A Follow Up

I am writing this as a follow-up to my previous article on HUT 8 Corp (NASDAQ:HUT) (TSX:HUT:CA) published on Seeking Alpha on 11 Dec 2023.

Since then, many changes have happened at HUT:

- After its merger with US Bitcoin Corp (USBTC) on 30 Nov 2023, HUT obtained the court approval for its stalking horse bid on 8 Jan 2024.

- On 11 Jan 2024, J Capital Research released a short report which stated concerns about the merger with USBTC. Shortly after that, on 2 Feb 2024, Marathon (MARA) announced that it will stop its managed service agreement with HUT. This probably caused the stepping down of the CEO on 7 Feb 2024.

- Nevertheless, not all the changes are negatives. HUT was still able to obtain a credit facility from Coinbase (COIN) on 12 Jan 2024. It was also able to sign a deal with Ionic Digital on 1 Feb 2024, potentially bring them a revenue of US$81.5 million over 4 years.

During this period, Bitcoin (BTC-USD) prices rose over 71% while HUT’s share price declined more than 13%. In this article, I will discuss about my action and the reasons related to that, as well as, my plan on HUT.

Comparing BTC Price vs HUT Share Price (Yahoo Finance)

My Action and Reasons

In one of the comments in the previous article, on 7 Feb 2024, I had already stated that I had sold all HUT shares, with only options remaining.

Seeking Alpha

This drastic action was a result of the following reasons.

CEO Was Replaced

One of the primary reasons I initially invested in HUT was their strong balance sheet, its diversified strategic approach to generate fiat revenue as well as mining and holding BTC, and expanding beyond mining by leveraging its cryptocurrency expertise. This direction seemed to be taking shape under former CEO Jaime Leverton’s leadership. While additional details emerged casting the USBTC merger negatively, I believed the combined company retained synergistic potential. I was particularly interested in HUT becoming the “exclusive operator” of Celsius Mining’s fleet, receiving a $15 million annual management fee for five years, net of expenses.

However, Leverton’s abrupt stepping down as CEO on 7 Feb 2024 without a clear rationale prompted me to re-evaluate my position. To be frank, the short report itself did not overly concern me, but the handling of Leverton’s dismissal was, in my view, poorly managed and raised governance issues. The BTC halving event was only two months away, historically correlated with share price increases for mining companies. The Board of Directors could have retained Leverton through that event before parting ways. Furthermore, remaining silent on reasons of changing CEO prior to such an important event triggered numerous red flags for me. As an investor, transparency is paramount.

Leverton was actively posting about HUT and her work in High-performance computing on X as recently as 2 Feb and 7 Feb 2024, suggesting the change in CEO caught her by surprise as well.

Jaime Leverton X Account (X)

In my opinion, these actions led me to the conclusion that my original bullish thesis may no longer held, suggesting that I should exit my position.

The New CEO

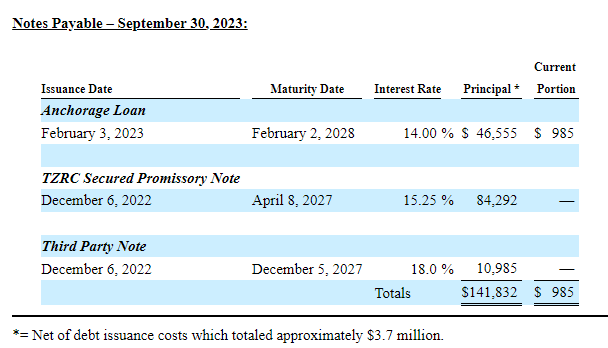

There were two concerns I had regarding the new CEO, Asher Genoot, appointment. Prior to the merger, Genoot was the co-founder and president of USBTC, which was in a bad shape. Upon reviewing USBTC’s financial reports, it became evident that the company was heavily leveraged, with a debt-to-equity ratio of 6.13x. Additionally, the interest rates on these facilities ranged from 14% to 18%, leading to losses and an unsustainable capital structure.

Interest Rate on USBTC Debt Facilities (HUT 10K)

Replacing Leverton with the same individual who was managing the financially troubled USBTC did little to assure me he could better steer HUT. Furthermore, reports (1,2 and 3) suggested that Leverton was dismissed shortly after the short report. But the short report primarily criticized USBTC as a poor acquisition and alleged its management team, including Genoot, had a track record of failed startups. Therefore, simply replacing one allegedly problematic person with another did not inspire confidence in me that HUT is in better hands.

With the benefit of hindsight, interviews Asher conducted after assuming the CEO role at HUT did not provide a compelling vision or strategy that will differentiate his approach. This served only to amplify my doubts that replacing Leverton was the correct decision. Therefore, this further enhanced my view that I should sell my position.

Potential Change in Strategy

The appointment of a new CEO has the potential to signal a strategic shift for the company. According to Reddit, certain long-term HUT investors expressed dissatisfaction with the former CEO for diversifying business revenue. These investors preferred that she concentrate on expanding the mining fleet instead. Therefore, appointing a new CEO raised the possibility that the company may pivot back towards prioritizing miner procurement simply to placate those shareholders.

However, adopting such a “follow the crowd” approach of primarily growing the mining operation would not align with my investment thesis. In my view, mindlessly accumulating more rigs does not differentiate one mining company from its peers, and there are likely better options available with superior efficiencies.

This leadership change brought uncertainty around HUT future direction that ultimately weighed into my analysis and eventual decision to exit the investment.

I May Be Wrong

Despite having already exited my position in HUT, there remains a possibility that the company could outperform my expectations.

New CEO Focus On Improving Efficiency

Some investors had grown frustrated with HUT previous mining operations due to relatively inefficient BTC production. The company’s cost per BTC mined had consistently been on the higher side of industry metrics. The Drumheller facility in particular was underperforming in terms of BTC mining output and the current CEO has closed it.

As a result, relocating mining rigs to sites with more competitive electricity and operational costs seemed a prudent strategic decision. Improving efficiencies at the facility level is important for maintaining competitiveness as BTC network difficulty increases.

Overall, making adjustments to mining infrastructure based on cost considerations and productivity analytics demonstrates a focus on maximizing shareholder value through efficient operations. This might be a start to a better HUT.

HODLing Strategy Will Benefit From Halving Event

It’s important to note that HUT has adopted a HODLing strategy whereby they have a stack of mined BTC that is held long term on its balance sheet. Even though they have been selling their BTC and reducing its stack, as of their most recent disclosure, the company’s still have over 9,000 BTC.

Should the upcoming 24 Apr 2024 halving event catalyze another bullish price response for BTC, it is reasonable to assume BTC price could surge above $100,000 per coin. If that price target is realized, the valuation of HUT’s HODL position alone would exceed US$900 million.

This compares extremely favorably to HUT’s current market cap of US$634 million. Even under a conservative post-halving BTC price scenario, the appreciated value of their reserves could significantly outweigh the firm’s current share price. Should BTC price rise as in previous cycles, HUT’s valuation would have to undergo substantial re-rating.

My Plan

I have fully divested from my prior equity position in HUT given the leadership and strategic uncertainties. Going forward, I intend to generate income by selling put options on HUT shares rather than directly owning the stock for now.

Selling put options allows me to benefit from volatility and time decay without taking on full downside exposure. For example, a 19 Jul 2024 put option with a US$5 strike price offered a premium of approximately US$0.80, translating to an attractive yield of 16%.

If these puts were to be assigned, it would require the share price falling another 40-60% to reach $5. However, at that price, HUT’s market cap would likely still be below the estimated value of its over 9,000 BTC holdings based on current BTC prices of around $73,000 each. This provides some downside protection should the stock continue lower in the near term.

Overall, selling put options is a means of participating in potential HUT upside while mitigating risk, given the current uncertainties facing the firm under new leadership. I can generate yield from premiums without taking a speculative long position in the shares.

Conclusion

While significant uncertainties surround HUT given the leadership changes, the company’s substantial BTC holdings provide some downside protection. With over 9,000 BTC in reserve, it would be quite challenging for even an inept manager to mismanage the firm to the point of insolvency in the near term.

Additionally, for the existing shareholders, maintaining a long position in HUT shares heading into the upcoming BTC halving event could prove rewarding if history repeats. Alternatively, shareholders could generate additional income by selling call options against their positions.

However, longer-term uncertainties linger regarding HUT’s strategic direction and ability to optimize operations under new management. They face an uphill battle to regain efficiency advantages in an increasingly competitive mining environment during this transitional period.

While BTC upcoming halving presents a potential short-term tailwind, ongoing concerns regarding leadership and execution leave me inclined to maintain a NEUTRAL outlook without a direct long equity stake for the time being. Generating option premiums represents my preferred approach.

Read the full article here