In my original write-up on Etsy (NASDAQ:ETSY), I wrote that while the company had some growth opportunities ahead of it, that economic softness and vendors selling unlicensed merchandise posed a risk. As such, I was neutral on the name, but saw more risk to the downside. Since then the stock is down -40% versus an over 4% gain in the S&P. Let’s catch up on the name.

Company Profile

As a reminder, ETSY operates two-sided marketplaces that connect buyers and sellers. Its best-know marketplace is Etsy.com, which had $12 billion in GMS (gross merchandise sales) in 2022. The market place primarily focuses on the sales of crafts, handmade goods, and vintage items. The company also runs musical instrument marketplace Reverb, fashion resale marketplace Depop; and Brazilian-based marketplace for handmade items Elo7.

About three quarters of ETSY’s revenue is marketplace revenue, which consists of listing fees, transaction fees, and payment processing fees. The other quarter of its revenue comes from Services Revenues, which is made up of shipping labels, on-site advertising, and other services.

Number of Active Buyers Grow, But Are Buying Less

One of the opportunities for ETSY I discussed in my original write-up was for the company to attract more buyers and bring back lapsed buyers to the Etsy Marketplace. On that front, the company did well once again in Q2.

Active Etsy Marketplace buyers increased 3% to 90.6 million, which was up from the 1% growth it saw in Q1. The company had been focusing on bringing in more male buyers, and the number of male buyers did increase 8% year over year, up from the 6% growth it saw in Q1.

Another focus was on bringing back lapsed buyers. For Q2, the company reactivated 6 million lapsed buyers, a 21% year over year increase. This was a similar result to Q1.

Q1 was the first time the company increased its number of active buyers since Q4 2021, so to increase them in back to back quarters is a sign of solid progress on this front. However, once again the company did see some weakness on the buyer side as well. Habitual buyers decreased -9% year over year to about 7.0 million, continuing a trend it saw in Q1. Meanwhile GMS per active buyer on a 12-month trailing basis decreased -6% to $128.

Overall GMS was down -0.6%, or -0.4% ex-FX, to $3.0 billion, and Etsy GMS was down -0.7%, or -0.4% ex-FX, to $2.6 billion.

Revenue rose 7.5% to $628.9 million, helped by an earlier price increase and a shift towards more international buyers, which has more payment fees. Adjusted EBITDA rose 2% to $166.2 million.

Looking ahead, the company forecast Q3 GMS of between $2.95-$3.1 billion and revenue of between $610-645 million. It expects an adjusted EBITDA margin of between 27-28%, implying adjusted EBITDA of between $164.7-$180.6 million. At the time, analysts were projecting Q3 GMS of $3.07 billion and revenue of $633 million.

Discussing the current environment last month at the Goldman Sachs Communications & Technology Conference, CFO Rachel Glaser said:

“I mean there’s very clear data that suggests we’ve had heavy macro headwind and particularly affecting buyers with lower household income. We talked about that on our last call. The data clearly shows that there’s growth in buyers with higher household incomes in GMS and there’s decline in buyers with lower household income is really quite telling. We see lots of external data that says people are spending, but they’re spending on — heavily on essentials, health care, grocery, gasoline. So Etsy is none of those things. Certainly, you can buy diapers on Etsy if you want to, but for the most part, you’re going to another e-commerce player to buy those things. When we look at data we see, there’s growth in e-commerce, but if you strip out the really large sites that have blended in grocery or heavy orientation towards essentials and you look just more at pure-play e-commerce sites, Etsy is holding its own, sometimes winning, sometimes just shy, but we’re — the metrics are stable and solid. We talked about a lot of positives on our last call in spite of the macro environment that we’re in. So for instance, we had our highest ever active buyer count at the end of Q2. … I think we were just about flat on GMS per buyer. So things are trending in the right direction in spite of heavy macro headwinds. Macro headwinds are cyclical. So that means cyclical is cyclical. It means it’s temporal. It’s a thing that will pass. The underlying strength and the fundamentals of Etsy’s business continue to be very strong.”

Overall, it appears investors have been much more focused on how the macro is impacting ETSY compared to the turnaround in active buyer growth the company has seen. The company obviously can’t control the macro, and the home furnishing and decorating area is one that has been hit particularly hard. However, I really like the strides the company is making, and it will be interesting if some of the AI investments it is making can help make its marketplace a better shopping experience that makes it easier to sort and search its items. That could be a nice longer-term growth driver.

Q3 Earnings Preview

ETSY has beaten results on both the top and bottom lines consistently over the past two years, so I wouldn’t expect any surprises on that front. However, guidance has often driven the stock, and investors haven’t liked the company’s more cautious tone the past two quarters, despite the turnaround in growing active buyers. The stock sold off -6.7% the next session after in its Q1 report and -15.9% after its Q2 report.

As such, revenue guidance likely will be the main focus for investors. On that front, analysts are currently projecting Q4 revenue of $843.9 million, which would represent about 4.5% year over year growth. Notably, last quarter the company lapped an earlier Etsy Marketplace transaction fee change, and it also noted that Q4 take rate is usually seasonally lower.

I’d expect ETSY to continue to take a more cautious stance, but the Q4 revenue estimates seem fairly reasonable and its stock price is down a lot.

Valuation

ETSY stock currently trades around 12.5x the 2023 consensus EBITDA of $746.4 million and about 11.2x the FY2024 consensus of $828.5 million.

It trades at a forward PE of nearly 14x the 2023 consensus of $4.64 and just over 13.2x the 2024 consensus of $4.91.

Revenue growth is expected to be 7.3% this year, and then grow around 9-13% a year over the next few years.

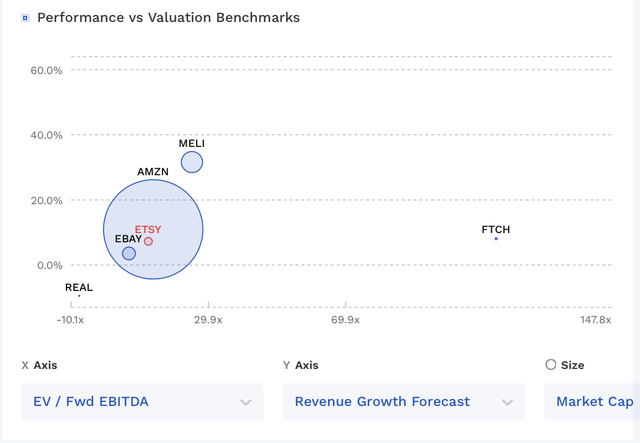

ETSY trades at towards the middle of the pack vs other marketplace stocks, trading at a premium to the likes of eBay (EBAY) and at a discount to Amazon (AMZN).

ETSY Vs Peer Valuations (FinBox)

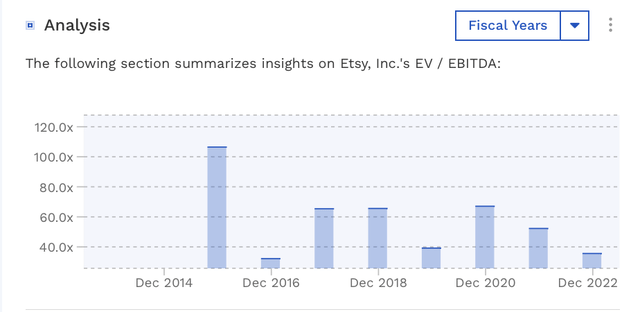

Historically, it’s trading historically at one of its lowest EV/EBITDA multiples by far, and it’s also trading at a big P/S discount to where it historically traded as well, under 3x versus an average of 10.6x from 2018-2022.

With investors overly focused on the macro, I think ETSY’s sell-off has taken the stock to one of its most attractive levels in a long time.

ETSY Historical EV/EBITDA Valuation (FinBox)

Conclusion

While ETSY has some challenges, I like how the company has been able to increase its active users, and its push into international markets also appears to be gaining traction. The current valuation is also much more attractive now than in the past. As such, I’m going to raise my rating to “Buy” with a $100 price target. That’s about a 4.5x EV/sales multiple and under 15x EV/EBITDA multiple, which seem reasonable give its revenue growth rates.

The biggest risk to the name is the macro impacting spending on its marketplaces even more than anticipated, as well as any crack downs on merchants selling unlicensed merchandise.

Read the full article here