Find a job you enjoy doing, and you will never have to work a day in your life.”― Mark Twain.

Shares of temp worker service TrueBlue, Inc. (NYSE:TBI) have started to bounce off a 13-year lows even as the company’s top line has been in steady decline since 2016. A new CEO and CFO have been onboarded to right the company, but there is little yet in terms of a game plan to stem the decline. With a pristine balance sheet, share repurchase program, and compelling valuations on the surface, the recent insider buying merited a deeper dive. An analysis follows below.

Seeking Alpha

Company Overview:

TrueBlue, Inc. is a Tacoma, Washington based provider of contingent workforce solutions, matching ~611,000 individuals with ~84,000 clients in 2022. The company offers general, industrial, commercial driver, and skilled trade staffing, as well as recruitment process outsourcing (RPO) in the U.S., Canada, Puerto Rico, Australia, and the UK. True Blue was founded in 1989 as Labor Ready and debuted on the NASDAQ in 1996, raising net proceeds of $33.6 million at $16.33 per share. Its stock moved onto the NYSE in 1999 with the company changing to its current moniker in 2008. Shares of TBI trades just over $15.00 a share, translating to an approximate market cap of $415 million.

The company operates on a 52- or 53-week fiscal year (FY) ending on the last Sunday before or on December 31st. For the avoidance of doubt, the 52-week period ending December 25, 2022 is FY22.

Segments

Management views its operations through three reporting segments: PeopleReady; PeopleScout; and PeopleManagement.

PeopleReady provides temporary, blue-collared skilled labor for the construction, transportation, manufacturing, retail, hospitality, and renewable energy verticals in the U.S. – where it is the market leader – Canada, and Puerto Rico. For the 39-week period ending September 24, 2023 (23YTD), it generated segment profit of $18.7 million on revenue of $811.1 million versus segment profit of $65.3 million on revenue of $958.3 million in 22YTD.

PeopleScout can both recruit permanent employees and manage multiple third-party staffing vendors on behalf of its clients primarily in the U.S., UK, Canada, and Australia. In 23YTD, it accounted for segment profit of $24.0 million on revenue of $182.1 million, as compared to segment profit of $42.3 million on revenue of $248.8 million in 22YTD.

PeopleManagement provides temp workers to manufacturing, warehousing, and distribution facilities, as well as recruitment and management of dedicated commercial drivers for transportation and distribution applications. It was responsible for segment profit of $4.2 million on revenue of $420.8 million in YTD23, versus segment profit of $11.7 million on revenue of $489.4 million in 22YTD.

Staffing Industry

With TTM revenue of $2.0 billion, TrueBlue competes in an extremely fragmented $680 billion global staffing market, the largest component of which is the $220 billion U.S. opportunity. Major players include ManpowerGroup (MAN) (TTM revenue of $19.1 billion), Robert Half International (RHI) ($6.7 billion), Kelly Services (KELYA) ($4.9 billion), and Korn Ferry (KFY) ($2.8 billion). One of the largest subsegments is domestic industrial staffing, which is estimated at $39 billion. The company also competes in a $6 billion global RPO market, of which North America comprises half the opportunity. Like the global staffing market, it is characterized by no one dominant player and thus ripe for a growth-through-acquisition approach.

Share Price Performance

Despite its long-standing in the industry, TrueBlue’s top line peaked in 53-week FY16 at $2.75 billion as the company entered the higher-margin RPO business (PeopleScout) through two acquisitions in 2014 and 2016. Revenues were trending lower into the pandemic, with FY19 revenue at $2.37 billion. During this period – really from the onset of 2013 through the start of 2020 – shares of TBI remained rangebound between $20 and $31.

The pandemic selloff down to $12.02 per share foreshadowed a significant downdraft in business, with the company’s top line falling to $1.85 billion in FY20. The following year more or less resumed the downtrend witnessed in the pre-pandemic years, with FY21 up 18% year-over-year but down 8% from FY19. FY22 was also up year-over-year (4% to $2.25 billion) but still down 5% versus FY19. TrueBlue’s stock returned to its $20 to $31 range at the onset of 2021 and briefly set an all-time high of $32.91 in October 2021. The bottom end of that range was knocked out for good after the company’s 4QFY22 conference call, when it suggested that 1QFY23 revenue was going to be down double digits year-over-year.

Q3 FY2023 Financials

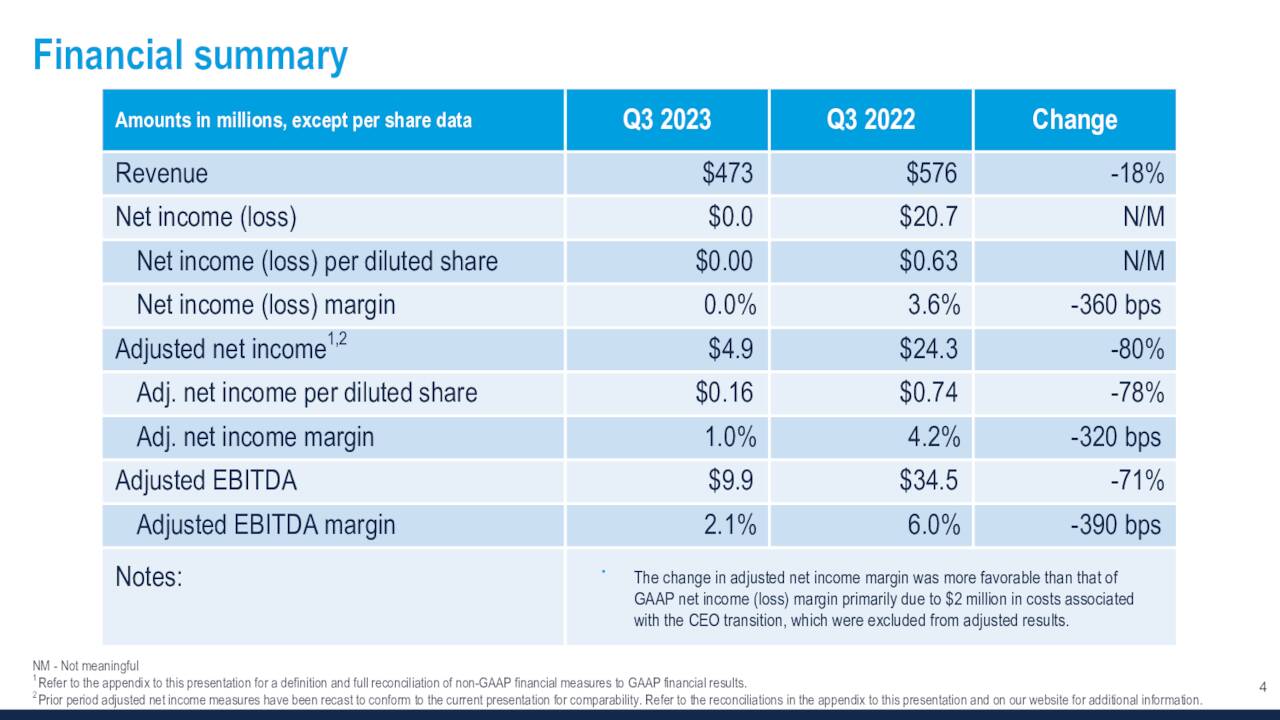

As can be seen from the segment breakdown, that trend has continued throughout FY23, with 23YTD segment profits down 61% to $46.9 million on a 17% decline in revenue to $1.41 billion. And there was little in the company’s 3QFY23 financial report of October 23, 2023, to engender confidence in a turnaround. TrueBlue posted earnings of $0.16 a share (non-GAAP) and Adj. EBITDA of $9.9 million on revenue of $473.2 million, versus $0.74 a share (non-GAAP) and Adj. EBITDA of $34.5 million on revenue of $575.7 million in 3QFY22, representing declines of 78%, 71%, and 18%.

October Company Presentation

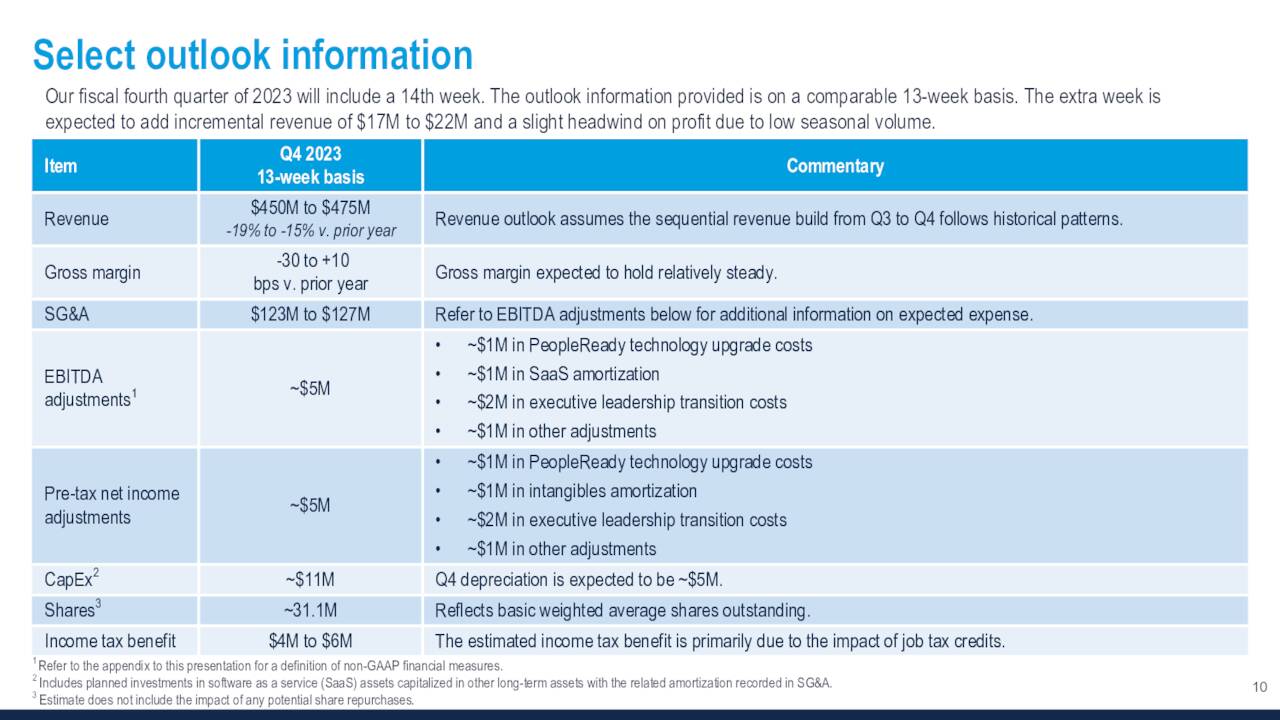

Citing client caution, specific weaknesses in retail, transportation, and service verticals, hiring freezes, lower employee quit rates, and lower average deal sizes in its pipeline, management gave a collective shrug of the shoulders on its post-earnings conference call, forecasting 4QFY23 revenue 17% lower versus 4QFY22 on a 13-week basis to $462.5 million (based on a range midpoint). Since 4QFY23 has 14 weeks, the algebra equated to ~$483 million versus a consensus of $501 million. Unsurprisingly, shares of TBI cratered 22% in the subsequent trading session to $10.70, a level not seen since 2010. The stock has moved up some 20% since then.

October Company Presentation

Owing to TrueBlue’s subpar performance coming out of the pandemic, there have been significant changes in the C-suite, with two new CEOs since June 2022 and a new CFO added in October 2023.

Balance Sheet & Analyst Commentary:

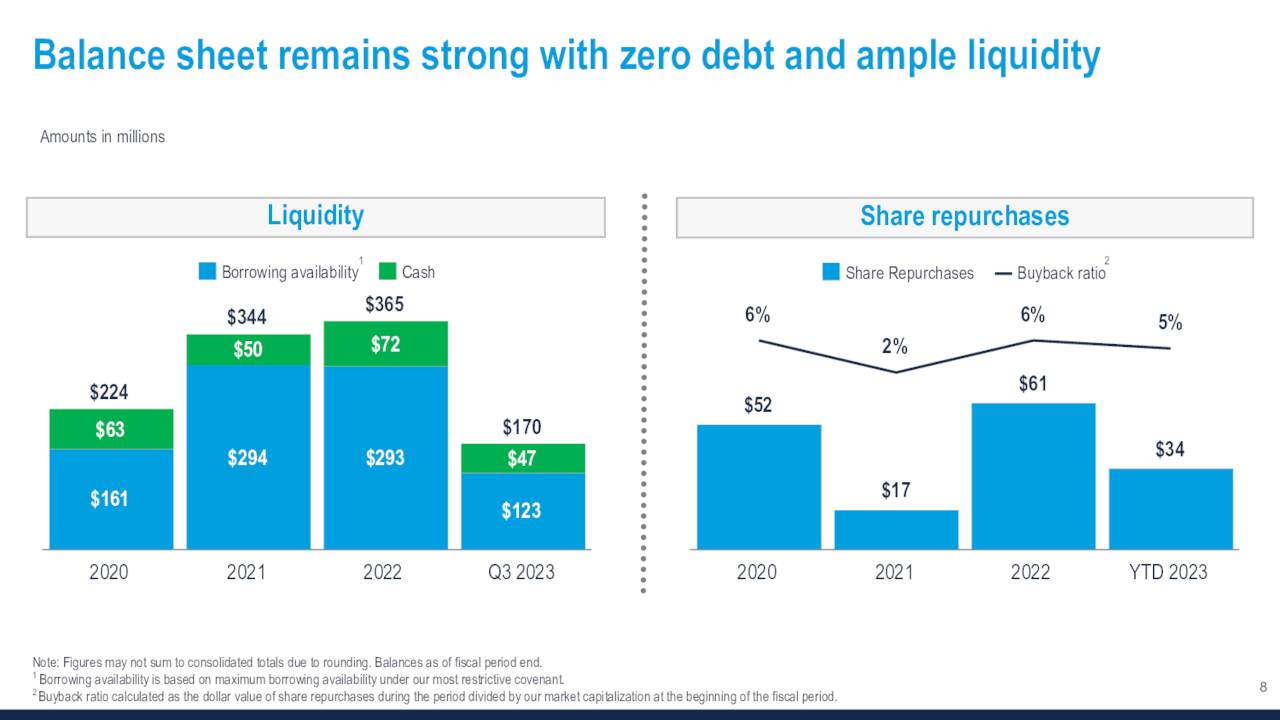

The one positive element for the company is its no-debt balance sheet, which held cash and equivalents of $47.1 million with access to an additional $123 million of liquidity under the most restrictive covenant of its $300 million revolving credit facility. It returns free cash flow to investors in the form of share repurchases, having bought back ~$238 million of its own stock since 2018 (~11.6 million shares). That said, the buying screeched to a halt in 3QFY23, with TrueBlue only repurchasing 6,605 shares. The remaining balance on its current authorization is $55.1 million.

October Company Presentation

Despite the company’s declining top line with no turnaround in sight, the two Street analysts offering commentary on TrueBlue in 2023 are still bullish on its outlook, although BMO Capital lowered its price objective from $20 to $15, while Baird reduced its target from $18 to $16. On average, they expect the company to earn $0.25 a share (non-GAAP) on revenue of $1.89 billion in FY23, followed by $.31 a share (non-GAAP) on revenue of $1.83 billion in FY24.

Newly installed CEO Taryn Owen is bullish on her ability to right the ship, purchasing 10,000 shares of TBI at $11.06 on October 26, 2023. Joining her with a vote of confidence were PeopleScout President Richard Betori (2,500 shares) and board member Kristi Savacool (4,550).

Verdict:

They certainly have a valuation case for TrueBlue, Inc., based on a price to sales basis, given the company’s pristine balance sheet. However, there is little in terms of a game plan to turn the barge away from Niagara Falls. To put things in perspective, the company’s TTM Adj. EBITDA is $44.8 million. The prior twelve months before that, it was $132.1 million. With the exception of the rebound from the pandemic, the company has essentially produced yearly revenue declines since FY16. When factoring higher mortgage rates into the mix, employees are de-incentivized to find work elsewhere as they are essentially trapped in their low-mortgage-rate homes – a lateral move could mean a significantly higher monthly outlay. This low-employee-turnover dynamic is likely to keep True Blue’s top line in decline. As such, as the economy careens into a very uncertain 2024, TrueBlue is to be avoided.

A man is worked upon by what he works on. He may carve out his circumstances, but his circumstances will carve him out as well.”― Frederick Douglass.

Read the full article here