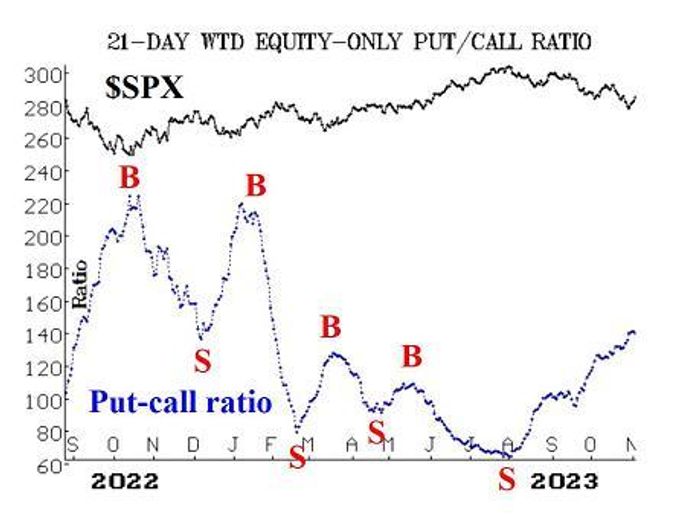

Put-call ratios are still giving mixed signals. The standard equity-only put-call ratio generated a buy signal a couple of weeks ago, and that was certainly premature at best and outright wrong at worst. The weighted equity-only put-call ratio has remained on a sell signal and is still on that sell signal today. Meanwhile, the total put-call ratio generated a buy signal. This is a short-term signal of sorts, as its target is a 100-point gain for SPX. That has already occurred, so that signal — while correct — is no longer in play.

Market breadth has finally improved, and the NYSE breadth oscillator has generated and confirmed a buy signal. However, the “stocks only” breadth oscillator is still not on a buy signal. It is quite close to one, though, and it could be confirmed today if breadth is positive.

New Lows on the NYSE continue to run at a high rate. Even when the market was rallying this week there were 100 to 200 stocks on the NYSE making new lows. Thus, this indicator remains negative. Its sell signal would only be stopped out if NYSE New Highs outnumber New Lows for two consecutive days.

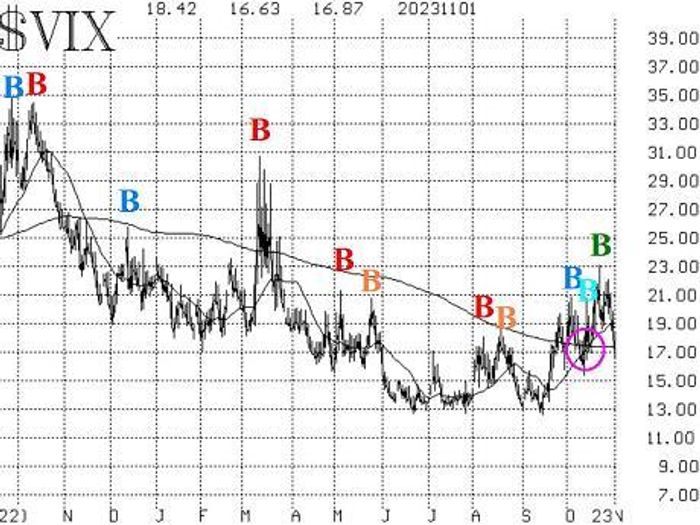

The indicators involving VIX

VIX

VX00,

are moving towards the bullish side in their outlook for stocks. First, the “spike peak” buy signal of October 24th remains in place. Second, the trend of $VIX sell signal, which was generated when both VIX and its 20-day moving average crossed above the 200-day moving average, is in jeopardy. That sell signal would be stopped out if VIX were to close back below the 200-day MA, and that appears to be happening. Yesterday (November 1st), VIX closed below the 200-day MA by a few cents, but we want to see something more definitive to stop out the sell signal. At the time of this writing, VIX is much lower than the 200-day (which is at about 17.35). Any close below 16.80 by VIX would stop out the sell signal.

The construct of volatility derivatives came perilously close to a sell signal, but never achieved that status. Now, it is improving to a much more bullish outlook for stocks. The term structure of the VIX futures is now sloping upwards again after the SPX rally and after the FOMC meeting. The 9-day CBOE Volatility Index (VIX9D) remains elevated above VIX, but that is mostly due to the fact that the Unemployment Report is due tomorrow.

“The October Seasonal pattern has been tremendously bullish again this year.”

The October Seasonal pattern has been tremendously bullish again this year. This seasonal pattern begins with the close of trading on October 27th and lasts through November 2nd. In that time, SPX has risen sharply again this year, and so this seasonal system will stand at 32 wins and 6 losses after today. We’ll use it again next year.

In summary, we are maintaining a “core” bearish position because of the downtrend on the SPX chart. In addition, we are trading other signals– many of which have been bullish — around that “core.”

New recommendation: Consumer Staples SPDR (XLP)

Again, this recommendation was not filled last week, but it remains open for the coming week, since XLP

XLP

is toying with the entry point. The original recommendation was based on a MVB buy signal, which has still not been confirmed. At this point, a close above 68.04 would also be a small technical upside breakout.

IF XLP closes above 68.04, THEN buy 4 XLP Dec (1st) 68 calls In line with the market.

XLP: 67.94

If bought, we will set a stop in the next newsletter.

New recommendation: MVB buy signal

Another MVB buy signal has been generated, as explained in the market commentary above. We are going to act on this signal.

Buy 1 SPY Dec (15th) at-the-money call and Sell 1 SPY Dec (15th) call with a striking price 15 points higher.

We will hold this position until either SPX reaches the +4σ Band or closes below the -4σ Band, whichever comes first. We will update the status each week in the follow-up section.

Follow-up action:

All stops are mental closing stops unless otherwise noted.

We are using a “standard” rolling procedure for our SPY spreads: in any vertical bull or bear spread, if the underlying hits the short strike, then roll the entire spread. That would be roll up in the case of a call bull spread, or roll down in the case of a bear put spread. Stay in the same expiration and keep the distance between the strikes the same unless otherwise instructed.

Long 1 SPY

SPY

Nov (10th) 412 put: Bought in line with the equity-only put-call ratio sell signals. We are going to hold a put until the weighted ratio rolls over to a buy. Most recently, we rolled down when the 420 puts became eight points in-the-money. Continue to roll down every time the put becomes 8 points ITM. In essence, this is our “core” bearish position.

Long 2 EQR

EQR,

Nov (17th) 60 puts: Roll down to the Nov (17th) 52.5 puts. We will continue to hold as long as the weighted put-call ratio for EQR remains on a sell signal.

Long 1 SPY Nov (20th) 412 put: Established in line with the “New Highs vs. New Lows” sell signal. Stop out if New Highs outnumber New Lows on the NYSE for two consecutive days. Most recently, we rolled to the 412 put when the 420 put became eight points in-the-money (ITM). Continue to roll down every this put becomes eight points ITM.

Long 0 CHEF

CHEF,

Nov (17th) 20 puts: Stopped out on November 1st, when CHEF closed above 20.20.

Long 2 DLR

DLR,

Nov (10th) 118 puts: Sell these puts now, since the weighted put-call ratio is no longer on a sell signal.

Long 3 XLE

XLE

Nov (17th) 86 puts: Hold as long as the weighted put-call ratio of XLE remains on a sell signal.

Long 1 SPY Nov (17th) 434 call short 1 SPY Nov (17th) 452 call: This spread was bought in line with the CBOE Equity-only put-call ratio buy signal. We are holding without a stop initially. Roll the whole spread up if the long side becomes at least 8 points in-the-money.

Long 3 ES

ES,

Nov (17th) 60 calls: Hold this position as long as the weighted put-call ratio chart for ES remains on a buy signal.

Long 1 SPY Nov (10th) 418 call: We originally bought two calls in line with the October seasonal trade. Then, when SPY rallied, we sold them and rolled to one 418 call. Sell this call at the close of trading on Thursday, November 2nd.

All stops are mental closing stops unless otherwise noted.

Send questions to: [email protected].

Lawrence G. McMillan is president of McMillan Analysis, a registered investment and commodity trading advisor. McMillan may hold positions in securities recommended in this report, both personally and in client accounts. He is an experienced trader and money manager and is the author of the best-selling book, Options as a Strategic Investment. www.optionstrategist.com

©McMillan Analysis Corporation is registered with the SEC as an investment advisor and with the CFTC as a commodity trading advisor. The information in this newsletter has been carefully compiled from sources believed to be reliable, but accuracy and completeness are not guaranteed. The officers or directors of McMillan Analysis Corporation, or accounts managed by such persons may have positions in the securities recommended in the advisory.

Read the full article here