Per LSEG, only 29 companies have reported their Q1 ’24 earnings so far, and the big banks that reported on Friday morning April 12th, won’t be in the numbers so to speak until Monday, April 15th or Tuesday, April 16th. Another 41 companies are expected to report this week.

The point being to all this is that the “expected” Q1 ’24 S&P 500 EPS growth has fallen to +2.7% as of Friday, April 12th, ’24, (down from +5% as of last Friday, April 5th), which might alarm some, but that pattern is pretty typical.

Q4 ’23 S&P 500 EPS expected YoY growth peaked at +10.9% on 9/22/23, then fell to an expected growth rate of +4.4% as of January 12, ’24 while actual S&P 500 EPS growth wound up at +10.1% or twice the expected growth rate by late March ’24.

The “expected” quarterly growth rates follow a typical pattern, like the above. Ed Yardeni has long called this the “fish-hook effect”. Quarterly growth rates start higher 3-6 months out, as the actual quarter gets set to be reported (as Q1 ’24 is getting started now) the quarterly S&P 500 growth rate bottoms (usually prior to the busiest weeks) and then stabilizes or moves 3-5% higher typically for that quarter’s expected growth.

In other words, Q1 ’24’s final S&P 500 EPS growth will likely be between 5-7% ultimately. However, the “upside surprise” factor matters, which this blog has written about here.

Here’s what might be interesting:

As Q1 ’24 earnings get reported, watch how full-year ’24 expected sector EPS growth rates change.

In the above table, note the sharp drop in the “expected” healthcare sector’s earnings (highlighted). That could be a bad estimate, or it could be the first sign of a tougher year for healthcare.

Healthcare had a tougher year in ’23, returning just 2% despite the weight-loss drug impact. Johnson & Johnson (JNJ), Abbott Labs (ABT) and Intuitive Surgical (ISRG) are healthcare companies reporting this week.

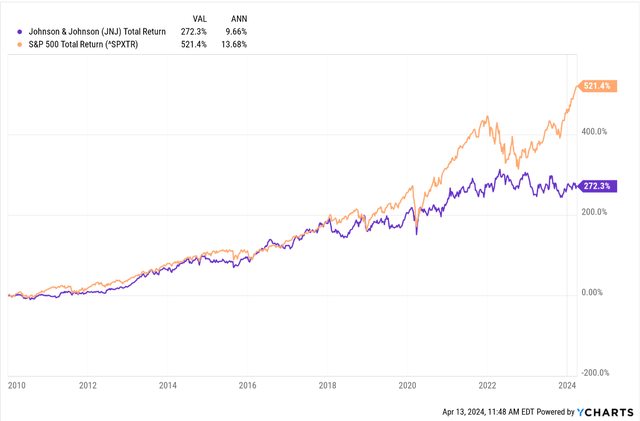

Speaking of Johnson & Johnson, this blog’s technician, Gary Morrow (on X @GarySMorrow) let me know this week that JNJ would soon test its ’23 low near $144.

This performance chart shows how JNJ has underperformed the S&P 500 for the last 13 years, but is marginally ahead of the S&P 500 (i.e. a few basis points) since January 1, 2000.

JNJ may be suffering from what is known as “conglomerate-itis”. The company that survived the Tylenol murder scare in the early 1980s (becoming a Harvard case study in crisis management), has faltered badly in the last 10 years.

JNJ’s Consumer business lagged for years, while the Medical Device & Diagnostics carried the growth, (with Pharma lagging too), and those segments reversed as MDD slowed and the Consumer brands started to recover, but this blog stopped following JNJ in 2018, i.e. updating the financials and earnings estimates, and hasn’t kept up with the story.

Take this for what it’s worth, but I’m amazed the healthcare giant hasn’t been broken up. (Still long one JNJ position in one account bought in 2012.)

In the spreadsheet above, the financial sector growth estimate has improved since 12/31, while the industrial sector looks to have been cut in half from +12% expected growth to +6%.

Goldman Sachs (GS) and Schwab (SCHW) are scheduled to report Monday, April 15th, ’24, while Netflix (NFLX) will be the other earnings report which this blog will be watching.

S&P 500 data:

- The forward 4-quarter estimate rose again to $251.81 from $251.58 last week, with the only unusual aspect to that is that the pattern is typically a lower revision than higher.

- The P/E ratio this week is 20.3x down from last week’s 20.6.

- The S&P 500 earnings yield rose again to 4.91%, its second consecutive increase.

- Because of the few companies having reported Q1 ’24 earnings, the upside surprise factor isn’t yet relevant. Last week it was +20%, this week it was +13% for EPS, but take that with a grain of salt.

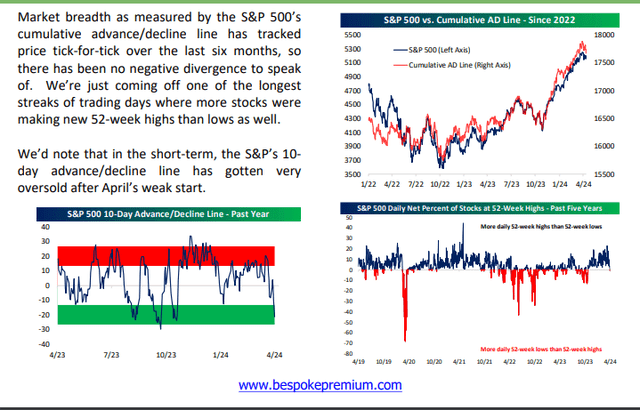

This one chart from Bespoke shows breadth keeping pace with the market advance (always a plus), while the 10-day advance/decline is now very oversold.

Summary/conclusion: S&P 500 earnings do not get really interesting until the week of April 22nd, but there are a few reports of interest this week. Financials usually get their reporting out of the way first, and that’s the case again, as by the end of this week, more than 50% of the financial sector will have reported.

Another earnings post will be forthcoming tomorrow.

Really, there is no reason not to expect another decent earnings season, particularly given the US economy and inflation.

None of this is advice or a recommendation. Past performance is no guarantee or suggestion of future results. Investing can involve the loss of principal, even over short periods of time. Market volatility can change quickly. All S&P 500 EPS and revenue data is sourced from LSEG.

Thanks for reading.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here