Warren Buffett’s Berkshire Hathaway (BRK.A)(BRK.B) has recently been making aggressive investments in the energy sector, particularly in Occidental Petroleum (OXY) (of which it now owns more than a third) and Chevron (CVX) along with some notable energy infrastructure investments in recent years, revealing Buffett’s bullishness on energy. In fact, CVX and OXY are two of Berkshire’s top six stock positions. In this article, we will look at why Buffett is likely buying energy hand-over-fist right now and then share what this means for the Energy Select Sector SPDR Fund ETF (NYSEARCA:XLE).

Why Buffett Is So Bullish On Energy

Buffett’s bullishness on energy is based on several factors:

-

Attractive Industry Fundamentals: Thanks to a renewed focus on high-grading investments, reducing CapEx, and strong recent energy prices, many energy companies have recently become free cash flow machines and have poured that cash into strengthening their balance sheets and return capital to shareholders via buybacks and dividends. Given that Buffett’s investment strategy generally places a premium on companies with strong fundamentals and competent management teams, it makes sense that he would be attracted to the industry in general, and these two companies in particular.

-

Scale: For a conglomerate of Berkshire Hathaway’s size, it needs large businesses to make any investment worthwhile. The energy industry has plenty of large-cap companies and there is a significant need for capital in the sector given that the rise of ESG investing and the pivot towards renewables has starved the sector of capital and reduced energy companies’ appetite for more ambitious growth investments. As a result, the sector appears to be a good match for Berkshire.

-

Macro-Economic and Global Supply Factors: The disruption of global energy supply chains, especially in the wake of Russia’s invasion of Ukraine, has made it clear that the West will need fossil fuels for years to come to ensure its energy security in an increasingly geopolitically fractured and tense world. This gives large energy companies like OXY and CVX a mission-critical role in the economy, which increases their value and reduces downside risk. Moreover, the ESG and pandemic-induced underinvestment in energy infrastructure places a premium on existing fossil fuel energy production facilities and increases the growth profile for companies like OXY and CVX.

-

Buffett’s Traditional Investment Approach: Last, but not least, despite the aforementioned factors, many energy companies remain quite inexpensive, with low P/E ratios and high free cash flow yields despite the S&P 500 (SPY) itself sitting at very lofty valuations. As a result, large energy companies provide Buffett with an increasingly rare opportunity to buy high-quality businesses with healthy fundamentals, strong cash returns to shareholders, and increasing competitive strength in the global energy industry at earnings yields that are quite attractive.

XLE Implications

We agree with Buffett’s bullishness on the sector, especially because the outlook for energy prices looks quite bullish in both the short and long term.

In the short term, OPEC+’s recent strategic decision to curtail oil production puts upward pressure on oil prices, particularly if the global economy can avoid recession as the U.S., Europe, and China continue to try to strike a healthy balance between bringing down inflation and continuing their post-COVID-19 lockdown economic recoveries.

Additionally, escalating geopolitical tensions, notably in energy producing regions like Russia, the Middle East (Israel-Hamas conflict, potential Iran involvement), and South America (Venezuela-Guyana dispute) have the potential to disrupt oil supply chains and even reduce energy production, thereby pushing prices upwards due to supply constraints and a heightened risk perception.

Another significant potential short-term catalyst is the state of US shale oil production. Despite reaching record production levels, the US shale industry faces challenges such as high production costs and vulnerability to fluctuations in oil prices, which could restrict its output growth, thus impacting the global oil supply balance. Moreover, if the Federal Reserve indeed goes through with an easing of its recent quantitative tightening and pivots to interest rate cuts, global economic activity could pick up again, likely boosting demand for oil and natural gas and therefore energy prices are likely to rise once again.

Over the long term, the bull case for energy prices rests largely on anticipated global demand growth, especially from emerging economies, coupled with the continued reliance on oil for transportation, industrial processes, and as a feedstock for petrochemicals. Despite the ongoing transition to renewable energy in major economies in places like Europe, the U.S., and China, demand for oil and natural gas is expected to remain strong in these countries for the foreseeable future while seeing major demand growth in developing economic giants like India and Brazil.

Moreover, growing challenges to oil production, such as the depletion of easily accessible reserves and reduced investment in new oil exploration and production, are likely to tighten the market further, boosting prices further as time goes on.

Buffett’s recent energy investments and our energy sector outlook paint a very bullish outlook for XLE for the following reasons.

First of all, it is made up almost entirely of the largest energy stocks, as per its top 10 holdings (its number 2 holding – making up over 17% of its portfolio – is Buffett’s largest energy stock holding):

- Exxon Mobil (XOM) – 22.68%

- Chevron – 17.41%

- ConocoPhillips (COP) – 8.88%

- Schlumberger (SLB) – 4.54%

- EOG Resources (EOG) – 4.49%

- Marathon Petroleum (MPC) – 4.06%

- Phillips 66 (PSX) – 3.96%

- Pioneer Natural Resources (PXD) – 3.56%

- Valero Energy (VLO) – 3.02%

- ONEOK (OKE) – 2.92%

If Buffett is bullish on large-cap energy – and CVX in particular – that bodes very well for XLE too.

Second, as we already pointed out, higher energy prices bode well for energy producers given the fact that their profits are leveraged to energy commodity prices.

Third, Buffett has in the past cautioned investors against investing in funds with high fees, stating:

Performance comes, performance goes. Fees never falter.

XLE passes this test with flying colors thanks to its very low 0.10% expense ratio.

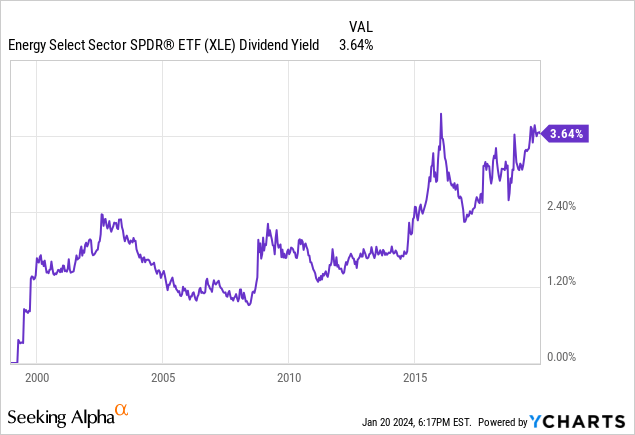

Last, but not least, with a dividend yield of 3.71%, XLE’s yield looks quite attractive at the moment relative to both SPY’s measly 1.38% dividend yield as well as its own history. As the chart below illustrates, prior to the COVID-19 energy sector crash – and barring the 2018 energy sector crash – XLE’s yield has never been as high as it is today:

Investor Takeaway

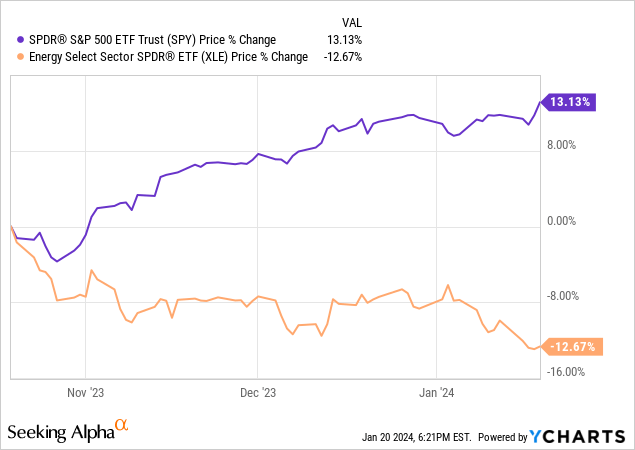

Given the energy sector’s bright future, its alignment with Buffett’s investment strategy, and the fact that XLE has drifted lower in recent months while SPY has rallied higher:

it appears that right now is a very opportunistic time to be contrarian and buy energy hand-over-fist like Buffett.

Read the full article here